Approval Secrets: How International Students Get Car Loans in Ontario

Table of Contents

- Key Takeaways

- Understanding Your Eligibility: The Legal and Financial Baseline

- The Study Permit Requirement: Matching Loan Terms to Your Stay

- Age Requirements: Ontario’s 'Age of Majority'

- Income Sources: Can Part-Time Work Qualify You?

- The Car Loan Application for International Students in Ontario: A Step-by-Step Roadmap

- Phase 1: Preparation and Document Gathering

- Phase 2: Choosing Between Bank Financing and Dealership Financing

- Phase 3: The Pre-Approval Process

- Decoding the Credit Score Dilemma

- Why 'No Credit' is an Opportunity in Ontario

- Leveraging Newcomer Programs

- How to Build 'Shadow Credit'

- Budgeting for the 'Total Cost of Ownership' (TCO) in Ontario

- Interest Rates and the HST Impact

- Maintenance and Ontario's Climate

- Navigating Ontario Car Insurance: The Silent Approval Killer

- The GTA vs. Smaller Towns

- Leveraging Home Country Experience

- Choosing the Right Vehicle for Approval

- New vs. Used: The Great Debate

- Reliability Ratings and the 'Lien'

- Dealership Secrets: How to Spot Student-Friendly Lot Owners

- 'Buy Here, Pay Here' vs. Traditional Dealerships

- Negotiating the 'Out-the-Door' Price

- The Role of a Co-signer: Is it Necessary?

- Common Pitfalls and How to Avoid Them

- Driving Toward Your Future

- Frequently Asked Questions (FAQ)

- Can I get a car loan if my study permit expires in 12 months?

- Do I need an Ontario Driver’s License, or is an International License enough?

- What is the average interest rate for international students in Ontario?

- Can I take the car to another province if I move for a co-op term?

- Does RBC really offer loans with no Canadian credit history?

Stepping off the plane at Pearson International Airport is the beginning of a massive adventure. You’ve secured your spot at a world-class institution like the University of Toronto, McMaster, or Western. But reality sets in quickly: Ontario is vast. Whether you are commuting from Mississauga to a campus in downtown Toronto or navigating the winter slush in London, relying solely on public transit can turn a 20-minute trip into a two-hour ordeal. You need a car. But as an international student, the path to vehicle ownership often feels blocked by a wall of "No's" from traditional lenders.

The truth? Getting a car loan in Ontario as a non-resident isn't just possible—it’s a well-trodden path. The "secrets" to approval aren't about magic; they are about understanding how Canadian financial institutions assess risk and how you can position your profile to be the "safe bet" they are looking for. This guide pulls back the curtain on the Ontario automotive lending landscape, giving you the exact blueprint to go from a bus pass to a driver’s license.

Key Takeaways

- The Golden Rule: Your loan term must almost always end before your study permit expires. If you have two years left on your permit, don't apply for a five-year loan.

- No Credit ≠ Bad Credit: Major Canadian banks (RBC, Scotiabank, etc.) have specific "Newcomer" programs that treat a lack of Canadian credit history as a neutral starting point rather than a negative one.

- Skin in the Game: A down payment of 10% to 20% is the most effective way to bypass strict income requirements and lower your interest rates.

- The Insurance Hurdle: In Ontario, insurance is often more expensive than the car payment itself for young drivers. Budgeting for this is critical for long-term approval.

- Documentation is King: Having your Letter of Enrollment, Study Permit, and bank statements organized is 50% of the battle.

Understanding Your Eligibility: The Legal and Financial Baseline

Before you even browse an online inventory, you need to know where you stand legally. Lenders in Ontario operate under strict provincial regulations, and they have specific criteria for non-permanent residents. You aren't just a student to them; you are a "temporary resident," and that classification dictates the rules of the game.

The Study Permit Requirement: Matching Loan Terms to Your Stay

This is the single most common reason for rejection. A bank will rarely issue a loan that outlasts your legal right to be in the country. If your study permit expires in 36 months, your loan term should ideally be 24 to 30 months. Lenders fear that if your permit expires and you leave Canada, they will have no way to collect the remaining balance. When planning your purchase, look at your permit’s expiry date first, as it dictates your monthly budget more than the car's price does.

Age Requirements: Ontario’s 'Age of Majority'

In Ontario, you must be 18 years old to enter into a legally binding contract. If you are a 17-year-old freshman, you cannot legally sign a car loan or an insurance policy. In these cases, you would require a legal guardian or a co-signer who meets the age and residency requirements to hold the loan in their name until you reach the age of majority.

Income Sources: Can Part-Time Work Qualify You?

Can you get a loan on a part-time salary? Yes, but there are caveats. Most lenders want to see a minimum monthly income of $1,500 to $2,000. While your primary focus is your studies, the 20 or 40 hours you are permitted to work per week (depending on current federal regulations) are vital. However, lenders also recognize GIC (Guaranteed Investment Certificate) funds. If you can show that you have a significant sum of money set aside for living expenses, it acts as a secondary layer of security for the bank.

The Car Loan Application for International Students in Ontario: A Step-by-Step Roadmap

The process of getting a car is a marathon, not a sprint. Jumping straight to the dealership without preparation often leads to high-interest predatory loans. Follow this phase-based approach to ensure you get the best terms possible.

Phase 1: Preparation and Document Gathering

You need to prove four things: who you are, why you are here, where you live, and how you pay. Collect your valid Study Permit, a Letter of Enrollment from your Registrar’s office, your Social Insurance Number (SIN), and at least three months of Canadian bank statements. You will also need an Ontario Driver’s License. While an International Driver’s Permit (IDP) allows you to drive, most lenders require a provincial license to finalize a lien on a vehicle.

Phase 2: Choosing Between Bank Financing and Dealership Financing

Banks offer lower rates but have stricter "Newcomer" criteria. Dealerships (especially those with dedicated finance departments) have more flexibility but may charge higher interest. If you have a solid relationship with a bank like RBC or CIBC, start there. If they say no, a reputable dealership that works with multiple lenders is your next best bet.

Phase 3: The Pre-Approval Process

Never shop for a car without a pre-approval. This tells you exactly how much you can spend and what your interest rate will be. It prevents the "heartbreak" of falling in love with a car you can't afford. Pre-approval also gives you leverage when negotiating the price of the vehicle.

Decoding the Credit Score Dilemma

You’ve likely heard that you need a "good credit score" to buy anything in Canada. This is a half-truth. While a 750 score gets you the best rates, having *no* credit is significantly better than having *bad* credit. Lenders view a blank slate as an opportunity, whereas a history of missed payments is a red flag.

Why 'No Credit' is an Opportunity in Ontario

Ontario’s financial ecosystem is designed to integrate newcomers. Banks understand that an international student arriving from Mumbai, Beijing, or Lagos won't have a TransUnion or Equifax report yet. Instead of looking at a score, they look at "alternative data." This includes your banking history, the prestige of your university, and your field of study. Engineering and medical students, for example, are often viewed as lower risk due to their high future earning potential.

Leveraging Newcomer Programs

The 'Big Five' banks (RBC, TD, Scotiabank, BMO, CIBC) all have departments dedicated to newcomers and international students. These programs often waive the requirement for a Canadian credit history if you meet certain down payment thresholds. They are essentially betting on your future success in Canada.

How to Build 'Shadow Credit'

While they don't always show up on your official credit score immediately, things like your phone bill (Bell, Rogers, Telus) and your rent payments matter. If a lender is on the fence about your car loan, providing proof of a year’s worth of on-time rent and utility payments can act as "Shadow Credit," proving your reliability as a borrower.

Budgeting for the 'Total Cost of Ownership' (TCO) in Ontario

The sticker price of the car is just the beginning. In Ontario, the costs of keeping a car on the road are substantial, and failing to account for them is how many students end up in financial distress.

| Cost Category | Estimated Monthly/Annual Cost | Notes for Students |

|---|---|---|

| Loan Payment | $350 - $600 | Depends on the car price and interest rate. |

| Insurance | $250 - $500 | Extremely high for drivers under 25 in the GTA. |

| Fuel | $150 - $300 | Fluctuates based on global oil prices and commute. |

| Maintenance | $50 - $100 | Oil changes, brakes, and unexpected repairs. |

| Winterization | $800 (One-time) | Winter tires are essential for Ontario safety. |

Interest Rates and the HST Impact

What is a "fair" rate? For a student with no credit, expect anywhere from 7.9% to 15.9%. While this seems high compared to the 0% or 1.9% ads you see on TV, those rates are reserved for Tier 1 credit holders. Additionally, remember that Ontario has a 13% Harmonized Sales Tax (HST). If you buy a car for $20,000, you are actually financing $22,600. This "tax hit" can push your monthly payments higher than you initially calculated.

Maintenance and Ontario's Climate

Ontario winters are brutal on vehicles. Salt used on the roads causes rust, and extreme cold drains batteries. When budgeting, you must factor in the cost of a set of winter tires. Many insurance companies in Ontario offer a small discount if you use winter tires, but the upfront cost is usually around $800 to $1,200 for a decent set on rims. This is not an "optional" expense if you value your safety.

Navigating Ontario Car Insurance: The Silent Approval Killer

You can get approved for a car loan and still be unable to take the car home. Why? Because you cannot legally drive a car off a dealership lot in Ontario without proof of insurance. For international students, insurance is often the most difficult part of the equation.

The GTA vs. Smaller Towns

Where you live in Ontario drastically changes your insurance costs. If you are a student at York University living in Brampton or North York, your insurance could be double what a student at Queen’s University pays in Kingston. Brampton, in particular, has some of the highest insurance rates in North America. If you are on a tight budget, consider living in a slightly different postal code to save thousands per year in premiums.

Leveraging Home Country Experience

Standard Ontario insurance companies treat you as a "new driver" with zero years of experience, regardless of how long you drove back home. However, some companies will give you "experience credits" if you can provide an official Letter of Experience from your previous insurance provider (in English or professionally translated) and a certified driving record from your home country's licensing authority. This can potentially save you $100 or more per month.

Choosing the Right Vehicle for Approval

Not all cars are created equal in the eyes of a bank. If you are asking for a loan, the bank wants to know that if you stop paying, they can sell the car and get their money back. This is why your choice of vehicle directly impacts your approval odds.

New vs. Used: The Great Debate

New cars are easier to finance because they have a predictable value and come with warranties. Banks love new cars. However, the depreciation is massive. Used cars (3-5 years old) are the "sweet spot" for students. They have already lost their initial value but are still reliable enough for a lender to feel secure. Avoid cars older than 10 years or with over 150,000 kilometres, as many banks simply won't finance them.

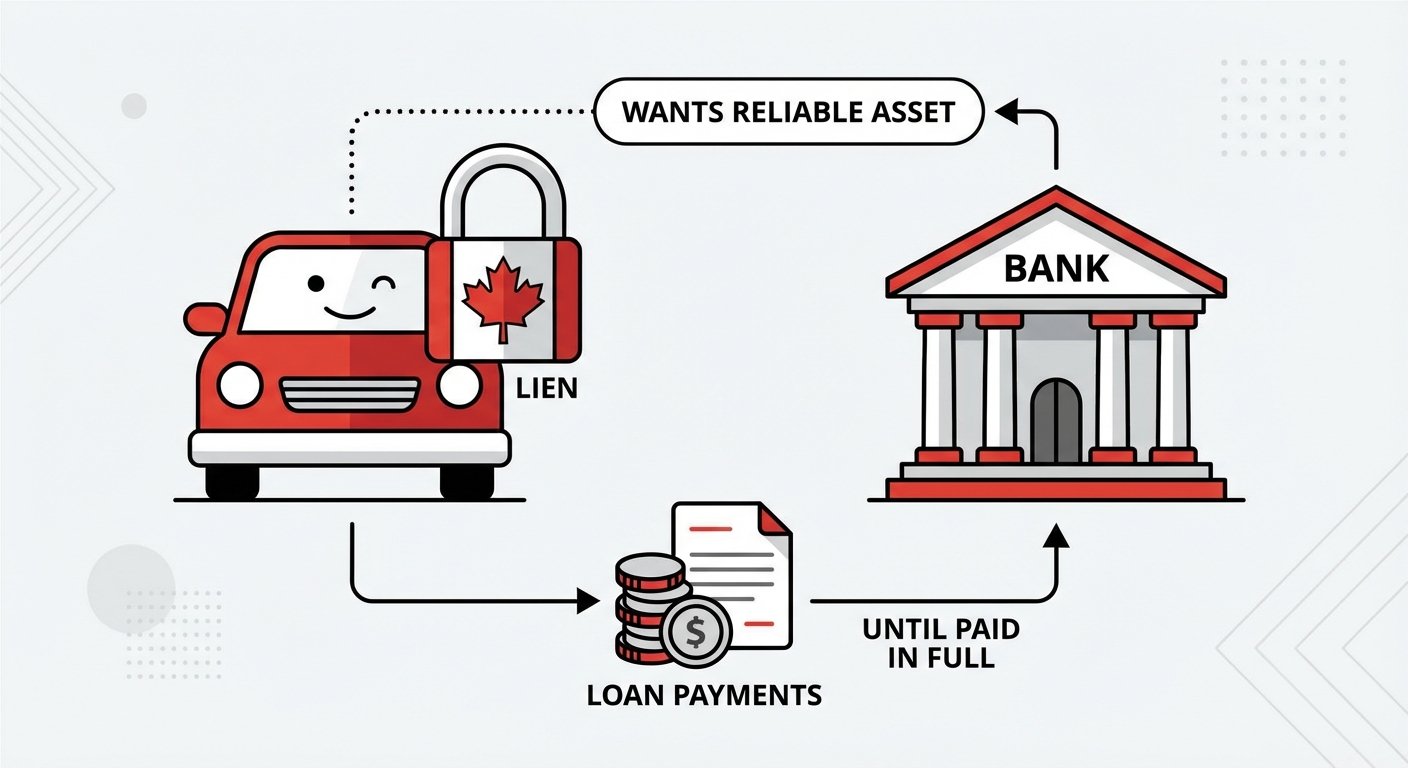

Reliability Ratings and the 'Lien'

Lenders prefer "Standard" brands like Honda, Toyota, and Mazda. These cars hold their value incredibly well. If you try to finance a 10-year-old luxury BMW, the bank sees a high risk of expensive repairs that might cause you to stop making your loan payments. When you finance a car, the bank places a "lien" on it. This means they technically own a portion of the vehicle until the last cent is paid. They want that asset to be as reliable as possible.

Dealership Secrets: How to Spot Student-Friendly Lot Owners

The Ontario used car market is diverse, ranging from massive corporate franchises to small "corner lot" operations. Knowing where to shop is as important as knowing what to buy.

'Buy Here, Pay Here' vs. Traditional Dealerships

You will see signs saying "No Credit? No Problem! Everyone Approved!" These are often "Buy Here, Pay Here" lots. They act as the lender themselves. While they are easy to get approved at, the interest rates are often astronomical (20-30%), and the cars may not be in the best condition. It is almost always better to go to a traditional dealership that works with major banks or established automotive finance companies.

Negotiating the 'Out-the-Door' Price

Dealerships often try to focus the conversation on the "weekly payment" to distract you from the total price. Always ask for the "Out-the-Door" (OTD) price, which includes the car price, HST, and all fees. Watch out for "Admin Fees" or "Documentation Fees" exceeding $500. While some fees are standard, others are just pure profit for the dealer. As an international student, you have the right to ask for a breakdown of every single charge.

The Role of a Co-signer: Is it Necessary?

If your income is too low or your study permit is too short, a lender might ask for a co-signer. This is a Canadian Citizen or Permanent Resident who agrees to take responsibility for the loan if you fail to pay.

Having a co-signer is the "fast track" to the lowest interest rates. However, it is a massive legal responsibility for the other person. If you miss a payment, *their* credit score is damaged. If you move back to your home country and stop paying, the bank will legally pursue the co-signer for the full amount. Because of this, most students only use family members or very close family friends as co-signers. If you don't have one, don't worry—most "Newcomer" programs are designed specifically for people in your exact situation.

Common Pitfalls and How to Avoid Them

The excitement of getting your first car in Canada can lead to some expensive mistakes. Here is how to stay protected:

- The 96-Month Trap: Dealers might offer you an 8-year loan to make the monthly payment look tiny. Never do this. You will end up owing far more than the car is worth (Negative Equity) within a year.

- Ignoring the Fine Print: Some loans have "Pre-payment Penalties." You want a loan that allows you to pay it off early without any fees. This is crucial if you decide to sell the car before you graduate.

- Skipping the Pre-Purchase Inspection (PPI): If buying used, always have an independent mechanic look at the car. A $150 inspection can save you $5,000 in engine repairs later.

Driving Toward Your Future

Owning a car in Ontario is about more than just getting from point A to point B. It is about freedom, the ability to take on better-paying co-op jobs in different cities, and the chance to explore the incredible landscapes of the Great Lakes region. By understanding the interplay between your study permit, the banking "Newcomer" programs, and the realities of Ontario insurance, you can navigate the financing process with confidence. Start early, keep your documentation organized, and remember: every on-time payment you make is a brick in the foundation of your future Canadian credit history. You aren't just buying a car; you are building a life here.

Frequently Asked Questions (FAQ)

Can I get a car loan if my study permit expires in 12 months?

It is difficult but not impossible. Most major banks will not issue a traditional loan for such a short duration. Your best options would be a short-term lease take-over, purchasing a reliable "cash car" (a cheaper vehicle paid in full), or finding a lender that specializes in short-term high-interest financing. Generally, lenders want at least 24 months of remaining time on a permit.

Do I need an Ontario Driver’s License, or is an International License enough?

While you can legally drive with an International Driver's Permit (IDP) for a short period, you almost certainly need an Ontario G2 or G license to get a car loan and insurance. Lenders and insurance companies require a provincial license to register the lien and the policy. If you haven't started the process, visit a DriveTest centre as soon as possible.

What is the average interest rate for international students in Ontario?

For students with no Canadian credit history, interest rates typically range between 8% and 15%. If you have a co-signer with excellent credit, you could see rates as low as 5% to 7%. Rates vary based on the age of the vehicle and the specific "Newcomer" program you qualify for.

Can I take the car to another province if I move for a co-op term?

Yes, but you must notify your insurance company and the lender. Different provinces have different insurance requirements and tax laws. If your move is permanent, you will eventually need to register the vehicle in your new province and update your driver's license, but for a 4-month co-op, your Ontario registration is usually sufficient as long as your insurance company is aware.

Does RBC really offer loans with no Canadian credit history?

Yes, RBC (and several other major banks like Scotiabank and CIBC) has a specific "Newcomer to Canada" program. These programs are designed for people who have been in the country for less than 3-5 years. They focus more on your down payment, your income/savings, and your legal status rather than a traditional credit score.