Post-Proposal Car Loan: Your Credit Score Just Got a Mulligan.

Table of Contents

- Post-Proposal Car Loan: Your Credit Score Just Got a Mulligan.

- Key Takeaways: Your Fast Track to a Post-Proposal Car Loan

- The Mulligan Moment: Reclaiming Your Driving Future After a Consumer Proposal

- From Financial Reset to Road Ahead: Understanding Your New Starting Line

- Decoding Your 'Post-Proposal' Credit Score: What Lenders *Really* See Now

- The Fading Shadow: How Your Consumer Proposal Appears (and Disappears) on Your Report

- Beyond the Score: What Other Data Points Lenders Scrutinize

- The Strategic Rebuild: Architecting a Stronger Credit Profile for Car Loan Success

- Secured Credit Cards: Your First Step Back to Credit Health

- Credit Builder Loans: A Calculated Boost for Your Payment History

- The Unsung Heroes: Utility Bills & Rent Reporting

- Avoiding New Credit Traps: Prudent Borrowing in Your Rebuilding Phase

- Timing is Everything: When to Hit the Gas on Your Car Loan Application

- The Sweet Spot: Months vs. Years Post-Discharge

- The Diminishing Impact: Why Patience Pays Dividends in Lower Rates

- Navigating the Lender Labyrinth: Who Will Say 'Yes' (and at What Cost)?

- Tier 1: Specialist Lenders for Post-Proposal Applicants (The 'Second Chance' Specialists)

- Tier 2: Credit Unions & Community Banks (Your Local Advantage)

- Tier 3: Dealership Financing – The Good, The Bad, and The Ugly

- Why Big Banks Remain a Challenge (Initially) – And How to Eventually Win Them Over

- Crafting Your Irresistible Application: Beyond the Credit Score

- The Down Payment Advantage: Lowering Lender Risk, Boosting Your Odds

- Income Stability & Employment History: Proving Your Capacity to Pay

- The Co-Signer Conundrum: When it Helps, When it Hurts (and How to Protect Them)

- Realistic Expectations: Choosing the Right Vehicle for Your Budget

- Documentation Deep Dive: What You *Must* Have Ready

- Beyond Approval: Smart Strategies for Your New Car Loan

Post-Proposal Car Loan: Your Credit Score Just Got a Mulligan.

Navigating life after a consumer proposal can feel like starting a new game with a few penalties still on the scoreboard. But when it comes to securing a car loan, that proposal isn't a game-ender; it's a strategic reset. At SkipCarDealer.com, we understand that a reliable vehicle isn't a luxury in Canada – it's often a necessity for work, family, and daily life. This isn't about dwelling on past financial challenges; it's about leveraging your "mulligan" – that fresh start – to rebuild your credit and get back on the road. This comprehensive guide will equip you with the knowledge and actionable steps to confidently secure a car loan post-consumer proposal. We'll demystify the credit landscape, reveal lender insights, and arm you with the strategies to drive away with a loan that supports your financial recovery, not hinders it.

Key Takeaways: Your Fast Track to a Post-Proposal Car Loan

- Patience is a Virtue (But Not Forever): While immediate approval *is* possible, waiting 6-12 months post-discharge to build positive credit can significantly improve your loan terms and interest rates.

- Rebuild Proactively: Actively use secured credit cards and consider credit builder loans immediately after your proposal is satisfied to demonstrate responsible payment behaviour.

- Know Your Credit Report: Regularly monitor your Equifax and TransUnion reports. Understand how your consumer proposal appears and, more importantly, when it will be removed.

- Focus on Stability: Lenders prioritize stable employment, consistent income, and a manageable debt-to-income ratio just as much, if not more, than your past credit events.

- Down Payment Power: A substantial down payment significantly reduces lender risk and can open doors to better rates and approval, even with a recovering credit score.

- Target the Right Lenders: Start with specialist lenders or credit unions who are more accustomed to working with post-proposal applicants, rather than major banks initially.

- Get Pre-Approved: Secure your financing *before* you step onto a dealership lot. This empowers you to negotiate and shop for a vehicle within your approved budget.

- Manage for the Long Term: Your first post-proposal car loan is a stepping stone. Make all payments on time, and plan to refinance for better rates once your credit improves further.

The Mulligan Moment: Reclaiming Your Driving Future After a Consumer Proposal

Life throws curveballs, and sometimes, those curveballs involve financial difficulty. A consumer proposal, in the Canadian context, is a formal, legally binding agreement made with your unsecured creditors to pay back a portion of what you owe. It's designed to help you avoid bankruptcy while providing a structured path to financial recovery. Crucially, once your consumer proposal is completed and discharged, it signifies a fresh start – your "mulligan." It’s an opportunity to rebuild, re-establish, and regain control of your financial narrative, including securing essential financing like a car loan. This isn't about being penalized for past struggles; it's about demonstrating your renewed commitment to financial responsibility.

From Financial Reset to Road Ahead: Understanding Your New Starting Line

Many people mistakenly believe that a consumer proposal is a life sentence of bad credit. While it certainly impacts your credit score and report, its purpose is to provide a foundation for rebuilding, not an ongoing penalty. Think of it this way: during your consumer proposal, your credit options are severely limited. Lenders see you as actively undergoing a debt repayment process under legal terms. However, once that proposal is *satisfied* and *discharged*, your situation fundamentally changes. You've fulfilled your obligations, and you're now standing on solid ground, ready to prove your creditworthiness anew. Your new starting line is defined by your discharge date – the moment you officially complete your proposal and are free from its terms. This distinction between "during" and "after" is crucial, as it dictates the types of financing available to you and the strategies you should employ.

Decoding Your 'Post-Proposal' Credit Score: What Lenders *Really* See Now

Your credit score is often the first thing lenders look at, but after a consumer proposal, it tells only part of the story. While your score will undoubtedly be lower immediately after discharge, lenders who specialize in non-prime financing understand the context. They're looking beyond just the three-digit number; they're scrutinizing your credit report for specific indicators of your current financial health and your commitment to rebuilding.

The Fading Shadow: How Your Consumer Proposal Appears (and Disappears) on Your Report

A consumer proposal will be listed on your credit report, specifically under the "R9" rating, indicating a major derogatory event. However, this isn't a permanent fixture. In Canada, a consumer proposal is typically removed from your credit report (both Equifax and TransUnion) either:

- Three years after the date you satisfied all the terms of your proposal, OR

- Six years after the date you filed your proposal.

Whichever of these two dates comes first is when the consumer proposal should disappear from your report. This timeline is critical. The further you are from your discharge date, and especially once the proposal is completely removed from your report, the less weight it carries with lenders. This gradual fading makes demonstrating positive payment history in the interim even more important.

Beyond the Score: What Other Data Points Lenders Scrutinize

While the R9 rating and your lower credit score are undeniable, savvy lenders – particularly those specializing in non-prime loans – look deeper. They want to see evidence of your *current* ability and willingness to pay. Key data points they scrutinize include:

- Payment History Since Proposal: This is paramount. Have you made all payments on any new credit (even small ones) on time and in full? This is your strongest indicator of renewed responsibility.

- Current Debt-to-Income (DTI) Ratio: Lenders assess how much of your gross monthly income is consumed by debt payments. A lower DTI indicates more disposable income available for a new car loan.

- Stability of Employment: A consistent job history, ideally with the same employer for a significant period (e.g., 2+ years), signals stable income.

- Income Level: Your verifiable income needs to be sufficient to comfortably cover the proposed car loan payments, along with your other living expenses.

- Residential Stability: Living at the same address for several years can also indicate overall stability and reliability.

- Other Assets: While less common for car loans, any other assets you possess can sometimes be viewed favourably.

These factors often weigh more heavily than the historical consumer proposal, especially once some time has passed since your discharge.

Pro Tip: The Power of Proactive Credit Monitoring Post-CP

Don't wait for a lender to tell you what's on your credit report. Take control! Regularly check your credit reports from both Equifax and TransUnion. In Canada, you are entitled to a free copy of your credit report annually from each bureau. Review it for accuracy, ensure your consumer proposal discharge is correctly noted, and track your progress as new positive accounts and payment histories begin to appear. Dispute any errors immediately. Knowing what lenders see puts you in a much stronger negotiating position.

The Strategic Rebuild: Architecting a Stronger Credit Profile for Car Loan Success

Securing a car loan after a consumer proposal isn't just about waiting; it's about actively rebuilding your credit profile. This strategic approach demonstrates to lenders that you are financially responsible and capable of managing new debt.

Secured Credit Cards: Your First Step Back to Credit Health

A secured credit card is one of the most effective tools for rebuilding credit after a consumer proposal. Here's how it works:

- You provide a cash deposit to the issuer, typically ranging from $200 to $1,000.

- This deposit becomes your credit limit.

- You use the card like a regular credit card, making small purchases.

- You make your payments on time and in full each month.

The key here is that your responsible usage (low utilization, on-time payments) is reported to the credit bureaus. This quickly builds a positive payment history, which is exactly what car lenders want to see. After 12-18 months of responsible use, many secured card issuers will offer to convert your card to an unsecured one and return your deposit.

Credit Builder Loans: A Calculated Boost for Your Payment History

Credit builder loans are another excellent tool. Unlike traditional loans where you receive the money upfront, with a credit builder loan:

- You apply for a small loan (e.g., $500 - $2,000).

- The funds are held in a locked savings account or GIC by the lender.

- You make regular payments (e.g., $50/month) over a set period (e.g., 12-24 months).

- Once the loan is fully repaid, the funds are released to you.

The benefit is that your consistent, on-time payments are reported to credit bureaus, demonstrating reliable payment behaviour for an installment loan – which is precisely what a car loan is. This type of loan, combined with a secured credit card, creates a diverse credit mix that lenders appreciate.

The Unsung Heroes: Utility Bills & Rent Reporting

Did you know your on-time rent and utility payments could help your credit? While not all landlords or utility companies report to credit bureaus by default, there are services available in Canada that can facilitate this. Companies like FrontLobby or Landlord Credit Bureau allow landlords to report tenant payment history to Equifax and TransUnion. Similarly, some utility providers may offer reporting or you can use third-party services that consolidate and report these payments. Inquire with your landlord or utility providers, or research these services, as consistent on-time payments for essential services can offer an alternative way to build positive history, especially if other credit options are initially limited.

Avoiding New Credit Traps: Prudent Borrowing in Your Rebuilding Phase

As you rebuild, it's crucial to avoid the temptation of taking on too much new debt too quickly. Each new credit application results in a "hard inquiry" on your credit report, which can temporarily lower your score. Furthermore, accumulating too much debt, even if you can manage the payments, will increase your debt-to-income ratio, making you appear riskier to car lenders. Focus on a few, well-managed accounts rather than many. Keep your credit utilization low on secured cards (ideally under 30% of your limit) and ensure every single payment is made on time.

Pro Tip: The Magic Number – Why a Diverse Credit Mix Matters (Responsibly)

Lenders like to see a diverse credit mix, which means having both revolving credit (like a secured credit card) and installment credit (like a credit builder loan). This shows you can handle different types of financial obligations. However, this only helps if you manage *all* accounts perfectly. Don't open multiple accounts just for the sake of diversity; focus on one or two that you can manage impeccably to build a solid foundation of positive payment history.

Here's a quick comparison of these credit-building tools:

| Feature | Secured Credit Card | Credit Builder Loan | Rent/Utility Reporting Services |

|---|---|---|---|

| Type of Credit | Revolving Credit | Installment Credit | Payment History (Non-Credit Account) |

| Initial Cost/Deposit | Required (becomes your limit) | No upfront deposit (funds held by lender) | Varies (monthly fee for service, or free if landlord reports) |

| How it Builds Credit | On-time payments, low utilization reported to bureaus. | Consistent, on-time payments reported to bureaus. | On-time payments for essential services reported to bureaus. |

| Access to Funds | Immediately, up to your deposit limit. | After full repayment of the loan. | No direct access to funds. |

| Best Use Case | Establishing initial credit history, demonstrating responsible revolving credit use. | Adding installment credit history, proving ability to make consistent payments over time. | Supplementing credit history, especially for those without traditional credit. |

Timing is Everything: When to Hit the Gas on Your Car Loan Application

The desire for a new vehicle can be strong, but strategic timing is paramount after a consumer proposal. While it's technically possible to get a loan soon after discharge, patience often pays significant dividends in the form of better interest rates and more favourable terms.

The Sweet Spot: Months vs. Years Post-Discharge

Immediately after your consumer proposal is discharged, your credit score will still reflect the impact. However, with active rebuilding strategies (secured cards, credit builder loans), you can start to see improvements within 6 to 12 months.

- 0-6 Months Post-Discharge: Approval is possible, but you'll likely face the highest interest rates and may require a larger down payment or co-signer. Options might be limited to specialist lenders.

- 6-12 Months Post-Discharge: With a few months of positive payment history under your belt, your approval odds improve, and you might qualify for slightly better rates. This is often a good "first step" if a vehicle is immediately necessary.

- 1-2 Years Post-Discharge: This is often the "sweet spot." If you've diligently rebuilt your credit during this period, your score will have significantly improved, and the consumer proposal will carry less weight. You'll likely qualify for more competitive rates and have more lender options.

- 2+ Years Post-Discharge: The longer you go with perfect payments and active credit rebuilding, the more the impact of the consumer proposal fades. You'll be closer to qualifying for prime rates and have access to a wider range of lenders.

For more insights on how soon you can get a loan, check out our guide on Discharged? Your Car Loan Starts Sooner Than You're Told.

The Diminishing Impact: Why Patience Pays Dividends in Lower Rates

Every month that passes after your consumer proposal discharge, and every on-time payment you make, serves to push the negative impact of the proposal further into your credit history. Lenders use algorithms and human review to assess risk. As more positive data points accumulate, the "risk" associated with your past proposal diminishes. This directly translates to lower interest rates. A lender's interest rate is a reflection of the perceived risk of lending to you. By patiently building a solid credit foundation, you effectively reduce that perceived risk, making yourself a more attractive borrower and saving yourself potentially thousands of dollars in interest over the life of the loan.

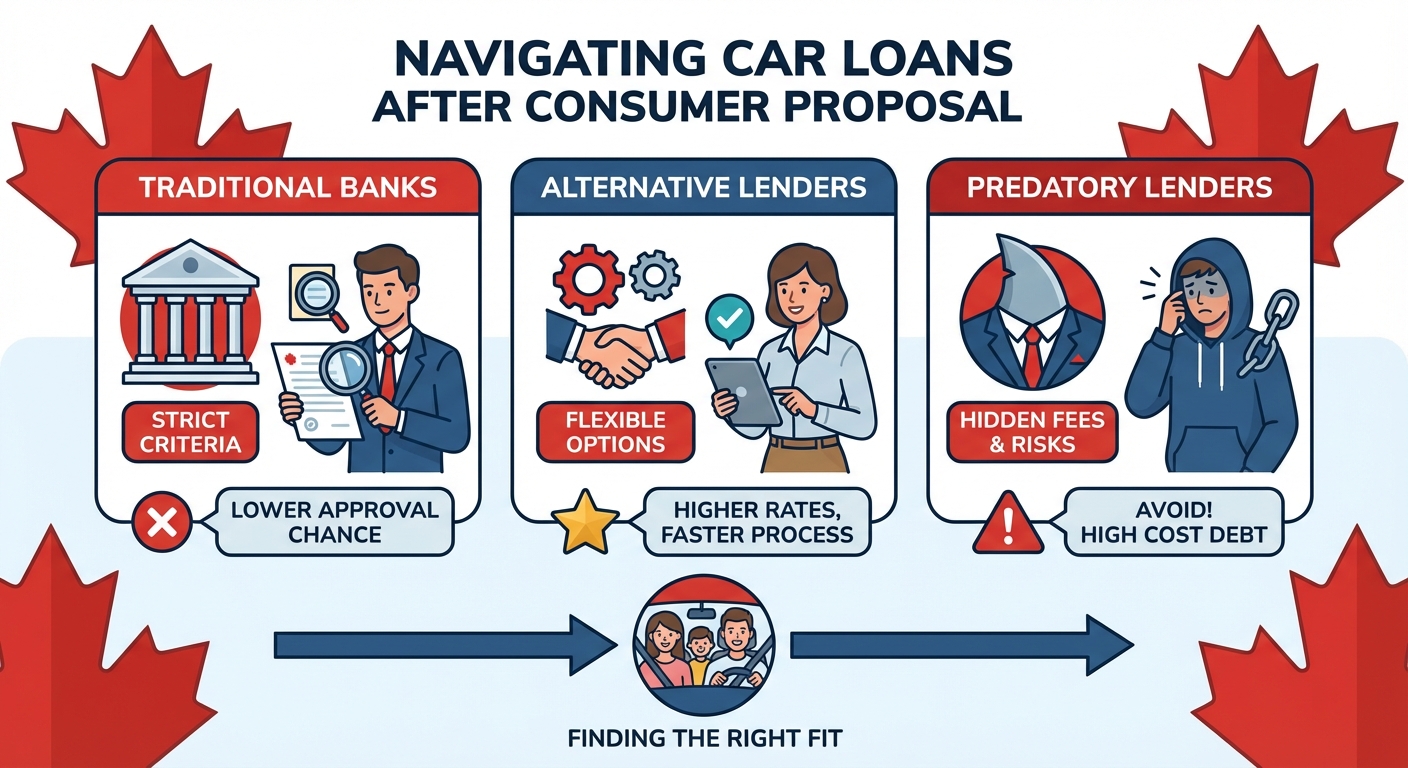

Navigating the Lender Labyrinth: Who Will Say 'Yes' (and at What Cost)?

Not all lenders are created equal, especially when you're seeking a car loan after a consumer proposal. Understanding the different types of lenders and their typical approaches is key to finding the right fit and avoiding predatory practices.

Tier 1: Specialist Lenders for Post-Proposal Applicants (The 'Second Chance' Specialists)

These lenders, often referred to as subprime or non-prime lenders, specialize in working with individuals who have faced financial challenges, including consumer proposals, bankruptcies, or generally lower credit scores.

- How they assess risk: They look beyond just your credit score, putting significant emphasis on your current income, employment stability, debt-to-income ratio, and your ability to provide a down payment. They understand that past events don't define your future.

- Typical rates: Expect higher interest rates compared to prime loans, as they are taking on greater risk. Rates can range from 10% to 25% or even higher, depending on your individual circumstances and the time elapsed since your discharge.

- Advantages: They are often your best bet for approval immediately after a consumer proposal discharge. They are set up to provide "second chance" financing, which can be a crucial stepping stone to rebuilding your credit.

- What to look out for: Be wary of excessively high interest rates or hidden fees. Always read the fine print and compare offers. Ensure the loan terms are manageable for your budget.

Tier 2: Credit Unions & Community Banks (Your Local Advantage)

Credit unions and smaller community banks often operate with a more flexible, relationship-focused approach compared to large national banks.

- How they assess risk: They may be more willing to consider your individual story and circumstances, especially if you have an existing banking relationship with them or can demonstrate consistent income and a strong desire to rebuild. They might look at your character and stability more holistically.

- Typical rates: Generally more competitive than specialist lenders, potentially falling in the 7% to 15% range, depending on your credit profile and the institution.

- Advantages: They can offer a middle ground – potentially better rates than specialist lenders for those with improving credit, and more flexibility than big banks. They often prioritize their members or local community residents.

- What to look out for: You may need to become a member (usually a small deposit) to apply for a loan. Their approval criteria, while more flexible than big banks, still tend to be stricter than specialist lenders.

Tier 3: Dealership Financing – The Good, The Bad, and The Ugly

Many dealerships offer financing options, either through their own in-house programs or by brokering loans with a network of lenders.

- In-house financing: Some dealerships offer financing directly. These can sometimes be easier to get approved for but often come with higher interest rates and less favourable terms.

- Dealer-brokered loans: Dealerships work with a variety of lenders, including specialist lenders and some banks. They can submit your application to multiple institutions simultaneously.

- Advantages: Convenience – you can often apply for financing and buy a car all in one place. Dealers have relationships with lenders who specialize in various credit situations.

- What to look out for: Dealers may mark up interest rates to increase their profit. Always come prepared with your own pre-approval to ensure you're getting a competitive rate. Without external offers, you might pay more than necessary.

Why Big Banks Remain a Challenge (Initially) – And How to Eventually Win Them Over

Major Canadian banks (like RBC, TD, Scotiabank, BMO, CIBC, National Bank) typically have the strictest lending criteria. Their automated systems often flag consumer proposals as high risk, making initial approval very difficult for non-prime applicants.

- The challenge: They primarily focus on prime borrowers with excellent credit scores and a long history of positive credit. Their algorithms are less forgiving of past credit events.

- The long-term goal: Don't target big banks for your *first* post-proposal car loan. Instead, use your first loan (from a specialist lender or credit union) as a tool to rebuild. Once you've made 12-24 months of perfect payments on that loan, and your credit score has significantly improved, you can then approach a major bank for refinancing at a much lower, prime interest rate. This is the ultimate victory in credit rebuilding.

Pro Tip: Get Pre-Approved *Before* You Shop for a Car

This is arguably one of the most powerful strategies for any car buyer, but especially for those rebuilding credit. Getting pre-approved from a specialist lender or credit union before you visit a dealership gives you a firm understanding of your budget and the interest rate you qualify for. It empowers you to negotiate the car price as a cash buyer, preventing the dealership from focusing on monthly payments and potentially hiding markups in the financing. You'll walk onto the lot with confidence, knowing your financing is already secured.

Crafting Your Irresistible Application: Beyond the Credit Score

While your credit score and history are important, they are not the only factors lenders consider. For post-proposal applicants, other elements of your application can significantly influence approval and loan terms. Think of it as painting a complete picture of your financial reliability.

The Down Payment Advantage: Lowering Lender Risk, Boosting Your Odds

A substantial down payment is one of your most potent tools when applying for a car loan after a consumer proposal. Here's why:

- Reduces Lender Risk: The more money you put down, the less the lender has to finance. This directly lowers their risk, as their exposure to potential default is reduced.

- Increases Approval Odds: With lower risk, lenders are more willing to approve your application, even with a recovering credit profile.

- Better Interest Rates: Reduced risk can translate into better interest rates. Even a 5-10% down payment can make a noticeable difference, while 15-20% can significantly improve your terms.

- Lower Monthly Payments: A larger down payment reduces the total amount borrowed, resulting in lower monthly payments and less interest paid over the life of the loan.

Aim to save as much as you can for a down payment. It's an investment in your financial future and an immediate signal of your commitment.

Income Stability & Employment History: Proving Your Capacity to Pay

Lenders need assurance that you can consistently make your loan payments. This is where your income and employment history come into play.

- Consistent Employment: A stable job with the same employer for at least 1-2 years is highly favourable. It shows reliability and a steady income stream.

- Verifiable Income: Lenders will require proof of income, typically through pay stubs (for employed individuals) or bank statements and tax returns (for self-employed individuals). Ensure your income is consistent and easily verifiable.

- Manageable Debt-to-Income Ratio: Your DTI (total monthly debt payments divided by gross monthly income) is a critical metric. Lenders want to see a DTI that allows you to comfortably afford new car payments without being overextended. Generally, a DTI below 40-45% is preferred.

The Co-Signer Conundrum: When it Helps, When it Hurts (and How to Protect Them)

A co-signer with good credit can significantly improve your chances of approval and secure a better interest rate.

- When it Helps: If your credit is still very weak, a co-signer adds their creditworthiness to your application, providing the lender with an additional guarantee.

- When it Hurts: A co-signer takes on full legal responsibility for the loan. If you miss payments, it negatively impacts their credit score and they are obligated to pay. This can strain personal relationships.

- How to Protect Them: Only consider a co-signer if you are absolutely confident in your ability to make every payment on time. Have a clear, written agreement with your co-signer outlining responsibilities. Ensure they understand the risks involved. Your ultimate goal should be to refinance the loan in your name alone once your credit improves.

Realistic Expectations: Choosing the Right Vehicle for Your Budget

It's tempting to eye that brand-new, fully loaded SUV, but after a consumer proposal, practicality should be your guide.

- Prioritize Affordability: Focus on reliable, affordable used cars. They depreciate slower, have lower insurance costs, and are easier to finance.

- Calculate True Affordability: Don't just consider the monthly payment. Factor in insurance, fuel, maintenance, and potential repair costs. A good rule of thumb is that your total car expenses (payment, insurance, fuel) shouldn't exceed 10-15% of your gross monthly income.

- Increase Approval Chances: Lenders are more comfortable financing a reasonably priced vehicle that aligns with your income and budget, rather than an aspirational purchase that strains your finances.

Documentation Deep Dive: What You *Must* Have Ready

Being prepared with all necessary documentation streamlines the application process and shows lenders you're serious and organized.

- Proof of Income: Recent pay stubs (3-4), employment letter, T4s, or Notice of Assessment (for self-employed).

- Proof of Identity: Valid Canadian driver's licence, passport, or other government-issued ID.

- Proof of Residency: Utility bill (hydro, gas, internet) or bank statement showing your current address.

- Consumer Proposal Discharge Papers: Official documentation confirming the successful completion and discharge of your proposal.

- Bank Statements: Recent statements (3-6 months) to show financial stability and cash flow.

- List of References: Some lenders may ask for personal or professional references.

For a detailed checklist, especially if you're in Alberta, you might find our guide on Approval Secrets: Exactly What Paperwork You Need for Alberta Car Financing helpful.

Pro Tip: Negotiating Your Interest Rate and Terms – It's Not Set in Stone

Even with a recovering credit score, interest rates are often negotiable, especially with specialist lenders or dealership financing. Don't simply accept the first offer. Come prepared with research on typical rates for your credit situation, and if you have a pre-approval from another lender, use it as leverage. Highlight your stable income, down payment, and consistent payment history since your proposal. Politely ask if there's any room for improvement on the rate or terms. Every percentage point saved can mean hundreds, if not thousands, of dollars over the life of the loan.

Beyond Approval: Smart Strategies for Your New Car Loan

Getting approved for a car loan after a consumer proposal is a significant milestone, but it's just the beginning. The way you manage this loan will profoundly impact your credit recovery and future financial opportunities. This loan is a