Key Takeaways

- Risk Sharing is Key: Specialized programs like the CSBFP reduce lender risk by having the government guarantee a portion of the loan, making approvals easier for businesses that lack traditional collateral.

- Modernized Limits: Since 2022, loan ceilings have increased to $1.15 million, and for the first time, specialized lines of credit are available to help with daily operational liquidity.

- Sector Focus Wins: Approval isn't just about your credit score; it's about matching your business type (Agri-food, Tech, Manufacturing) to the specific mandate of the lender.

- Strategic Stacking: You can combine different government-backed loans to cover both long-term equipment purchases and short-term working capital needs.

The Evolving Landscape of Canadian Business Financing

For decades, the path to business growth in Canada felt like a narrow corridor. You walked into one of the "Big Five" banks, presented a mountain of collateral, and hoped your personal credit score was high enough to satisfy a rigid algorithm. If you didn't fit the mold, the door was often shut. However, the narrative is shifting. We are entering an era where "specialized" is the new standard for savvy entrepreneurs.

The current economic climate has forced a rethink. With fluctuating interest rates and a push for domestic innovation, the Canadian government and crown corporations have doubled down on specialized loan programs. These aren't just safety nets; they are strategic tools designed to propel Small and Medium-sized Enterprises (SMEs) past the hurdles of traditional lending. Whether you are a startup in Vancouver or a manufacturing plant in Southern Ontario, understanding these specialized avenues is the secret to unlocking capital that your competitors might not even know exists.

What exactly defines a "specialized" program? In the Canadian context, these are financial products where the risk is shared between a private lender and a government entity, or programs where the lending criteria are tailored to specific demographics, industries, or environmental goals. They move beyond the "one size fits all" approach of commercial term loans.

The Foundation: The Canada Small Business Financing Program (CSBFP)

If there is a flagship for specialized lending in Canada, it is the Canada Small Business Financing Program. This program has been a cornerstone for years, but it underwent a massive transformation in 2022 that many business owners have yet to fully exploit. The brilliance of the CSBFP lies in its risk-sharing model. When you apply through a bank or credit union, the federal government guarantees up to 85% of the loss to the lender if the business defaults. This single factor turns a "No" into a "Yes" for thousands of applicants every year.

2022 Program Enhancements: A Deep Dive

The 2022 updates were the most significant in the program's history. Before these changes, the CSBFP was often criticized for being too rigid, focusing almost exclusively on "hard assets" like real estate and heavy machinery. The modernization changed the game in three distinct ways:

- The Line of Credit Option: For the first time, the CSBFP includes a line of credit of up to $100,000. This is revolutionary for businesses that struggle with seasonal cash flow or need to bridge the gap between accounts receivable and accounts payable.

- Increased Loan Amounts: The maximum loan amount jumped from $1 million to $1.15 million. This includes a maximum of $1 million for real property and $500,000 for equipment and leasehold improvements.

- Extended Terms: Loan terms were extended to match the life of the assets, with some real property loans now stretching up to 15 years, significantly lowering the monthly debt-servicing burden on the business.

To be eligible, your business must be a for-profit entity in Canada with annual gross revenues of $10 million or less. This covers the vast majority of Canadian businesses, yet many owners still assume they are "too small" or "not established enough" to qualify.

Sector-Specific Specialized Loans

Sometimes, the secret to approval isn't a general program, but one that speaks the language of your specific industry. Traditional banks often struggle to value software-as-a-service (SaaS) companies or specialized farming equipment. That's where sector-specific lenders step in.

Technology and Innovation

The Business Development Bank of Canada (BDC) offers specialized tech financing that ignores the traditional requirement for physical collateral. Instead, they look at your recurring revenue, your intellectual property, and your growth trajectory. They understand that a tech company's value is in its code and its customer base, not its office furniture.

Agriculture and Agri-Food

Farm Credit Canada (FCC) is the heavyweight in this sector. Their programs are designed around the agricultural cycle. They offer "Flexi-term" loans where you can skip principal payments during a bad harvest or a market downturn. This level of specialization is something a general commercial lender simply cannot provide.

Manufacturing and Exporting

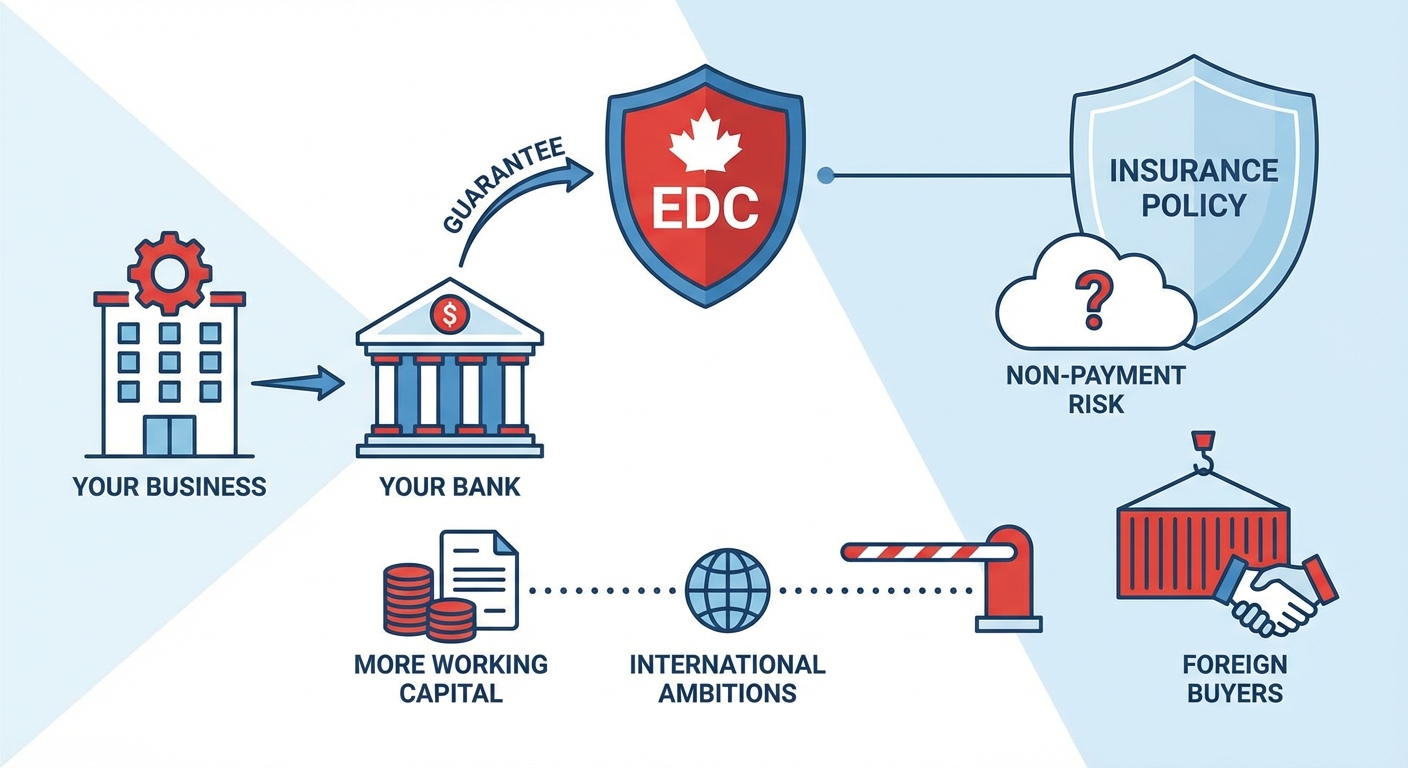

If your business is looking to move goods across the border, Export Development Canada (EDC) provides guarantees that allow your bank to lend you more working capital. They essentially act as an insurance policy for your international ambitions, covering the risks of non-payment by foreign buyers.

Programs for Underrepresented Entrepreneurs

The Canadian government has identified that certain groups face systemic barriers when accessing capital. To level the playing field, specialized programs have been launched that prioritize social impact alongside financial viability.

The Women Entrepreneurship Strategy (WES) is a multi-billion dollar investment aimed at increasing women-owned businesses' access to the financing, talent, and networks they need. Similarly, the Black Entrepreneurship Loan Fund provides loans of up to $250,000 to Black business owners and entrepreneurs across Canada. These programs often come with mentorship components, recognizing that capital alone isn't always enough for long-term success.

For Indigenous entrepreneurs, the National Aboriginal Capital Corporations Association (NACCA) and its network of Aboriginal Financial Institutions (AFIs) provide specialized developmental loans. These lenders look beyond standard credit scores, focusing instead on the community impact and the long-term sustainability of the business within its local context.

Newcomers to Canada face a unique challenge: the "thin file" problem. Without a Canadian credit history, traditional banks are often hesitant. However, organizations like Windmill Microlending or specialized newcomer programs at major credit unions offer "character-based" lending. They value your international experience and educational background, providing the seed capital needed to start a business in your new home.

The 'Approval Secrets': What Lenders Don't Always Tell You

You can have the best business idea in the world, but if you don't speak the lender's language, the vault stays locked. Approval for specialized programs hinges on the "Five Cs" of credit, but through a modified lens.

- Character: In specialized lending, this is often about your industry experience. Have you run a business like this before?

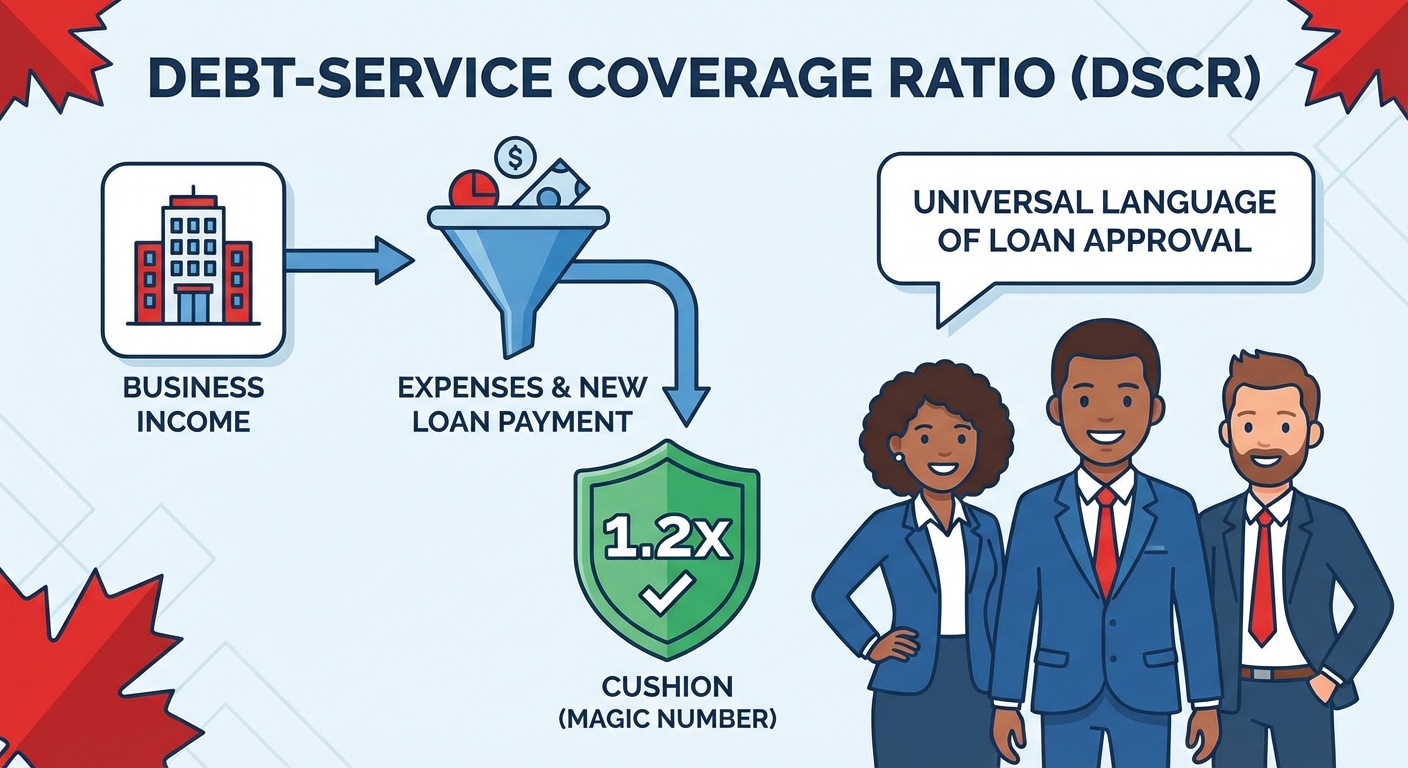

- Capacity: This is your ability to repay. Lenders look at your Debt-Service Coverage Ratio (DSCR).

- Capital: Your personal "skin in the game." Even with a government guarantee, you usually need to contribute 10-20% of the project cost.

- Collateral: While specialized programs reduce collateral requirements, they don't eliminate them. What assets can be pledged?

- Conditions: The external environment. How does your business survive a recession or a supply chain disruption?

The Power of a 'Bank-Ready' Business Plan

A specialized lender isn't looking for a 50-page manifesto. They want a "Bank-Ready" plan. This means clear financial projections (Income Statement, Balance Sheet, Cash Flow) for at least the next two years. It means a clear explanation of how the loan will generate more revenue than the cost of the interest. If you are applying for a specialized loan to buy a $200,000 CNC machine, show the lender exactly how many new contracts that machine will allow you to sign.

| Feature | Traditional Commercial Loan | Specialized Loan (e.g., CSBFP) |

|---|---|---|

| Collateral Requirement | Often 100% or more of loan value | Significantly reduced (85% Gov Guarantee) |

| Interest Rates | Variable, based on risk profile | Capped at Prime + 3% (for CSBFP) |

| Approval Focus | Credit Score & Hard Assets | Business Plan & Sector Potential |

| Personal Guarantee | Usually 100% of loan amount | Often limited to 25% of the total loan |

Purpose-Driven Financing: Green and Sustainable Loans

As Canada moves toward a net-zero economy, "Green" financing is becoming one of the most accessible specialized categories. If your business is looking to upgrade to energy-efficient HVAC systems, install solar panels, or transition a delivery fleet to electric vehicles, there are specific pools of capital waiting for you.

The BDC and various provincial bodies offer "Green" loans that often feature lower interest rates or longer repayment holidays. The logic is simple: energy-efficient businesses have lower operating costs, making them lower-risk borrowers in the long run. Furthermore, many of these loans can be paired with federal tax credits for clean technology, effectively reducing the "net cost" of your expansion. Being "Green" isn't just a PR move anymore; it's a financial strategy that lowers your cost of capital.

Navigating the Application Process: A Step-by-Step Roadmap

Applying for a specialized loan can feel like a marathon, but it's manageable if you break it down into four distinct phases.

Step 1: Internal Audit

Before you talk to a lender, you need to know your numbers. What is your funding gap? Do not just ask for "as much as I can get." Specialized programs require a specific "Use of Proceeds." Are you buying equipment? Renovating a leased space? Buying a competitor's assets? Be precise.

Step 2: Selecting the Right Program

Match your need to the program's mandate. If you need a line of credit for inventory, the new CSBFP LOC is your best bet. If you are a tech startup with no assets but high revenue, BDC is your destination. Don't waste time applying for programs where you don't fit the primary criteria.

Step 3: Documentation - The 'Secret' Checklist

Speed of approval is almost always determined by how quickly you can produce these documents:

- Last 2-3 years of Financial Statements (Accountant-prepared is best).

- Personal and Business Tax Returns (Notice of Assessments).

- A copy of your commercial lease (if applicable).

- Detailed quotes or invoices for the assets you intend to purchase.

- Proof of your personal investment (bank statements showing the 10-20% down payment).

Step 4: The Pitch

When you sit down with the lender, don't just talk about your product. Talk about the Debt-Service Coverage Ratio (DSCR). Show them that after all expenses and your new loan payment are covered, the business still has a cushion of at least 1.2x. This "magic number" is the universal language of loan approval.

Common Pitfalls and How to Avoid Them

Even with the best intentions, many applications for specialized loans hit a wall because of avoidable mistakes. One of the most common is misunderstanding "ineligible" costs. For example, under the CSBFP, you cannot use the funds to pay off existing debt or to fund general working capital (outside of the specific $100,000 Line of Credit). If you submit a plan that uses 50% of the funds for "marketing," the application will be rejected immediately.

Another pitfall is over-leveraging. Just because you can borrow $1.15 million doesn't mean you should. Specialized debt is still debt. It must be repaid. Taking on too much leverage, even with a government guarantee, can stifle your cash flow and prevent you from reacting to market changes.

Lastly, incomplete documentation is the #1 reason for delays. If a lender asks for three years of financials and you provide two, the clock stops. In the world of specialized lending, "close enough" is never good enough. Treat your application with the precision of a surgical procedure.

Frequently Asked Questions

Can I apply for a specialized loan if I have a low credit score?

Yes, but it depends on the reason for the low score. Specialized programs like those from NACCA or the Black Entrepreneurship Loan Fund often look at the "holistic" picture of the business owner. However, if your low score is due to recent, unresolved bankruptcies or defaults on government debt (like unpaid taxes), approval will be very difficult. The government guarantee is meant to offset a lack of collateral, not a lack of financial responsibility.

What is the maximum amount I can borrow under the CSBFP?

As of the 2022 updates, the maximum total amount is $1.15 million. This is broken down into specific categories: up to $1 million for real property, $500,000 for equipment and leasehold improvements, and a $100,000 line of credit. Note that the total combined amount across all these categories cannot exceed the $1.15 million ceiling.

Do specialized loans require personal guarantees?

Most do, but they are often limited. For a traditional commercial loan, a bank might ask for a 100% personal guarantee. Under the CSBFP, the personal guarantee is typically limited to 25% of the total loan amount. This protects your personal assets (like your home) much more than a standard loan would.

How long does the approval process typically take compared to traditional loans?

Specialized loans generally take longer-anywhere from 4 to 8 weeks. This is because there is an extra layer of "due diligence" to ensure the loan meets the government's or the specific program's criteria. Traditional loans can sometimes be approved in days, but they carry much stricter requirements for collateral and credit.

Can I use specialized loans to buy out a competitor?

Yes, but with caveats. Under the CSBFP, you can use the funds to purchase the assets of another business (equipment, real estate, etc.). However, you generally cannot use it to buy "shares" of a company. If you are looking for a share-purchase buyout, you would be better served looking at BDC's specialized "Transition Capital" or "Mezzanine Financing" programs.

Future-Proofing Your Business with the Right Capital

The landscape of Canadian business financing is no longer a monolith. The "Approval Secrets" are no longer hidden behind the mahogany doors of executive boardrooms; they are found in the specialized mandates of programs designed to foster diversity, innovation, and sustainability. By understanding the risk-sharing nature of the CSBFP, the sector-specific expertise of the BDC and FCC, and the targeted support for underrepresented entrepreneurs, you can position your business to thrive even in uncertain times.

Capital is the fuel for your business engine. By choosing specialized financing, you aren't just getting a loan; you are entering into a partnership where the lender and the government have a vested interest in your success. Don't wait for your local branch to offer these programs to you. Arm yourself with your "Bank-Ready" plan, understand your DSCR, and proactively seek out the specialized capital that fits your vision. The path to growth is open; you just need to know which door to knock on.