Approval Secrets: Exactly What Paperwork You Need for Alberta Car Financing

Table of Contents

- Key Takeaways

- Introduction: Why Your Paperwork is the Key to the Ignition

- Pillar 1: Proof of Identity (The Alberta Standard)

- Valid Alberta Driver’s License

- Secondary Identification

- Status Documents for Newcomers to Alberta

- Pillar 2: Proving Your Income (The Wild Rose Country Nuances)

- Standard T4 Employment

- The Oil & Gas / Seasonal Worker Challenge

- Self-Employed and 'Gig Economy' Workers

- Income Documentation Comparison Table

- Pillar 3: Proof of Alberta Residency

- Utility Bills and Connectivity

- Rental Agreements and Mortgage Statements

- Pillar 4: Banking and Financial Verification

- The Infamous 'Void Check'

- Bank Statements (The Deep Dive)

- Pillar 5: Alberta Insurance Requirements

- The 'Pink Card' and Beyond

- Gap Insurance in Alberta

- The 'Approval Secrets' for Specific Credit Tiers

- Subprime/Credit Rebuilding: The Reference List

- First-Time Buyers: The Education Secret

- The Role of AMVIC (Alberta Motor Vehicle Industry Council)

- The Bill of Sale

- Mechanical Fitness Assessment (MFA)

- The Digital Workflow: Scanning and Sending

- Common Pitfalls: Why Paperwork Gets Rejected

- Summary Checklist: The 'Approval Secrets' Pack

- Frequently Asked Questions (FAQ)

- Do I need my SIN to get a car loan in Alberta?

- Can I get financed with a temporary/interim paper license?

- What if I just started a new job in Calgary/Edmonton last week?

- Does Alberta require a down payment for every financed deal?

- Can I use my digital pink card for the initial application?

- How do I prove income if I get paid in cash (e.g., servers/tips)?

Walking into an Alberta dealership without your ducks in a row is like trying to drive through a Jasper blizzard without winter tires—you might get moving, but you’re probably going to get stuck. In the modern lending environment, the days of "handshake deals" and "no-doc" loans are largely a thing of the past. Whether you are shopping in the heart of Calgary, the industrial hubs of Edmonton, or the smaller communities across the Peace Country, lenders have become more meticulous than ever.

But here is the good news: being prepared doesn’t just save you from a headache; it actually gives you leverage. When you show up with a complete "Approval Pack," you signal to the lender that you are a low-risk, high-stability candidate. This can be the difference between a 14.9% interest rate and a 6.9% rate. This guide pulls back the curtain on the specific Alberta-centric requirements that will get you behind the wheel faster and with more money left in your pocket.

Key Takeaways

- The "Big Four": Every successful Alberta car loan rests on four pillars: Identity, Income, Residency, and Insurance.

- Alberta Nuances: Our province has unique regulations via AMVIC (Alberta Motor Vehicle Industry Council) and specific lending criteria for seasonal or oil-patch workers.

- Digital is King: While physical copies are okay, high-quality PDF exports from your banking app or employer portal are processed significantly faster by automated underwriting systems.

- The Prime Secret: Pre-organizing your documents allows your finance manager to submit your file to "Prime" lenders (like TD, RBC, or Scotiabank) before settling for higher-interest private lenders.

Introduction: Why Your Paperwork is the Key to the Ignition

Think of your paperwork as the foundation of a house. If the foundation is shaky, the whole structure—no matter how beautiful the truck or SUV is—will eventually collapse. In Alberta, the lending landscape has shifted dramatically over the last few years. Lenders have tightened their belts, moving away from "stated income" loans toward "fully documented" files. This shift is designed to protect both the bank and you, ensuring the loan is actually affordable.

If you walk into a dealership unprepared, you can expect to spend anywhere from four to six hours sitting in a cramped office, scrolling through your phone trying to find your last three paystubs or calling your insurance broker. By having these documents ready in a digital folder or a physical envelope, you can cut that time down to under an hour. More importantly, you mitigate the "Risk Score." Lenders view missing paperwork as a red flag for disorganization or, worse, potential fraud. When you provide everything upfront, you are essentially telling the bank, "I have nothing to hide, and I am a professional borrower."

Pillar 1: Proof of Identity (The Alberta Standard)

Valid Alberta Driver’s License

In Alberta, your driver’s license is more than just a permit to drive; it is the primary anchor for your credit application. Lenders require a valid Class 5 license. If you have a Class 5-GDL (Graduated Driver’s License), don't worry—most lenders treat this the same as a full Class 5 for financing purposes, provided it isn't suspended.

However, there is a common trap: the address. If you moved from Red Deer to Lethbridge six months ago but haven't updated your license, the lender’s "Fraud Detection" system will flag the mismatch between your credit bureau address and your ID. Always ensure your license is current. If it’s expired, a temporary paper "Interim" license from a registry office is usually acceptable, but only if accompanied by the expired hard card or a secondary photo ID.

Secondary Identification

Most "Prime" lenders and all "Subprime" lenders require a second piece of ID to verify your identity. This is a federal anti-money laundering requirement. Acceptable forms include a valid Passport, a Canadian Birth Certificate, or a Permanent Resident (PR) card.

Status Documents for Newcomers to Alberta

Alberta is a magnet for newcomers, and our financing market reflects that. If you are here on a Work Permit or Study Permit, you can still get financed. However, you must provide the original document. Lenders will typically match the length of your car loan to the remaining duration of your permit. You will also need your Social Insurance Number (SIN) card or the official document from Service Canada confirming your SIN.

Pillar 2: Proving Your Income (The Wild Rose Country Nuances)

Standard T4 Employment

If you work a standard 9-to-5 job with a salary or hourly wage, your primary document is the paystub. But not just any paystub. Alberta lenders strictly follow the "30-day rule." Your paystub must be dated within the last 30 days. It must also clearly show your Year-to-Date (YTD) earnings. This allows the lender to verify that you didn't just start the job yesterday and that your income is consistent.

The Oil & Gas / Seasonal Worker Challenge

Alberta’s economy runs on the "patch," which means many workers have fluctuating incomes due to "breakup" or seasonal layoffs. If you work in oil and gas, a single paystub might not tell the whole story. You could be making $15,000 one month and $2,000 the next.

To solve this, lenders will often ask for your last two years of Notices of Assessment (NOA) from the CRA. They will take the average of those two years to determine your "qualifying income."

Self-Employed and 'Gig Economy' Workers

If you run your own business in Calgary or Edmonton, or if you're a full-time delivery driver, you are "Self-Employed" in the eyes of the bank. You will need your last two years of NOAs. Additionally, have your Business License or Articles of Incorporation ready. Lenders want to see that the business is registered in Alberta and has been active for at least two years.

Income Documentation Comparison Table

| Employment Type | Primary Document | Secondary Document | Why Lenders Want It |

|---|---|---|---|

| Full-Time (T4) | Recent Paystub (30 days) | T4 Slip or Letter of Employment | Verifies stability and YTD earnings. |

| Oil & Gas / Seasonal | 2 Years of NOAs | Recent Paystub | Averages out seasonal fluctuations. |

| Self-Employed | 2 Years of NOAs | Business License / Incorporation | Confirms business legitimacy and net income. |

| Disability / Pension | Benefit Statement | 3 Months Bank Statements | Confirms the income is "non-taxable" and "permanent." |

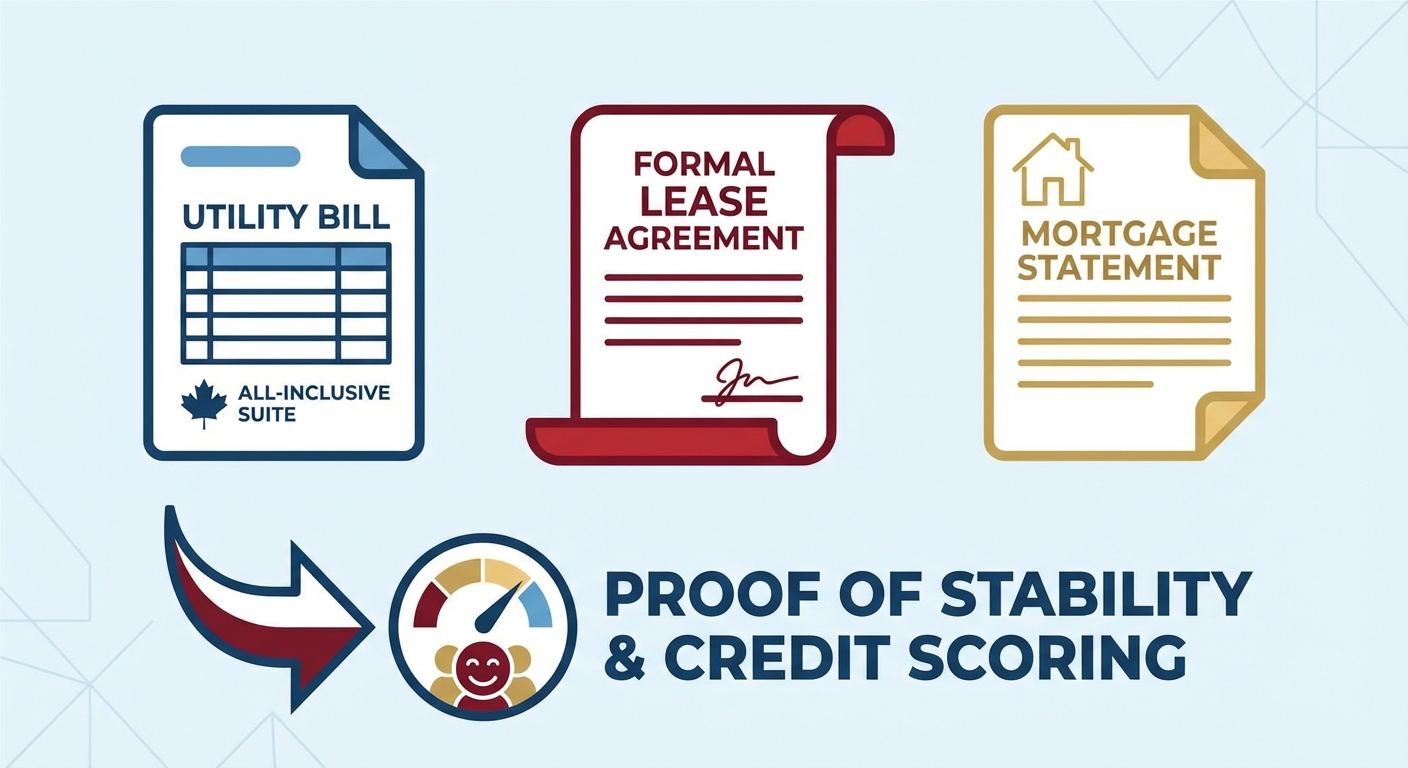

Pillar 3: Proof of Alberta Residency

Lenders need to know where the vehicle is going to be parked and where to send the bills. In Alberta, the "Gold Standard" for residency is a utility bill.

Utility Bills and Connectivity

A bill from Epcor, Enmax, or Telus is preferred because these companies perform their own credit checks. If you have an account with them, it implies a level of stability. The bill must be "fresh"—usually dated within the last 90 days. It must show your name and your physical address (not just a PO Box). If you live in a rural area and use a PO Box, you may need to provide a property tax assessment to show the physical land location.

Rental Agreements and Mortgage Statements

If utilities are included in your rent, a formal lease agreement is your next best bet. For homeowners, a recent mortgage statement works perfectly. Lenders are looking for "Time at Residence." If you have lived at the same spot for more than two years, you are considered a much lower risk than someone who moves every six months.

Pillar 4: Banking and Financial Verification

The Infamous 'Void Check'

Every car loan in Alberta is set up via Pre-Authorized Debit (PAD). The lender will automatically withdraw your payment on your payday (weekly, bi-weekly, or monthly). To set this up, they need a void check. Since most people don't carry checkbooks anymore, you can download a "Direct Deposit Form" or "Pre-Authorized Payment Form" directly from your banking app (ATB, RBC, BMO, etc.).

Bank Statements (The Deep Dive)

For most prime deals, you won't need bank statements. However, if your credit is in the "rebuilding" phase, or if you are self-employed, the lender will ask for the last 90 days of full statements. They aren't just looking at your balance; they are looking for "NSFs" (Non-Sufficient Funds charges).

Pillar 5: Alberta Insurance Requirements

You cannot drive a financed vehicle off a lot in Alberta without a "Pink Card." But for financing, the requirements go deeper than just the basic liability insurance required by law.

The 'Pink Card' and Beyond

While the law requires $200,000 in third-party liability, your lender will mandate "Full Coverage." This means you must have Collision and Comprehensive coverage. This protects the lender’s collateral (the car) in case of an accident or theft. You will need to provide your insurance broker with the "Loss Payable" name and address of the lender (e.g., "TD Auto Finance, PO Box...").

Gap Insurance in Alberta

Because Alberta has no provincial sales tax (GST only), vehicles here often have slightly better "out the door" pricing than in BC or Ontario. However, depreciation still happens the moment you drive off the lot. Gap Insurance covers the "gap" between what you owe the bank and what the insurance company pays out if the car is totaled. While not a required piece of paperwork to *get* the loan, it is a critical piece of the *protection* paperwork you should consider.

The 'Approval Secrets' for Specific Credit Tiers

The amount of paperwork you need is often tied directly to your credit score. Here is how the requirements break down by tier:

| Credit Tier | Score Range | Documentation Level | Key Requirement |

|---|---|---|---|

| Prime | 700+ | Minimal | License & Void Check (often no paystub needed). |

| Near-Prime | 640 - 699 | Moderate | Recent Paystub & Proof of Residence. |

| Subprime | Under 640 | Extensive | Bank Statements, Paystubs, & References. |

Subprime/Credit Rebuilding: The Reference List

If your credit is bruised, lenders want to know who they can call if they can't reach you. You will be asked for a "Reference List"—usually 2 to 5 people. You'll need their names, addresses, and phone numbers.

First-Time Buyers: The Education Secret

If you have no credit because you are a recent graduate from the University of Alberta, SAIT, or NAIT, you can often bypass the "no credit" hurdles by providing your Degree or Diploma. Many lenders have "Graduate Programs" that offer lower rates and lower down payment requirements for those who can prove they have recently completed post-secondary education.

The Role of AMVIC (Alberta Motor Vehicle Industry Council)

In Alberta, we are lucky to have AMVIC. This regulatory body ensures that the paperwork provided by the dealer is just as accurate as the paperwork you provide the bank.

The Bill of Sale

Before you sign your loan agreement, you will sign an AMVIC-standard Bill of Sale. This document must break down the price of the vehicle, any fees (like the AMVIC fee, which is currently $10), and any add-ons. The numbers on this page must match the "Amount Financed" on your bank contract exactly.

Mechanical Fitness Assessment (MFA)

For any used vehicle sold in Alberta, the dealer is legally required to provide you with a Mechanical Fitness Assessment. While the bank doesn't always ask to see this, it is a crucial piece of your "Approval Pack" because it ensures the vehicle you are financing is actually worth the loan you are taking out.

The Digital Workflow: Scanning and Sending

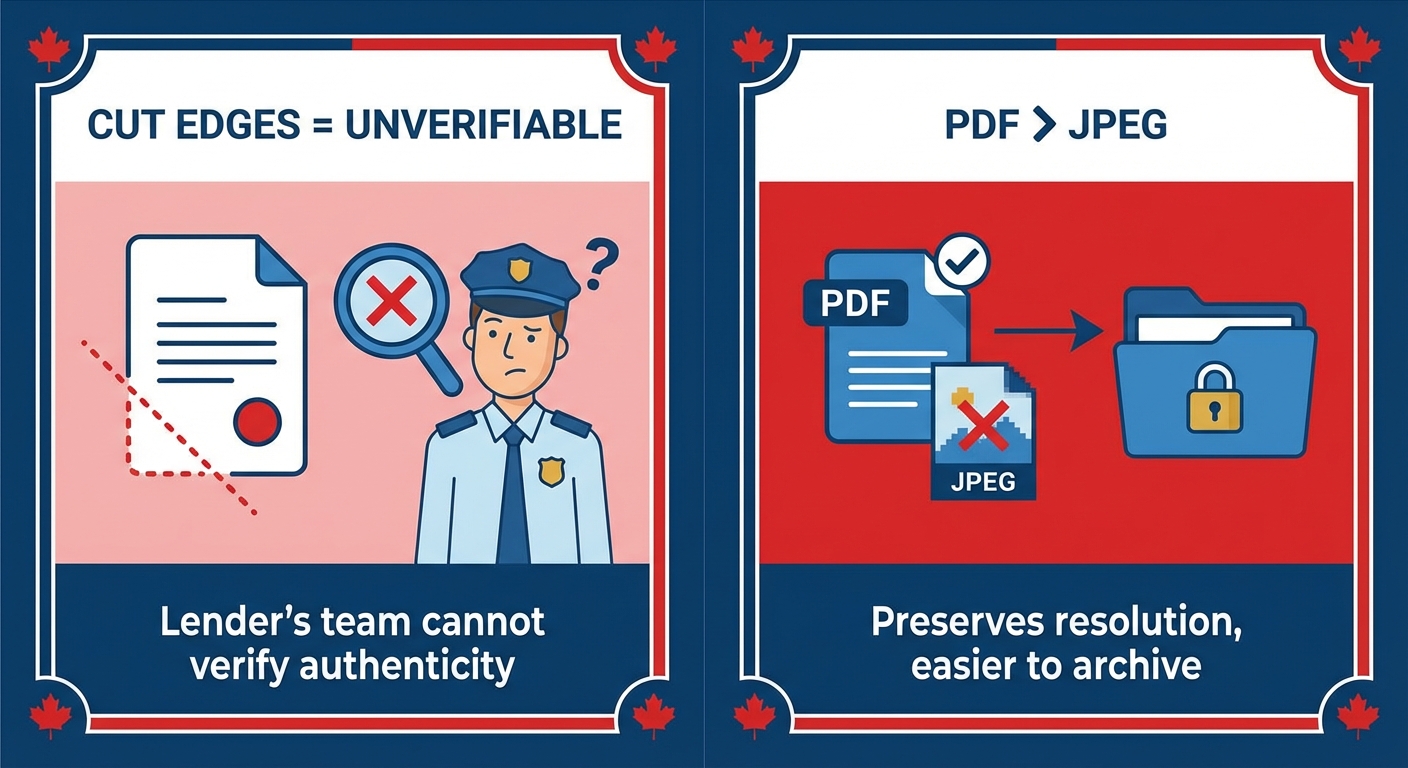

The fastest way to get an approval in today's market is to go digital. If you are taking photos of your documents with your smartphone, follow these rules:

- No Shadows: Don't hold your phone directly over the document in a dark room. Use natural light.

- Four Corners: Ensure all four corners of the page are visible. If a lender sees a "cropped" paystub, they may suspect you are hiding something like a garnishment or a loan deduction.

- PDF is Better: Use a scanning app (like the "Notes" app on iPhone or "Google Drive" on Android) to save the document as a PDF rather than a JPEG.

Common Pitfalls: Why Paperwork Gets Rejected

Even with the best intentions, small mistakes can lead to a "re-hash" (when a lender sends the deal back for corrections). The most common reason for rejection is the "Missing Page" rule. If your bank statement says "Page 1 of 6," the lender's auditor will demand all 6 pages—even if page 6 is completely blank. They need to see the document in its entirety to ensure it hasn't been tampered with.

Another pitfall is the "Illegible Screen Grab." Taking a screenshot of your banking app's "Transaction History" is rarely accepted as a bank statement. You must download the official monthly statement PDF, which includes your name, account number, and the bank’s branding.

Summary Checklist: The 'Approval Secrets' Pack

Before you head to the dealership or apply online, check off these items:

- [ ] Identity: Valid Alberta Driver's License (and Passport/PR Card if needed).

- [ ] Income: Paystub from the last 30 days showing YTD earnings.

- [ ] Taxation: Last 2 years of NOAs (if self-employed or in the oil patch).

- [ ] Residency: Utility bill (Enmax/Epcor/Telus) from the last 90 days.

- [ ] Banking: Direct Deposit form or Void Check from your bank app.

- [ ] Banking: 90 days of full bank statements (if credit is below 640).

- [ ] References: List of 2-5 names, addresses, and phone numbers.

Frequently Asked Questions (FAQ)

Do I need my SIN to get a car loan in Alberta?

While it is not legally required to provide your Social Insurance Number to a dealership, it is highly recommended. Providing your SIN ensures the lender pulls the correct credit bureau. Without it, if you have a common name, the bank might pull someone else's file, leading to an immediate decline or a massive delay while the bureaus are sorted out.

Can I get financed with a temporary/interim paper license?

Yes, but you usually need to provide a secondary photo ID (like a Passport) alongside the interim paper from the registry. The lender needs to see a photo to verify you are who you say you are. Once your hard card arrives in the mail, you should send a copy to the lender to update their files.

What if I just started a new job in Calgary/Edmonton last week?

Financing a car with a brand-new job is possible but difficult if you are still on a "probationary period." Most lenders want to see that you have passed your 3-month probation. However, if you stayed in the same industry (e.g., you moved from one oil company to another with no gap), lenders will often waive the probation requirement if you provide your offer letter and your first paystub.

Does Alberta require a down payment for every financed deal?

No, "Zero Down" financing is very common in Alberta for those with Prime or Near-Prime credit. If your credit is in the subprime category, a lender may request a down payment (usually 10-20%) to "reduce their exposure." Even if not required, putting $1,000 or $2,000 down can often help lower your interest rate.

Can I use my digital pink card for the initial application?

For the initial application, a digital pink card is usually fine. However, before the dealer can release the vehicle to you, they will need to see that the "Loss Payable" has been updated to the new lender. Most insurance apps allow you to update this and download a new digital card in minutes.

How do I prove income if I get paid in cash (e.g., servers/tips)?

Cash income is the hardest to prove. Lenders generally do not accept "hand-written logs." To use tip income for financing, you must show that the cash was deposited into your bank account regularly or that it was declared on your previous year's taxes (showing up on your NOA). If it’s not on your bank statement or your NOA, the lender will consider it "non-existent."