Self-Employed? Your Bank Doesn't Need a Resume.

Table of Contents

- Key Takeaways: Your Fast Track to Self-Employed Car Loan Success

- The Entrepreneurial Roadblock: Why Traditional Loans Fail the Self-Employed

- Beyond the Pay Stub: What 'No Income Verification' *Really* Means for Self-Employed Car Loans

- Your Bank Statements: The True Pulse of Your Business

- Tax Returns: Your Annual Financial Report Card

- Business Documentation: Proving Legitimacy and Longevity

- The Unseen Pillars: Credit Score and Down Payment

- The Lender Landscape: Navigating Your Options for a Self-Employed Car Loan

- Dealership Financing: Convenience vs. Cost

- Online Lenders & Fintech Platforms: Speed, Specialization, and Streamlined Processes

- Credit Unions: Relationship Banking and Member Benefits

- Traditional Banks: The Gold Standard (If You Fit the Mold)

- Specialty Lenders & High-Risk Financing: When All Else Fails

- Crafting Your Financial Narrative: Building an Irresistible Application

- Credit Score Mastery: Your Unofficial Co-Signer

- The Power of the Down Payment: De-Risking Your Application

- Showcasing Stability: Consistency in a Variable World

- Debt-to-Income Ratio for the Self-Employed: A Different Calculation

- Rates, Terms, and the Fine Print: What to Expect and How to Negotiate

- Understanding Your Interest Rate: The Cost of Doing Business

- Navigating Loan Terms: Short vs. Long-Term Implications

- Unmasking Hidden Fees and Clauses

- The Art of Negotiation: Securing Your Best Deal

- Common Pitfalls to Avoid on Your Self-Employed Car Loan Journey

- The Allure of 'Guaranteed Approval' Scams

- Overlooking Your Financial Health: Buying More Car Than You Can Afford

The traditional W-2 employee sails through car loan applications with pay stubs and employment letters, often with little more than a quick verification call. But for the self-employed, the road to a new vehicle often feels like a winding maze of skepticism, outdated requirements, and frustrating rejections. Are you a freelancer, a small business owner, or a gig economy worker who's been told your income isn't "stable" enough? Have you felt invisible to lenders because your paycheque doesn't arrive on a predictable bi-weekly schedule?

This deep dive shatters the myth that a steady, salaried paycheck is your only ticket to a new car in Canada. We're here to reveal how you can secure a car loan even if you don't have traditional pay stubs – often referred to as a "car loan for self-employed no income verification." But let's be clear: "no income verification" is a misleading phrase. Lenders always verify your ability to pay. What it truly means for you, the entrepreneur, is securing financing with *alternative* income verification that speaks your entrepreneurial language, showcasing your resilience, ingenuity, and consistent cash flow. Your bank might not need a resume, but they absolutely need your compelling financial story.

Key Takeaways: Your Fast Track to Self-Employed Car Loan Success

- 'No Income Verification' is a Misnomer: Lenders *always* verify financial stability. For self-employed individuals, this means looking beyond pay stubs to bank statements, tax returns, and a robust business history.

- Your Story is Your Strength: Frame your fluctuating income not as a liability, but as a sign of entrepreneurial resilience. Back this narrative with consistent cash flow, solid financial planning, and clear documentation.

- Credit Score is King (and Queen): A robust personal and, if applicable, business credit score is your most powerful asset when traditional income proof is scarce. It demonstrates your reliability as a borrower.

- Diverse Lender Landscape: Don't limit yourself to traditional banks. Dealerships, online lenders, and credit unions often have more flexible, understanding programs tailored for the self-employed.

- Preparation is Paramount: Gather comprehensive financial documents, even if not explicitly requested. Proactively demonstrating stability and repayment capacity can significantly boost your application.

- Down Payment Power: A significant down payment can dramatically offset perceived risk, opening doors to better rates and more favourable terms. It shows you have "skin in the game."

The Entrepreneurial Roadblock: Why Traditional Loans Fail the Self-Employed

For decades, car loan applications were meticulously designed for the salaried employee. Think about it: a steady job, bi-weekly pay stubs, an employment letter confirming your position and salary. This clear-cut proof of income provides a predictable, easily verifiable snapshot of your financial health, making you a low-risk borrower in the eyes of traditional lenders.

But what happens when your income isn't a fixed, consistent number? For the millions of Canadians who are freelancers, small business owners, contractors, or gig economy workers, the standard "proof of income" creates an immediate, often insurmountable, hurdle. Your income might fluctuate month-to-month, you might strategically write off business expenses to reduce taxable income, or your business might be too new to have years of audited financial statements.

From a lender's perspective, this variability translates into perceived "risk." They worry about your ability to consistently make payments if your income isn't guaranteed. Common misconceptions exacerbate this: lenders might assume that because your net taxable income is low (due to smart write-offs), your actual cash flow is insufficient. They may not understand the cyclical nature of certain industries or the unique financial rhythm of a thriving small business. This misunderstanding often leads to outright rejection, or, perhaps worse, offers with exorbitant interest rates and unfavourable terms, simply because your financial reality doesn't fit their rigid, outdated boxes.

The system wasn't built for you, the entrepreneur, but that doesn't mean you can't navigate it successfully. It just means you need to present your financial story in a language they understand, using the tools and documents that truly reflect your solvency and capability.

Beyond the Pay Stub: What 'No Income Verification' *Really* Means for Self-Employed Car Loans

The phrase "no income verification" is one of the most misunderstood terms in the world of self-employed financing. It conjures images of walking into a dealership, pointing at a car, and driving off without anyone asking about your finances. That's a myth. In reality, it doesn't mean a free pass; it means a *different* kind of verification. Lenders are still assessing your ability to repay the loan, but they're willing to look beyond the traditional W-2 or employment letter to understand your true financial picture. They want to see consistent cash flow and a history of responsible financial management, even if it's not neatly packaged in a bi-weekly stub.

This section demystifies the alternative documentation lenders scrutinize when a W-2 isn't available. We'll break down the specific financial documents that tell your income story, even if it's not a perfectly linear one, and how to present them effectively.

Your Bank Statements: The True Pulse of Your Business

Forget the pay stub – your bank statements are your most candid financial diary. For self-employed individuals, lenders will conduct a detailed analysis of both your personal and, if you have one, your business bank accounts. What exactly are they looking for? They want to see consistent deposits, indicating steady income streams, even if the amounts vary. They'll scrutinize your positive cash flow, ensuring that money is regularly coming in and that you're not consistently overdrawing or running on fumes. Managing expenses responsibly is also key; erratic spending or frequent non-sufficient funds (NSF) charges are major red flags.

Typically, lenders will request 6 to 12 months of bank statements. The more consistent and healthy your cash flow appears over this period, the stronger your application will be. To present them effectively, ensure your statements are clear, well-organized, and ideally show a healthy balance. If you have a dedicated business account, even better, as it clearly separates your personal and professional finances, making it easier for a lender to track business income. For more on this, check out our guide on Self-Employed? Your Bank Account *Is* Your Proof. Get Approved.

Tax Returns: Your Annual Financial Report Card

Your annual tax returns, specifically your T1 General and any relevant schedules like the T2125 Statement of Business or Professional Activities, serve as your annual financial report card. Lenders understand that self-employed individuals often use legitimate deductions to reduce their taxable net income. However, they need to see enough net income to comfortably cover your proposed car loan payments along with your other living expenses.

The importance of showing net income, even after aggressive deductions, cannot be overstated. While minimizing taxes is smart, reporting a net income that appears too low can hinder your loan approval. Lenders typically prefer to see at least two years of tax returns, as this demonstrates longevity and a consistent track record of earning. Multiple years help them average out any fluctuations and establish a more reliable income trend. Be prepared to explain any significant drops or spikes in income, providing context that reinforces your financial stability.

Business Documentation: Proving Legitimacy and Longevity

Beyond bank statements and tax returns, a suite of business documentation can significantly bolster your application, proving legitimacy and longevity. This can include your business registration and licensing, professional invoices demonstrating client work, long-term contracts with clients, or even a robust business plan. These documents paint a picture of an active, stable, and ongoing enterprise, reducing perceived risk.

A common question is: how long do you need to be self-employed to qualify? Most traditional lenders prefer to see at least two years of self-employment history, backed by two years of tax returns. However, some specialty lenders or credit unions may be more flexible, considering individuals with 6-12 months of consistent income, especially if combined with a strong credit score and a substantial down payment. The longer your verifiable history, the stronger your position.

The Unseen Pillars: Credit Score and Down Payment

When traditional income proof is less straightforward, your personal credit score becomes exponentially more critical. It acts as an unofficial co-signer, telling lenders about your history of responsible borrowing and repayment. A high credit score (generally 680 or above) signals reliability and can compensate for the perceived variability of self-employed income. It assures lenders that even if your monthly income fluctuates, you are diligent in meeting your financial obligations.

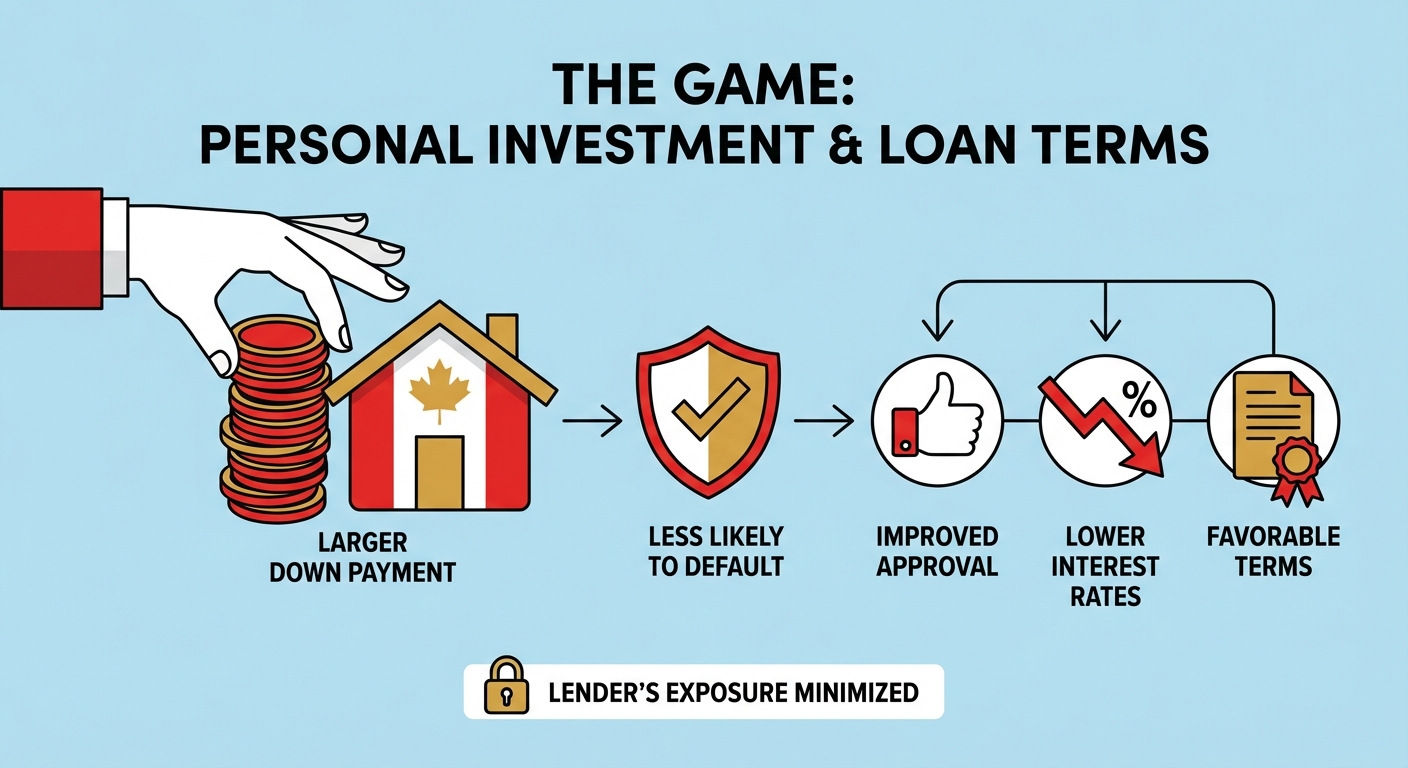

Equally powerful is the role of a substantial down payment. This isn't just about reducing the amount you need to borrow; it's about reducing lender risk. By putting down a significant portion of the car's value, you demonstrate "skin in the game" – a personal investment that makes you less likely to default on the loan. A larger down payment can improve your chances of approval, lead to lower interest rates, and secure more favourable terms, as the lender's exposure is minimized.

The Lender Landscape: Navigating Your Options for a Self-Employed Car Loan

Not all lenders are created equal, especially when it comes to financing for the self-employed. Understanding the diverse landscape of financial institutions and platforms is crucial for finding the right fit for your unique situation. Each type of lender has its own typical requirements, advantages, and disadvantages for entrepreneurs seeking a car loan.

Dealership Financing: Convenience vs. Cost

Dealership financing offers the ultimate 'one-stop shop' appeal. You choose your car, negotiate the price, and often secure financing all in the same location. Dealerships work with a network of lenders, including captive lenders (e.g., Ford Credit, Honda Financial Services) and indirect lenders (banks, credit unions). Many dealerships have experience working with self-employed applicants and may have specific programs designed for them. The convenience can be appealing, and sometimes, they can offer 'easy approval' due to their volume relationships with various lenders.

However, this convenience can sometimes come at a cost. While dealerships aim to get you approved, they might not always offer the absolute best rates initially. It's crucial to remember that dealerships have multiple lenders in their network, and their first offer might not be their best. Always be prepared to negotiate.

Online Lenders & Fintech Platforms: Speed, Specialization, and Streamlined Processes

The digital age has brought a significant rise in online lenders and Fintech platforms, many of which specialize in non-traditional applicants, including the self-employed. These platforms often leverage advanced algorithms to assess creditworthiness, allowing them to consider a broader range of financial data beyond just pay stubs. Advantages include quick pre-approvals, streamlined application processes, and diverse product offerings designed for varied financial situations.

Online lenders can be a great option for speed and convenience, often providing decisions within minutes. However, it's crucial to vet reputable platforms to avoid scams or predatory lenders. Look for transparent terms, clear contact information, and positive customer reviews. These lenders are often more accustomed to the nuances of self-employed income and may offer more flexible documentation requirements.

Credit Unions: Relationship Banking and Member Benefits

Credit unions can be a powerful ally for the self-employed. Unlike large banks, credit unions are member-owned and community-focused. This often translates into a more personalized approach to lending. They are frequently more willing to look beyond strict, standardized criteria and consider your individual circumstances and financial story. If you're an existing member with a good banking relationship, they might be more flexible with income verification or offer more favourable rates for members.

The importance of establishing a banking relationship with a credit union cannot be overstated. If your business banking or personal accounts are already with a credit union, they'll have a better understanding of your financial patterns and be more inclined to work with you on a car loan.

Traditional Banks: The Gold Standard (If You Fit the Mold)

While often the most stringent and traditional in their requirements, major banks can offer the best interest rates if you meet their (often higher) bar for self-employed applicants. If you have a long, stable history of self-employment (typically 2+ years of consistent, high net income on your tax returns) and an excellent credit score, your primary bank might be your best bet. They may prefer to see significant assets and a very clear separation of business and personal finances. It makes sense to approach your primary bank if you have a strong existing relationship and believe you meet their conservative criteria, as they may offer competitive rates and terms.

Specialty Lenders & High-Risk Financing: When All Else Fails

For self-employed individuals with credit challenges, a shorter business history, or very inconsistent income, specialty (or subprime) lenders play a crucial role. These lenders cater to higher-risk profiles and are often more willing to approve loans where traditional banks or credit unions might decline. While they offer a path to vehicle ownership, it's crucial to understand that their interest rates will be significantly higher to compensate for the increased risk. Their terms may also be stricter, with shorter repayment periods or larger down payment requirements.

Navigating these options responsibly means understanding the true cost of the loan. While they can provide a necessary stepping stone, the goal should be to improve your financial standing over time to qualify for better rates in the future. Always compare the Annual Percentage Rate (APR), not just the monthly payment, to understand the true cost of the loan over its lifetime.

Here's a quick comparison of lender types for self-employed individuals:

| Lender Type | Pros for Self-Employed | Cons for Self-Employed | Typical Requirements |

|---|---|---|---|

| Dealership Financing | Convenience, access to multiple lenders, experience with varied profiles. | Rates may not always be the lowest, potential for upselling. | Variable (depends on specific lender in their network), generally flexible. |

| Online Lenders & Fintech | Speed, specialized algorithms, broader acceptance criteria, streamlined process. | Less personal interaction, need to vet reputation, rates can vary widely. | Bank statements, tax returns (sometimes), credit score focus. |

| Credit Unions | Relationship-focused, flexible criteria, often better rates for members. | May require membership, can be slower than online lenders. | Bank statements, tax returns, existing member relationship helps. |

| Traditional Banks | Potentially lowest rates if approved, established reputation. | Most stringent requirements, often prefer 2+ years of high net income. | Detailed tax returns (2+ years), strong credit, clear business financials. |

| Specialty Lenders | Higher approval rates for challenging profiles, last resort option. | Significantly higher interest rates, stricter terms, potential for fees. | Focus on current income/cash flow, may accept shorter self-employment history. |

Crafting Your Financial Narrative: Building an Irresistible Application

Getting a car loan as a self-employed individual isn't just about handing over documents; it's about telling a compelling financial story. You need to present yourself as a reliable and capable borrower, even without the conventional salary that traditional lenders are accustomed to. This involves strategic preparation and a deep understanding of what lenders truly value.

Credit Score Mastery: Your Unofficial Co-Signer

Your credit score is arguably your most powerful asset when applying for a self-employed car loan. It acts as an unofficial co-signer, providing a universally understood measure of your financial reliability. A strong credit score (generally 680 or higher) can significantly mitigate the perceived risk of variable income, demonstrating that you are responsible with debt. For more insights into what score you might need, you can read The Truth About the Minimum Credit Score for Ontario Car Loans.

Actionable steps to improve your credit score include: consistently paying all your bills on time (every time!), reducing existing debt (especially high-interest credit card debt), and monitoring your credit report regularly for any errors or fraudulent activity. Understanding the factors that impact your score – payment history, amounts owed, length of credit history, new credit, and credit mix – empowers you to make informed decisions. A robust credit history can effectively compensate for income volatility, assuring lenders of your commitment to repayment.

The Power of the Down Payment: De-Risking Your Application

A larger down payment is not just a nice-to-have; it's a strategic move that significantly boosts your approval odds and can lead to lower interest rates. By investing your own capital upfront, you dramatically reduce the lender's risk. This "skin in the game" demonstrates your commitment to the purchase and your ability to save, both highly attractive qualities to lenders.

Strategies for saving for a substantial down payment might include setting aside a fixed percentage of every invoice, minimizing discretionary spending, or even selling an older vehicle. Understanding its impact on your loan-to-value (LTV) ratio is key: a lower LTV (meaning you're borrowing less relative to the car's value) makes you a much more appealing borrower and can unlock better terms.

Showcasing Stability: Consistency in a Variable World

Even if your monthly income fluctuates, demonstrating a consistent *pattern* of earnings over time is crucial. Lenders understand that self-employment isn't always linear. Highlight consistent client relationships, long-term contracts, recurring retainer agreements, or a solid track record of business longevity. If you've been in business for several years, emphasize that stability. A strong business plan outlining future projects, client pipelines, and revenue projections can also add significant weight to your application, especially if your business is newer. Your professional portfolio or testimonials can also subtly reinforce your value and stability.

Debt-to-Income Ratio for the Self-Employed: A Different Calculation

Your Debt-to-Income (DTI) ratio is a critical metric lenders use to assess your ability to manage monthly payments. For the self-employed, this calculation is often different and can be more complex. Lenders will typically use your gross income before many business deductions (or an average of your net income over several years) and compare it to your total monthly debt obligations (including the new car payment). Aggressive write-offs, while beneficial for taxes, can make your DTI appear higher than your actual cash flow would suggest.

Strategies for managing existing debt to present a healthier financial picture include paying down credit card balances, consolidating loans, or even delaying other major purchases until after your car loan is secured. Understanding how lenders calculate your DTI and proactively managing your debt can significantly improve your chances of approval. For those in Ontario, especially self-employed, navigating these options effectively is key, and you might find more tailored advice in resources like Approval Secrets: Navigating the Best Used Car Finance Options for Ontario’s Self-Employed.

Rates, Terms, and the Fine Print: What to Expect and How to Negotiate

Securing approval for a self-employed car loan is a significant achievement, but securing *favorable* terms is another beast entirely. This section delves into the specifics of interest rates, loan terms, and potential hidden costs, equipping you with the knowledge to negotiate confidently and avoid common pitfalls. Your goal isn't just to get approved; it's to get the best possible deal.

Understanding Your Interest Rate: The Cost of Doing Business

As a self-employed individual, you might face slightly higher interest rates compared to a traditionally employed person with an identical credit score. This is largely due to the perceived higher risk associated with fluctuating income. However, this isn't a foregone conclusion. Several factors influence your rate: your credit score (the higher, the better), the loan term (shorter terms often have slightly lower rates), the size of your down payment (larger down payments reduce risk and can lower rates), and the specific lender you choose.

It's crucial to understand the difference between the interest rate and the Annual Percentage Rate (APR). The interest rate is simply the cost of borrowing the principal. The APR, however, includes the interest rate plus any additional fees, providing a more comprehensive measure of the total annual cost of your loan. Always compare APRs when evaluating offers, as this gives you the true cost of borrowing.

Navigating Loan Terms: Short vs. Long-Term Implications

When financing a car, you'll be presented with various loan terms, typically ranging from 24 to 84 months (2 to 7 years). Each option comes with its own trade-offs. Shorter loan terms generally mean higher monthly payments but result in less interest paid over the life of the loan, allowing you to become debt-free faster. Longer loan terms, conversely, offer lower monthly payments, which can be appealing for managing cash flow, but you'll pay significantly more in total interest over the extended period.

Choosing a term that aligns with your business's cash flow and personal financial goals is paramount. If your business has strong, consistent cash flow, a shorter term might be preferable to save on interest. If your income is more variable, a slightly longer term with lower payments might provide more financial breathing room. However, be mindful of the total cost.

Unmasking Hidden Fees and Clauses

Beyond the interest rate, car loan agreements can sometimes contain various fees and clauses that can inflate the total cost. Be on the lookout for:

- Origination Fees: A charge for processing the loan.

- Documentation Fees: For preparing the paperwork.

- Prepayment Penalties: Fees if you pay off your loan early (less common in Canada, but always check).

- Late Payment Charges: Penalties for missed or delayed payments.

- Lien Registration Fees: For registering the lender's interest in the vehicle.

Read every line of your loan agreement meticulously. Don't hesitate to ask for clarification on any fee you don't understand. In some cases, certain fees (like documentation fees) might be negotiable, especially if you're a strong borrower or if you're comparing offers from multiple lenders. Knowing what to look for empowers you to identify these costs and, where possible, negotiate their removal or reduction.

The Art of Negotiation: Securing Your Best Deal

Negotiation is a skill that can save you thousands. Strategies for negotiating interest rates, loan terms, and even the car price itself are interconnected. Start by leveraging pre-approvals from multiple lenders. This not only confirms your eligibility but also gives you concrete offers to use as leverage. If a dealership knows you've been pre-approved at a certain rate, they're more likely to match or beat it to earn your business.

Know your budget inside and out, and stick to it. Be prepared to walk away if the terms aren't favourable. The power of being an informed consumer cannot be overstated. Research market rates for similar vehicles and for borrowers with your credit profile. Don't feel rushed or pressured. A confident, well-prepared approach will always yield better results. Remember, your financial health as a self-employed individual is unique, and you deserve a deal that respects your hard work and financial acumen. Even if you start with a higher rate, remember that refinancing is often an option to improve your terms later, as discussed in Approval Secrets: How to Refinance Your Canadian Car Loan with Bad Credit.

Common Pitfalls to Avoid on Your Self-Employed Car Loan Journey

The path to a self-employed car loan can have its unique challenges, and unfortunately, some pitfalls can derail your journey or lead to costly mistakes. Being aware of these common traps will help you make a smooth and financially sound purchase.

The Allure of 'Guaranteed Approval' Scams

Be extremely wary of any lender promising "guaranteed approval" or "no credit check" car loans, especially if they don't ask for any financial information. These are often red flags of predatory lenders or fraudulent schemes. No legitimate lender will offer a car loan without some form of financial assessment, even if it's alternative income verification. These offers typically come with exorbitant interest rates, hidden fees, and unfair terms that can trap you in a cycle of debt. Protect yourself by only dealing with reputable lenders, checking their reviews, and scrutinizing all terms before signing anything.

Overlooking Your Financial Health: Buying More Car Than You Can Afford

It's easy to get swept up in the excitement of a new vehicle and be tempted to buy a more expensive car than your cash flow can comfortably support. This is a common and costly mistake. Remember that a car loan payment is just one part of the total cost of car ownership. You also need to factor in insurance (which can be significantly higher for newer or luxury vehicles), maintenance, fuel, and potential repair costs. Create a realistic budget that accounts for all these expenses, ensuring your car