Lease Buyout Denied? Your Car Still Has a Future. (Yes, Even in Halifax).

Table of Contents

- Key Takeaways: Your Roadmap to Keeping Your Leased Car

- The Roadblock Revealed: Unpacking Your Lease Buyout Denial in Halifax and Beyond

- Why Your Credit Score Isn't the Only Culprit: Decoding Lender Decisions

- The Anatomy of a Lease Buyout: What You Were Up Against

- Reclaiming Your Financial Narrative: Preparing for a Successful 'Second Chance' Buyout

- Credit Report Deep Dive: Unearthing Opportunities and Addressing Red Flags

- Budgeting for Reality: Crafting a Sustainable Payment Plan

- Understanding Your Vehicle's True Worth: Appraisal and Market Value

- The Lifeline: Exploring Non-Traditional Financing Avenues for Challenged Credit

- Subprime Lenders: Your Direct Path to Re-Financing

- Credit Unions: Community Support with Flexible Terms

- Dealer Financing (In-House and Partnerships): A Convenient, Yet Cautious, Option

- Navigating the Deep End: Keeping Your Car After Bankruptcy or Consumer Proposal

- Consumer Proposal: A Path to Reaffirmation

- Post-Bankruptcy Financing: Rebuilding and Re-Engaging

- Addressing Late Payments and Collections: Proactive Communication is Key

- Beyond the APR: Unmasking the True Cost of Your Car's Future

- The Hidden Fees and Charges: What to Watch Out For

- Insurance Implications: How Your Credit Can Affect Your Premiums

- Long-Term Depreciation and Equity Building: Is it a Wise Investment?

- Your Next Steps to Approval: A Practical Checklist for Canadians

- Step 1: Get Your Documents in Order

- Step 2: Approach Lenders Strategically

- Step 3: Negotiate Like a Pro

- Step 4: Secure Your Future: Payment Tracking and Credit Building

- FAQ: Your Lingering Questions Answered

A lease buyout denial can feel like a dead end, especially when your credit history isn't sparkling. The prospect of losing your dependable ride can be daunting, impacting everything from your daily commute to your ability to manage family responsibilities. But for residents of Halifax, Nova Scotia, and across Canada, losing your vehicle isn't the only option. This deep-dive article explores proactive strategies to keep your leased car, even when facing significant credit challenges, offering practical advice, local insights, and a clear path forward. We understand that life throws curveballs, and a less-than-perfect credit score shouldn't automatically mean sacrificing your essential transportation.

Key Takeaways: Your Roadmap to Keeping Your Leased Car

- Denial is Not the End: A lease buyout rejection is a hurdle, not a stop sign. Alternative financing and negotiation are often viable.

- Credit Challenges are Common: Lenders understand that financial difficulties happen. Specialized options exist for those with consumer proposals, bankruptcies, or low credit scores.

- Preparation is Power: Understanding your credit report, current vehicle value, and personal budget is crucial before approaching new lenders.

- Explore Beyond Traditional Banks: Subprime lenders, credit unions, and even in-house dealer financing can be key allies in your quest.

- Location Matters: While principles are national, provincial regulations and local lender availability (e.g., in Halifax, Nova Scotia) can influence your options and success rate.

- Focus on the True Cost: Beyond the monthly payment, consider interest rates, fees, insurance, and long-term depreciation to make an informed decision.

The Roadblock Revealed: Unpacking Your Lease Buyout Denial in Halifax and Beyond

Before charting a new course, it's vital to understand why your initial lease buyout was denied. This isn't just about your credit score; it's a complex interplay of factors that lenders evaluate. A denial can feel personal, but it's typically a calculated risk assessment by the financial institution. We'll delve into the common culprits and how they specifically impact individuals in cities like Halifax, Nova Scotia, or Calgary, Alberta, where economic factors and market conditions can add another layer of complexity.

Why Your Credit Score Isn't the Only Culprit: Decoding Lender Decisions

While a low credit score is often the primary suspect, lenders consider a broader financial picture. Think of it as a mosaic, where your credit score is just one important tile. They're looking at your overall financial health, and a single metric rarely tells the whole story. Here’s a breakdown of other critical factors:

- Debt-to-Income (DTI) Ratio: This critical metric compares your total monthly debt payments to your gross monthly income. A high DTI signals to lenders that you might already be overextended, regardless of how well you've managed past credit. For instance, if you live in a high-cost-of-living area like Vancouver, British Columbia, or Toronto, Ontario, your DTI might be higher even with a good income due to mortgage or rent payments.

- Employment Stability: Lenders prefer a consistent employment history, ideally with the same employer for several years. Frequent job changes or periods of unemployment, even if brief, can raise concerns about your ability to maintain regular payments. This is particularly relevant for individuals in seasonal industries or those who are self-employed, though solutions exist for self-employed individuals looking for car loans.

- Vehicle's Market Value vs. Residual Value: The residual value is what the lessor projected the car would be worth at the end of the lease. If the car's actual market value has depreciated significantly more than anticipated (perhaps due to high mileage, condition, or a dip in the used car market), a lender might be hesitant to finance a buyout that leaves you "upside down" immediately. This scenario is especially common with certain luxury vehicles or models that experience rapid depreciation.

- Original Lessor's Internal Policies: Not all lenders are created equal. Some financial institutions that originally financed your lease might have stricter internal policies for buyouts, especially for customers with a changed credit profile. They might prefer to simply take the vehicle back rather than extending new credit for a buyout.

- Payment History with the Lessor: Even if your credit score is generally low, a perfect payment history on your lease itself can sometimes work in your favour. Conversely, a history of late or missed lease payments will be a major red flag, regardless of other positive factors.

- Recent Credit Inquiries: Too many recent applications for credit can lower your score and make you appear desperate to lenders. Each hard inquiry can slightly ding your score, so strategic application is key.

The Anatomy of a Lease Buyout: What You Were Up Against

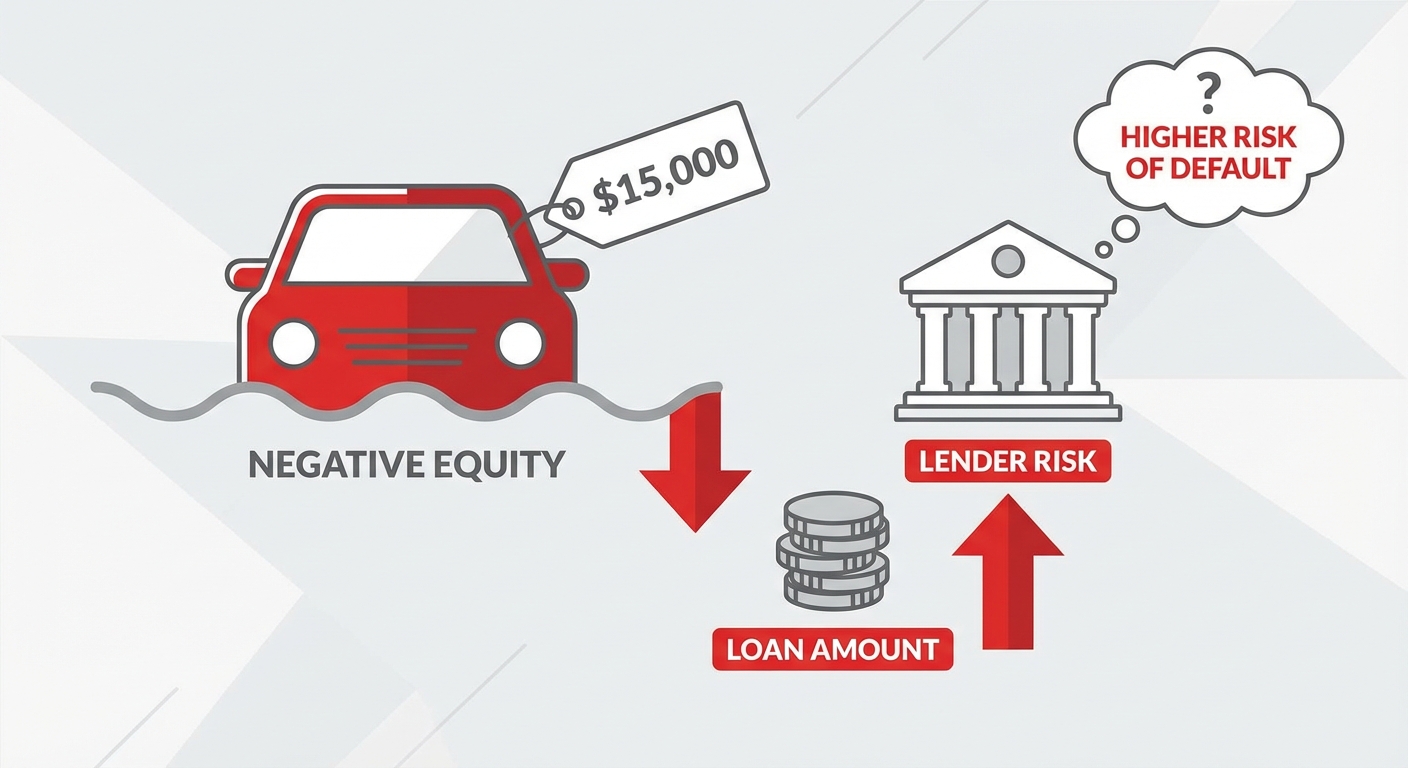

A quick refresher on how lease buyouts typically work helps clarify the financial mechanics at play. When you lease a car, you're essentially paying for the depreciation of the vehicle over the lease term, plus interest and fees. At the end of the lease, you have a few options: return the car, lease a new one, or buy out the current vehicle. The buyout price is determined by the "residual value" specified in your original lease agreement, plus any purchase option fees, outstanding taxes, and administration costs.

Lenders might be hesitant to finance a vehicle that's potentially depreciated below that residual value, especially when combined with a challenging credit profile. If the market value is less than the residual value, you'd be paying more than the car is currently worth. For example, if your lease agreement states a residual value of $18,000 for a car that, according to current market analysis, is only worth $15,000, you're looking at negative equity from day one. This makes it a riskier proposition for lenders, as their collateral (the car) is worth less than the loan amount, particularly if your credit history suggests a higher risk of default.

Reclaiming Your Financial Narrative: Preparing for a Successful 'Second Chance' Buyout

Successfully keeping your car despite credit challenges requires meticulous preparation. This isn't just about applying everywhere; it's about presenting yourself as a responsible borrower with a clear plan. Lenders, even those specializing in challenging credit, want to see that you've learned from past financial difficulties and are committed to making good on your new obligations. We'll guide you through the essential steps, applicable whether you're in Ottawa, Ontario, or a smaller community in Nova Scotia, such as Yarmouth or Truro.

Credit Report Deep Dive: Unearthing Opportunities and Addressing Red Flags

Obtaining and thoroughly reviewing your credit report from Equifax and TransUnion, Canada's two primary credit bureaus, is non-negotiable. This isn't merely a formality; it's your financial blueprint. You need to know exactly what lenders are seeing when they pull your report. We'll explain how to identify errors, dispute inaccuracies, and understand the factors that are truly impacting your score. This isn't just about finding problems; it's about finding opportunities to improve your profile, even marginally, before approaching new lenders.

Here’s what to look for:

- Personal Information Accuracy: Ensure your name, address, and employment history are correct. Mistakes here can affect your identity verification.

- Account Status: Check every account for correct payment status (e.g., "paid as agreed," "late," "collections").

- Errors and Inaccuracies: Disputed payments, accounts that aren't yours, or incorrect balances can significantly drag down your score. Both Equifax and TransUnion have clear processes for disputing errors. Gather supporting documentation and act swiftly.

- Hard Inquiries: Note how many hard inquiries appear. Too many in a short period can be detrimental.

- Debt Levels: Understand your current outstanding balances on credit cards, lines of credit, and other loans. High utilization (using a large percentage of your available credit) can negatively impact your score.

Even small improvements can make a big difference, especially when you're on the cusp of qualifying for better rates. For those who have faced significant challenges like consumer proposals or bankruptcy, understanding how these events appear on your report is crucial. While they remain for several years, demonstrating consistent positive behaviour afterward is key. For a deeper look into specific scenarios, consider our article on getting a car loan with active collections.

Pro Tip: The Power of a Small Improvement

Even a 10-20 point increase in your credit score can sometimes shift you into a more favourable lending tier, potentially saving you thousands in interest over the life of the loan. Focus on paying down small balances, correcting errors, and avoiding new credit inquiries in the months leading up to your application. Consider setting up payment reminders or automating small payments to credit cards to show consistent, positive activity.

Budgeting for Reality: Crafting a Sustainable Payment Plan

Lenders want to see that you can realistically afford the new loan. A meticulously crafted personal budget isn't just a suggestion; it's proof of your financial responsibility and foresight. We'll show you how to create a detailed personal budget, identify areas for cost-cutting, and determine a comfortable monthly payment. This plan will not only impress potential lenders but also ensure you don't fall into the same financial traps again. Be brutally honest with yourself about your income and expenses.

Start by listing all your sources of income. Then, meticulously list all your fixed expenses (rent/mortgage, existing loan payments, insurance) and variable expenses (groceries, utilities, fuel, entertainment). Look for areas where you can trim costs. Can you reduce discretionary spending? Are there subscriptions you can cancel? The goal is to demonstrate a clear surplus that can comfortably cover the new car loan payment, plus a buffer for unexpected costs. This level of detail shows a lender that you are serious about your financial commitment and have a solid grasp on your money management.

Understanding Your Vehicle's True Worth: Appraisal and Market Value

The residual value on your lease agreement might not reflect the car's current market value. This discrepancy can be a significant factor in your buyout decision. Get an independent appraisal. Knowing your car's actual worth strengthens your negotiation position and helps you assess if the buyout is still a financially sound decision. Services like Kelley Blue Book Canada or Canadian Black Book provide excellent resources for estimating your vehicle's value based on its make, model, year, mileage, and condition. An independent appraisal from a certified mechanic or valuation expert can give you a concrete figure.

If the market value is significantly higher than the residual value, you're in a strong position – you're buying equity. If it's lower, you need to carefully consider if paying the residual is still worth it, even with a new loan. This knowledge empowers you to negotiate with the lessor or evaluate whether to walk away and seek a different, more affordable vehicle.

The Lifeline: Exploring Non-Traditional Financing Avenues for Challenged Credit

When traditional banks say 'no,' it's time to look elsewhere. A diverse landscape of lenders specializes in helping individuals with less-than-perfect credit. These institutions understand that life circumstances can impact credit scores and are often more willing to look beyond just the numbers, focusing instead on your current ability to pay and your commitment to rebuilding credit. We'll explore these options, detailing their characteristics and what to expect, with specific examples relevant to the Canadian market, from Vancouver, British Columbia, to St. John's, Newfoundland and Labrador.

Subprime Lenders: Your Direct Path to Re-Financing

Demystifying subprime auto loans: how they work, who qualifies, and what interest rates to anticipate. Subprime lenders specialize in offering loans to individuals with lower credit scores, including those with a history of missed payments, consumer proposals, or even recent bankruptcies. They compensate for the increased risk by charging higher interest rates. However, for many Canadians in a challenging credit situation, a subprime loan represents a crucial opportunity to secure essential transportation and begin rebuilding their credit history.

Reputable subprime lenders in Canada will still assess your income, employment stability, and debt-to-income ratio, but their criteria are generally more flexible than traditional banks. It's crucial to approach them with transparency, providing all requested documentation. While interest rates will be higher, focus on securing a manageable monthly payment and a loan term that allows you to comfortably make payments. Over time, consistent on-time payments on a subprime loan can significantly improve your credit score, potentially allowing you to refinance at a lower rate in the future. Always ensure you understand all terms and conditions to avoid predatory practices.

Credit Unions: Community Support with Flexible Terms

Often overlooked, local credit unions can be more flexible than big banks, especially for their members. Credit unions are not-for-profit financial cooperatives owned by their members, which often translates to a more community-focused approach to lending. They may be more willing to consider your individual circumstances beyond just your credit score, especially if you have a long-standing relationship with them or are actively working to improve your financial situation.

We'll highlight the benefits of credit union financing for those with credit challenges and how to find one that might be willing to work with you in your specific region, such as those serving communities in Halifax, Nova Scotia, or other smaller towns across the Maritimes. Membership is usually required, but often just involves opening a small savings account. They may offer slightly more competitive rates than subprime lenders for similar risk profiles and can provide personalized advice. It's always worth exploring your local credit union options.

Dealer Financing (In-House and Partnerships): A Convenient, Yet Cautious, Option

Many dealerships offer in-house financing or have partnerships with a wide range of lenders, including subprime. This can be a convenient option, as you can often complete the entire vehicle purchase and financing process under one roof. Dealerships work with a network of lenders, which means they can often find a financing solution even for challenging credit situations. They understand the nuances of various lenders' criteria and can sometimes "shop around" on your behalf.

We'll discuss the pros and cons, the importance of negotiating terms, and how to ensure you're getting a fair deal, even when your options are limited. While convenient, it's crucial to be cautious. Always review the interest rate, loan term, and any additional fees carefully. Don't feel pressured to accept the first offer, and always compare it with other options you might have explored. Be prepared to walk away if the terms are not suitable or if you feel rushed. Dealerships can be excellent resources for those with challenged credit, but vigilance on your part is key to securing a favourable agreement.

Pro Tip: The Co-Signer Advantage

If you have a trusted friend or family member with good credit willing to co-sign, it can significantly improve your approval odds and secure a lower interest rate. A co-signer essentially guarantees the loan, mitigating risk for the lender. Ensure both parties understand the full implications and responsibilities of co-signing a loan, as the co-signer is equally responsible for repayment if you default.

Navigating the Deep End: Keeping Your Car After Bankruptcy or Consumer Proposal

The insight from Jean Fortin and other financial experts highlights that it is possible to keep your vehicle even after a consumer proposal or bankruptcy. These are significant financial events, but they do not necessarily mean the end of your ability to own a car. This section will provide an in-depth look at how this works in practice, detailing the legal and financial frameworks involved in Canada. For more detailed information on this topic, you might find our article Think Your Consumer Proposal Trapped Your Car Payments? Think Again, British Columbia. particularly helpful.

Consumer Proposal: A Path to Reaffirmation

A consumer proposal is a formal, legally binding offer made by an insolvent debtor to their creditors to pay back a portion of their debts over a period of up to five years. If your lease payments were current and the vehicle was insured during your consumer proposal, you might be able to 'reaffirm' the debt. Reaffirmation means you agree to continue making payments on the lease as per the original terms, essentially taking the lease out of the proposal. We'll explain the process, the role of your Licensed Insolvency Trustee (LIT), and what lenders look for post-proposal.

Your LIT will guide you on whether reaffirming your car lease is a viable option. It typically involves demonstrating that you can afford the payments and that the vehicle is essential. Lenders post-proposal will look for stability, a clear budget, and a commitment to rebuilding your credit. While the proposal itself affects your credit, successfully reaffirming and continuing payments on your vehicle can be a strong positive indicator for future lenders.

Post-Bankruptcy Financing: Rebuilding and Re-Engaging

While more challenging, keeping or re-financing a car after bankruptcy is not impossible. Bankruptcy offers a fresh financial start by discharging most unsecured debts, but it severely impacts your credit score for several years. This section outlines the typical waiting periods, the importance of rebuilding credit immediately, and specific lenders who specialize in post-bankruptcy auto financing across provinces like Alberta and Quebec.

Generally, lenders prefer to see some time pass after a bankruptcy discharge – often 1-2 years – and evidence that you've begun to rebuild your credit through secured credit cards or small, manageable loans. Specialized lenders understand the 'fresh start' aspect of bankruptcy and are designed to help individuals re-enter the credit market. They'll focus on your current income, employment stability, and your demonstrated commitment to financial responsibility since the bankruptcy. For more comprehensive guidance, read Bankruptcy Discharge: Your Car Loan's Starting Line.

Addressing Late Payments and Collections: Proactive Communication is Key

For those with a history of late payments or accounts in collections, hope is not lost. The key is proactive communication and demonstrating renewed financial responsibility. Before approaching new lenders, try to resolve any outstanding collections accounts. Even negotiating a "pay for delete" (where the collection agency agrees to remove the derogatory mark from your credit report upon payment) can significantly help, though these are rare and not guaranteed. If a pay-for-delete isn't possible, simply paying off the collection shows initiative.

When presenting your case to new lenders, be honest about your past difficulties but emphasize your current stability and improved financial habits. Highlight any steps you've taken to get back on track, such as creating a strict budget, increasing income, or reducing other debts. Your ability to show a clear path forward and a commitment to consistent payments is often more impactful than trying to hide past issues.

Beyond the APR: Unmasking the True Cost of Your Car's Future

Securing financing is only half the battle. Understanding the total financial commitment is crucial to avoid future pitfalls. A low monthly payment might seem appealing, but if it's coupled with a sky-high interest rate and hidden fees, you could end up paying far more than the car is worth over the loan term. This section dives into the often-overlooked costs and long-term implications of keeping your car with a challenging credit profile, ensuring you make an informed decision for your financial well-being.

The Hidden Fees and Charges: What to Watch Out For

Beyond the interest rate (APR), new loans can come with various fees that inflate the total cost. These can sometimes be buried in the fine print or presented as non-negotiable. We'll detail these potential costs and arm you with questions to ask every lender to ensure full transparency:

- Administration Fees: Charges for processing your loan paperwork.

- Loan Origination Fees: A fee for originating the loan, often a percentage of the loan amount.

- Mandatory Add-ons: Dealerships might try to include extended warranties, rust protection, or fabric protection. While some might be beneficial, they significantly increase your loan amount and interest. Always question their necessity and negotiate.

- Lien Registration Fees: Costs associated with registering the lien on the vehicle title.

- PST/GST/HST: Sales taxes on the purchase price of the vehicle, which can be substantial.

Always ask for a detailed breakdown of all costs and fees. Don't be afraid to question anything you don't understand or feel is excessive. A reputable lender or dealer will be transparent about all charges.

Insurance Implications: How Your Credit Can Affect Your Premiums

In many Canadian provinces, your credit score can influence your auto insurance premiums. Insurers use credit scores as a predictor of risk, believing that individuals with lower credit scores are more likely to file claims or miss payments. We'll explore this connection, discuss strategies for finding affordable coverage, and highlight any provincial differences (e.g., between Nova Scotia and British Columbia) that might impact your overall vehicle ownership costs.

For example, in provinces like Ontario and Alberta, your credit score can be a factor in calculating premiums, while in others like Newfoundland and Labrador, its impact might be less direct. Always shop around for insurance, getting quotes from multiple providers. Improving your credit score over time can eventually lead to lower premiums. Consider increasing your deductible if you can afford it, or ask about discounts for winter tires, anti-theft devices, or bundling home and auto insurance.

Long-Term Depreciation and Equity Building: Is it a Wise Investment?

While keeping your car provides essential transportation, consider its long-term financial viability. Cars are depreciating assets, and high interest rates can significantly impact your ability to build equity. We'll discuss how high interest rates can impact equity building and when it might be more strategic to consider a different, more affordable vehicle in the future.

With a high-interest subprime loan, a larger portion of your early payments goes towards interest, meaning you build equity more slowly. This can leave you "upside down" on your loan (owing more than the car is worth) for a longer period. While keeping your current car might seem convenient, if the total cost of the buyout (including high interest) significantly exceeds the car's current and projected value, it might be more financially prudent to return the car and seek a more affordable, lower-value vehicle with a more manageable loan, allowing you to build equity faster and reduce your overall financial burden.

Pro Tip: Read Every Line of the Contract

Never sign a loan agreement without thoroughly reading and understanding every clause. This includes the interest rate, loan term, total amount repayable, and all fees. If something is unclear, ask for clarification. Don't be rushed or pressured. Take the contract home if needed. A clear understanding prevents costly surprises down the road and ensures you're comfortable with your commitment.

Your Next Steps to Approval: A Practical Checklist for Canadians

Armed with knowledge, it's time for action. This step-by-step checklist will guide you through the application process, helping you maximize your chances of approval and secure the best possible terms for keeping your leased car. Remember, preparation and persistence are your greatest allies.

Step 1: Get Your Documents in Order

A comprehensive list of documents you'll need will streamline the application process and present you as an organized, serious borrower. Having these ready prevents delays and shows lenders you are prepared. Gather the following:

- Identification: Valid Canadian driver's licence, passport, or other government-issued ID.

- Proof of Income: Recent pay stubs (3-6 months), employment letter, Canada Revenue Agency (CRA) Notice of Assessment, or bank statements for self-employed individuals. For those on government benefits, a statement of benefits.

- Proof of Residence: Utility bill, bank statement, or lease agreement showing your current address.

- Existing Lease Agreement: The original document detailing the residual value, lease term, and any purchase options.

- Vehicle Details: Vehicle Identification Number (VIN), current mileage, and any service records.

- Proof of Assets: (Optional, but helpful) Bank account statements, investment statements.

- References: Some lenders may ask for personal or professional references.

Step 2: Approach Lenders Strategically

Tips on how to present your case, what to emphasize (e.g., current stable income, improved budgeting), and how to manage multiple applications without negatively impacting your credit further. Begin with lenders that specialize in challenging credit, such as subprime lenders or credit unions where you have a relationship. Explain your situation honestly and focus on your current ability to pay and your commitment to improving your financial standing. Highlight any positive changes you've made, such as a new stable job, paying down other debts, or successfully managing a secured credit card.

Avoid applying to too many lenders at once, as each "hard inquiry" can temporarily lower your credit score. Instead, do your research, narrow down your options, and apply to a few carefully chosen lenders within a short timeframe (typically 14-45 days), as multiple inquiries for the same type of loan within this window are often counted as a single inquiry by credit scoring models like FICO.

Step 3: Negotiate Like a Pro

Even with credit challenges, there's room for negotiation. Knowing your vehicle's market value is a powerful tool here. Key negotiation points include:

- Interest Rate: While rates will be higher with challenged credit, always ask if there's any flexibility.

- Loan Term: A longer term means lower monthly payments but more interest paid overall. A shorter term saves on interest but increases monthly payments. Find a balance that fits your budget.

- Fees: Question all administrative, processing, and add-on fees. Some might be negotiable or avoidable.

If your car's market value is significantly higher than the residual value, you can leverage this. You're buying equity, which reduces the lender's risk. If the market value is lower, you might be able to negotiate with the lessor directly on the buyout price if they are keen to avoid taking the car back and incurring disposition fees. Be confident, informed, and prepared to walk away if the terms are not acceptable. Do not feel pressured into a deal that doesn't feel right.

Step 4: Secure Your Future: Payment Tracking and Credit Building

Once approved, the journey continues. This new loan is a powerful tool to rebuild your credit. We'll provide advice on setting up automatic payments, consistently monitoring your credit, and utilizing your new loan as a tool to rebuild your credit score effectively. Consistently making on-time payments is the single most effective way to improve your credit score over time.

Set up automatic payments to ensure you never miss a due date. Continue to monitor your credit report regularly (you're entitled to a free copy annually from Equifax and TransUnion) to track your progress and ensure accuracy. As your credit score improves, explore options to refinance your loan at a lower interest rate, which can save you a significant amount of money over the life of the loan. This systematic approach will not only keep your car but also pave the way for a healthier financial future.

Pro Tip: Set Up Automatic Payments

To avoid missing payments and further damaging your credit, set up automatic deductions from your bank account. This ensures consistency, helps you budget more effectively, and provides peace of mind that your payments are always on time, which is crucial for credit rebuilding.