Auto Loan With Active Collections: The Approval Mechanics

Table of Contents

- Key Takeaways: Your Quick-Start Guide to Approval

- The Lender's Gauntlet: Seeing Your Application Through Their Eyes

- The Psychology of Underwriting: Moving Beyond Just the Credit Score

- The Automated vs. Manual Review

- Anatomy of a Collection: Deconstructing What Lenders Actually Care About

- The Hierarchy of Debt: Which Collections Are Deal-Breakers?

- The Age Factor: Time Heals Most Credit Wounds

- The Balance Threshold

- Deep Dive: 'Paid in Full' vs. 'Settled for Less' vs. 'Active'

- The Approval Engine: The Four Pillars That Override a Bad Score

- Pillar 1: Provable Income & Job Stability

- Pillar 2: The Down Payment

- Pillar 3: The Debt-to-Income (DTI) Ratio

- Pillar 4: The Right Vehicle

- Choosing Your Arena: Where to Apply for the Best Odds & Terms in 2026

- The Big Bank/Credit Union Approach

- The Dealership's 'Special Finance' Department

- The Online Subprime Lender

- The 'Buy Here, Pay Here' Trap

- The 2026 Outlook: New Rules and Market Shifts Impacting Your Loan

- The FICO 10T & VantageScore 4.0 Effect

- Economic Headwinds

- Regulatory Scrutiny on Medical Debt

- Your 30-Day Action Plan for Approval

- Week 1: The Credit Audit

- Week 2: The Strategic Strike

- Week 3: The 'Proof Packet' Assembly

- Week 4: The Application Gauntlet

- Frequently Asked Questions: Your Final Doubts Answered

Key Takeaways: Your Quick-Start Guide to Approval

- Yes, Approval is Possible: Getting an auto loan with active collections is achievable, but it requires a strategic approach. Lenders focus more on your recent payment history and income stability than on old collection accounts.

- Not All Collections Are Equal: Lenders view a $200 medical collection differently than a $5,000 defaulted credit card. The type, age, and amount of the collection heavily influence the lender's decision.

- Paying Isn't Always the Answer: Paying off a collection doesn't instantly remove it or guarantee a score increase. In some cases, especially with old debt, it's better to leave it alone and focus on other factors like your down payment.

- Your DTI is King: Your Debt-to-Income (DTI) ratio is often more critical than your credit score. Lenders need to see you can afford the new payment, regardless of past mistakes.

- Where You Apply Matters: Dealerships with 'special finance' departments are often better equipped to handle files with collections than traditional banks or credit unions.

The Lender's Gauntlet: Seeing Your Application Through Their Eyes

So, can you get an auto loan with active collections in Canada? The short answer is yes, absolutely. However, lenders view active collections as a significant risk indicator, meaning your application will be scrutinized far more closely than a standard one. Understanding their perspective is the first step to building an application they can't refuse.

When an underwriter sees a collection account, they don't just see a number. They see a story of a past financial obligation that went unfulfilled. Their primary job is to assess the risk that you might do the same with the new auto loan they're considering giving you. It's not personal; it's a calculated business decision based on patterns of behaviour.

The Psychology of Underwriting: Moving Beyond Just the Credit Score

While your credit score is the first gatekeeper, a human underwriter looks for context. They're trying to answer a few key questions:

- Was this a one-time mistake or a pattern of non-payment?

- Was the collection due to a temporary hardship (like a job loss or medical issue) or chronic financial mismanagement?

- What has the applicant done since the collection to demonstrate stability?

An application with a low score but recent, consistent on-time payments on other accounts can often look better than one with a slightly higher score but an active, recent collection.

The Automated vs. Manual Review

Most prime lenders use an automated system. If your score and DTI fit within their pre-set boxes, you get an instant approval. An active collection, especially a recent one, is a common trigger that kicks your application out of the automated queue and onto a human underwriter's desk. This is both a challenge and an opportunity. The computer says "no," but a person has the power to say "yes" if you give them a compelling reason.

A single, large collection from a defaulted credit card can poison an otherwise decent application. To an underwriter, this signals a high-risk event. Conversely, a small, old utility bill collection might be overlooked entirely. The context is everything.

Pro Tip: Use the 'Notes' Section

In your application's notes section (if available online or when speaking to a finance manager), briefly and professionally explain the circumstance behind a significant collection. For example: "The 2023 Rogers collection was related to a disputed final bill after moving provinces. The matter is currently under review." Honesty and context can be the difference between a decline and a manual review that leads to approval.

Anatomy of a Collection: Deconstructing What Lenders Actually Care About

Not all debt is created equal in the eyes of a lender. To build a winning strategy, you need to analyze your own credit report like an underwriter would. The type, age, and status of your collection accounts tell a detailed story about your financial past—and your potential future risk.

The Hierarchy of Debt: Which Collections Are Deal-Breakers?

Lenders categorize collections by their perceived severity. Here’s how they generally stack up, from least to most concerning:

- Medical Collections: Often viewed with the most leniency. Lenders understand these can be unexpected and don't always reflect poor financial planning.

- Utility/Telecom Collections (e.g., Hydro, Bell, Rogers): These are more serious but are often for smaller amounts and can sometimes be explained by moving or billing disputes.

- Unsecured Credit Lines (Credit Cards, Personal Loans): This is a major red flag. Defaulting on a loan from a financial institution suggests a higher risk of defaulting on another one.

- Previous Auto Loans (Repossessions): This is the cardinal sin of auto lending. A past repossession, especially a recent one, makes approval extremely difficult, though not impossible.

The Age Factor: Time Heals Most Credit Wounds

The recency of a collection is arguably more important than its amount. A 6-year-old, $2,000 collection that's about to fall off your credit report is almost irrelevant. A 6-month-old, $500 collection is a five-alarm fire for an underwriter because it indicates a very recent financial struggle.

- 0-2 Years Old: Maximum negative impact. This is a critical red flag.

- 2-4 Years Old: Still very relevant, but the negative impact begins to fade.

- 5+ Years Old: Much less weight. Many lenders will disregard collections this old if the rest of the file is strong.

The Balance Threshold

While a lower balance is always better, lenders often have internal thresholds. Many will overlook a collection or two if the total is under $500. Once you cross into the $1,000 - $1,500 range, it becomes a mandatory discussion point. A $3,500 collection will require a very strong application in other areas (like income and down payment) to overcome.

Deep Dive: 'Paid in Full' vs. 'Settled for Less' vs. 'Active'

This is one of the most misunderstood aspects of credit reports. How you resolve a collection matters immensely.

- Active/Open: The worst status. It tells a lender the issue is unresolved and you still owe the money. This is a primary reason for decline.

- Paid in Full: The best possible outcome for a collection. It shows you took responsibility and fulfilled the original obligation. While the original negative mark remains for ~6 years, the "Paid" status is a huge positive signal.

- Settled for Less: A mixed bag. It's better than "Active" because the account is closed. However, it tells the lender you didn't repay the full amount. This is less favourable than "Paid in Full" but still a major improvement over an open collection. For those dealing with larger debts, understanding your options is key. Our guide on Zero Down Car Loan After Debt Settlement 2026 provides more detailed strategies on this topic.

The Approval Engine: The Four Pillars That Override a Bad Score

Your credit score is a look in the rearview mirror. Lenders, especially in the subprime space, are more concerned with what's happening through the windshield. If you can build a powerful case based on your current stability, you can often override the negative history of a collection account. These are the four pillars of a strong application.

Pillar 1: Provable Income & Job Stability

This is non-negotiable. Lenders need to see that you have a consistent, verifiable source of income sufficient to cover your existing debts plus the new car payment. Job stability is a massive factor.

- The Gold Standard: 2+ years at the same full-time job with T4 income.

- The Silver Standard: 6 months to 2 years at your current job, or a consistent history in the same industry.

- The Challenge: Self-employment, contract work, or very new employment. While not impossible, these situations require more documentation to prove income stability. If you're self-employed, our guide Self-Employed? Your Bank Doesn't Need a Resume can help you prepare the right documents.

In our experience, an underwriter will always favour a borrower with a 620 score and 3 years on the job over a borrower with a 660 score who just started a new job last month.

Pillar 2: The Down Payment

A down payment is the single most effective tool for getting approved with collections. It reduces the lender's risk in two ways:

- It lowers the Loan-to-Value (LTV) ratio, meaning they have less money at risk if you default.

- It demonstrates your own "skin in the game," showing you're financially invested in the purchase.

For a subprime loan, aiming for a 10-20% down payment can dramatically increase your approval odds and may even help you secure a better interest rate.

Pillar 3: The Debt-to-Income (DTI) Ratio

Your DTI is your secret weapon. It's a percentage that shows how much of your gross monthly income goes towards servicing your debts. Lenders use it to determine if you can realistically afford a new payment.

How to Calculate Your DTI:

- Add up your monthly debt payments: This includes rent/mortgage, credit card minimum payments, student loans, and any other loan payments. (Do NOT include utilities, groceries, etc.).

- Find your gross monthly income: This is your total salary before any taxes or deductions.

- Divide your total monthly debts by your gross monthly income.

- Multiply by 100 to get the percentage.

Example: $1,500 in total debt payments / $4,500 gross monthly income = 0.333. Your DTI is 33.3%.

Most subprime lenders want to see a DTI (including the new estimated car payment) of under 45-50%. A low DTI tells a lender that even with past credit issues, you have the cash flow to handle your obligations now.

Pillar 4: The Right Vehicle

The car you choose is part of the loan application. Lenders prefer to finance assets that hold their value.

- The Sweet Spot: A 2-5 year old, reliable used car with reasonable kilometres (e.g., a Honda Civic, Toyota RAV4). These vehicles have already taken their biggest depreciation hit but are new enough to be dependable.

- The Red Flags: Very old (10+ years), high-mileage vehicles, or overly expensive new cars that stretch your budget. Lenders see old cars as a breakdown risk (leading to non-payment) and expensive cars as an affordability risk.

Pro Tip: Bring Your "Proof Packet"

Don't just tell them you're stable—show them. Bring 3 months of bank statements to the dealership. Showing a consistent positive balance, regular deposits, and no NSF (non-sufficient funds) fees provides powerful evidence of financial stability that a simple credit report cannot convey.

Choosing Your Arena: Where to Apply for the Best Odds & Terms in 2026

Where you submit your application is just as important as what's in it. Different lenders have different appetites for risk. Going to the right place first can save you from unnecessary credit inquiries and frustrating declines.

The Big Bank/Credit Union Approach

If you have a long-standing relationship with your bank or credit union and your collections are minor (e.g., one small, old medical bill), this is worth a shot. They typically offer the best interest rates. However, their underwriting criteria are the strictest. They rely heavily on automated systems and credit scores, making them less likely to approve an application with significant or recent collections.

The Dealership's 'Special Finance' Department

This is often the most effective path to approval for applicants with collections. Here's why:

- Specialized Lenders: These departments don't work with the big banks. They have established relationships with a portfolio of subprime lenders who specifically work with high-risk files.

- Expertise: The finance managers are experts at structuring deals to get them approved. They know what each lender is looking for and can present your application in the best possible light.

- One-Stop-Shop: They handle everything from the application to finding a suitable vehicle that fits the lender's criteria.

The trade-off is typically a higher interest rate, but for many, it's the difference between getting a car and not getting one.

The Online Subprime Lender

Companies that offer pre-approval online can be a good starting point. They allow you to see what you might qualify for without a hard credit check initially. However, you must be cautious. Vet these companies carefully and read all the fine print, as some can have predatory terms. The initial offer is often not the final one.

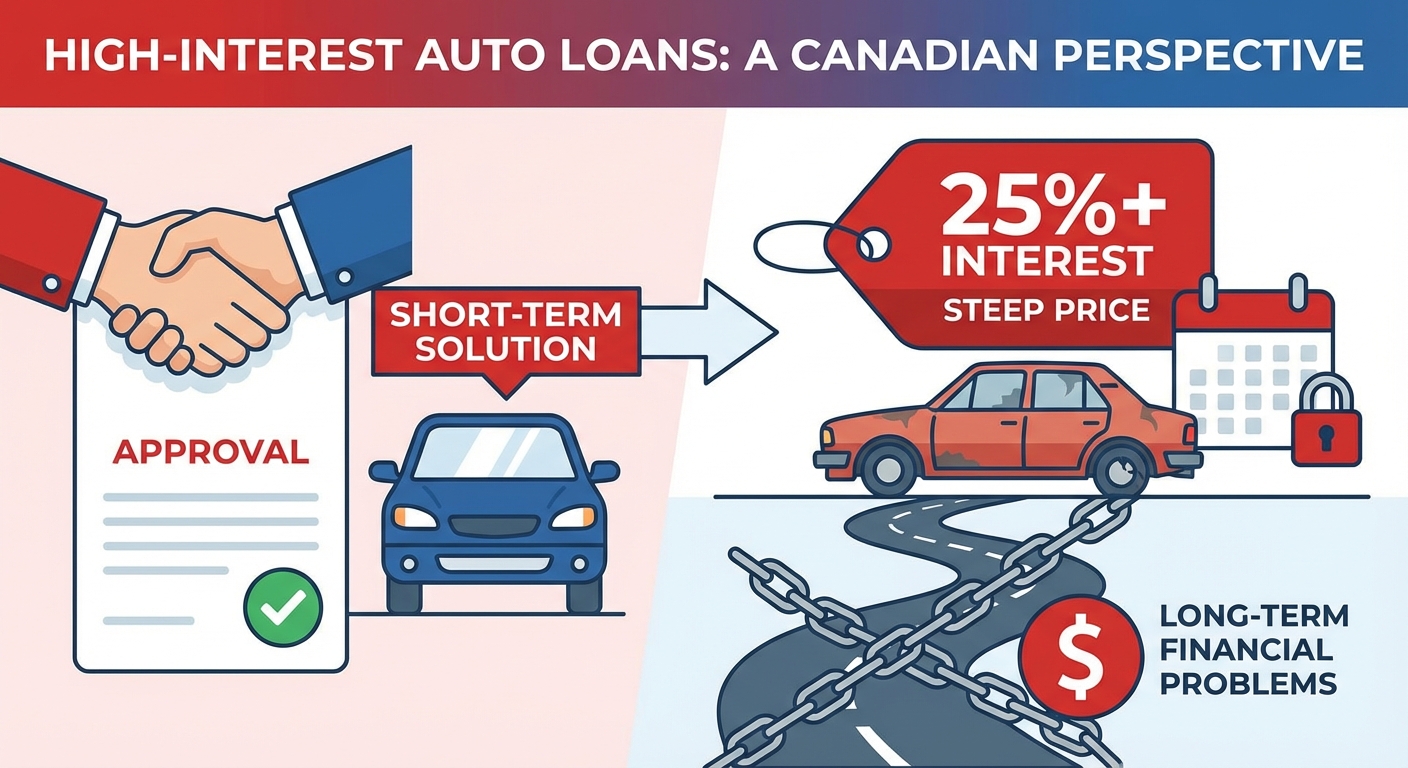

The 'Buy Here, Pay Here' Trap

This should be your absolute last resort. Buy Here, Pay Here (BHPH) lots finance their own vehicles, meaning they don't use external lenders. While approval is virtually guaranteed, it comes at a steep price: sky-high interest rates (often 25%+), older and less reliable vehicles, and strict payment schedules. They are a short-term solution that can create long-term financial problems.

| Lender Type | Approval Odds (w/ Collections) | Typical Interest Rate Range (2026) | Pros | Cons |

|---|---|---|---|---|

| Big Bank / Credit Union | Low | 7% - 12% | Best rates, potential relationship benefits. | Strict criteria, unlikely to approve recent/large collections. |

| Dealership Special Finance | High | 10% - 25% | Expertise in subprime, access to specialized lenders, high approval rate. | Higher interest rates, limited to dealership inventory. |

| Online Subprime Lender | Medium to High | 12% - 29.9% | Convenient pre-approval process, can shop around. | Risk of predatory terms, initial offer may change. |

| Buy Here, Pay Here | Very High | 25% - 35%+ | Almost guaranteed approval. | Extremely high rates, older cars, may not report to credit bureaus. |

The 2026 Outlook: New Rules and Market Shifts Impacting Your Loan

The world of credit and lending is constantly evolving. Staying ahead of these changes can give you an edge in your application process. Here’s what to watch for in 2026 and beyond.

The FICO 10T & VantageScore 4.0 Effect

Newer credit scoring models are being adopted that look at "trended data." Instead of just a snapshot of your debt, they analyze your payment patterns over the last 24 months. This is great news for someone recovering from past mistakes. These models can give more weight to the fact that you've been making consistent payments recently, even if an old collection is still on your report. They may also treat paid collections more favourably than older models did.

Economic Headwinds

Interest rates across Canada have been a hot topic. As the central bank adjusts rates to manage the economy, the cost of borrowing for everyone is affected. For subprime borrowers, these shifts are magnified. It's crucial to understand that a rate that was considered high two years ago might be standard in the current market. The goal is to secure a loan to get you into a reliable vehicle, then focus on improving your credit to refinance for a better rate in 12-18 months.

Regulatory Scrutiny on Medical Debt

Consumer protection agencies are increasingly looking at how medical debt is reported and used in lending decisions. There is a growing movement to have paid medical collections removed from credit reports entirely. While not yet law in Canada, the trend is clear: lenders are already starting to place less emphasis on medical collections compared to other types of debt. This could make it significantly easier for those whose credit was damaged by unexpected health issues.

Pro Tip: Build Positive "Trended Data" Now

You can start preparing for these new scoring models today. Get a small, secured credit card and use it for one small recurring bill (like Netflix). Pay it off in full every single month. This creates a perfect, positive payment history that will carry significant weight in newer scoring algorithms, helping to offset the damage from older collections.

Your 30-Day Action Plan for Approval

Information is useless without action. Follow this weekly plan to transform your situation from "worried applicant" to "prepared buyer" in just one month.

Week 1: The Credit Audit

Your mission is to know your credit file better than the lender does. Pull your free reports from both Equifax and TransUnion. Do not rely on third-party apps; get the official reports. Identify every single collection account. Note its original creditor, the collection agency, the date it first went delinquent, and the balance. Dispute any and all errors immediately, no matter how small.

Week 2: The Strategic Strike

Look at the flowchart from Section 3. Analyze each collection on your report. Is it old and small? It might be best to leave it alone. Is it recent and from a financial institution? This may be one to address. If you decide to pay, always try to get a "paid in full" letter from the agency. Document every phone call, email, and letter. Having a record of your efforts shows initiative to a lender. For those who have gone through a formal process, remember that a car loan after a consumer proposal is very possible. Our team specializes in these situations, as detailed in our guide, Your Consumer Proposal? We Don't Judge Your Drive.

Week 3: The 'Proof Packet' Assembly

Gather the ultimate proof of your stability. This isn't just about what the lender asks for; it's about anticipating their questions. Your packet should include:

- 3 most recent pay stubs.

- Your last 2 years of T4s or Notice of Assessments.

- A utility bill or cell phone bill in your name for proof of address.

- 3 months of complete bank statements.

- A void cheque or direct deposit form.

Week 4: The Application Gauntlet

Start smart. Consider applying for a pre-approval from your own credit union or a reputable online lender first. This gives you a baseline. Then, walk into a dealership's special finance department with your "Proof Packet" and your pre-approval offer in hand. You are no longer just an applicant; you are a prepared consumer negotiating from a position of strength and transparency.