Your Luxury Ride. No Pay Stub Opera.

Table of Contents

- Your Luxury Ride. No Pay Stub Opera.

- Key Takeaways

- Cracking the Code: How 'No Income Verification' Actually Works for the Self-Made

- The Pillars of Approval: What Lenders *Actually* Look For When Pay Stubs Are Absent

- Credit Score as Your Silent Partner: The Undeniable Power of a Stellar History

- Asset-Based Lending: Your Wealth, Not Your Wage

- The Down Payment Dominance: Why a Significant Upfront Investment is Your Strongest Negotiating Chip

- Business Bank Statements: The New Income Proof

- Navigating the Ecosystem: Who Offers These Specialized Loans?

- The Dealership Advantage: In-House Finance Specialists

- Boutique Lenders & Specialty Finance Companies: The True Niche Players

- Credit Unions: The Underestimated Ally

- Avoiding the Predatory Pitfalls: Identifying and Sidestepping High-Interest Traps and Scams

- The Cost of Convenience: Deconstructing Rates, Fees, and Hidden Charges

- Interest Rates: The Premium for Flexibility

- Origination Fees & Documentation Charges: What to Expect, How They're Calculated, and Strategies for Negotiation

- Prepayment Penalties: Freedom or Fetter? Understanding the Fine Print Regarding Early Loan Repayment

- Total Cost of Ownership Beyond the Payment: Beyond the loan, consider insurance implications, maintenance costs, and depreciation for luxury vehicles.

- Strategic Vehicle Selection: Does Brand Matter for Approval?

- High-Demand vs. Niche Luxury: How a Vehicle's Resale Value, Market Liquidity, and Perceived Reliability Influence Lender Confidence

- Age and Mileage Considerations: Why Newer, Lower-Mileage Luxury Cars Are Often Easier (and Cheaper) to Finance

- Specific Brands & Their Financing Arms: A Brief Overview

- The Art of Presentation: Crafting Your Financial Narrative

- Beyond the Numbers: The Story of Your Success

- Documentation That Speaks Volumes (Without a W-2)

- The Power of a Co-Signer (When Necessary): A Strategic Consideration

- Your Next Steps to Approval: A Blueprint for Success

- Step 1: Financial Self-Assessment

- Step 2: Documentation Assembly

- Step 3: Research & Lender Matching

- Step 4: Pre-Approval Pursuit

- Step 5: Negotiation Mastery

- Step 6: Due Diligence & Finalization

- FAQ: Unlocking Further Clarity on Your Luxury Journey

Your Luxury Ride. No Pay Stub Opera.

The hum of a finely tuned engine, the scent of premium leather, the sleek lines of a vehicle that commands attention – this isn't just a car, it's a statement. For Canada's thriving community of entrepreneurs, dynamic freelancers, and gig economy trailblazers, a luxury vehicle often signifies more than status; it represents hard-earned success, a reward for relentless dedication, and sometimes, a necessary tool for business. You've built your empire, navigated complex projects, and delivered exceptional results. Your financial acumen is undeniable, your drive unparalleled. So, why should securing the luxury car you deserve feel like an impossible quest, bogged down by outdated bureaucratic hurdles? The silent frustration for many self-employed individuals is the stark reality that traditional financing models often miss the mark. Banks, accustomed to the predictable rhythm of bi-weekly pay stubs and T4s, struggle to comprehend the nuanced, yet often robust, financial landscape of the self-made. Your income might be project-based, seasonal, or flow through various channels, making it difficult to fit into conventional boxes. This isn't a reflection of your financial health, but rather a limitation of their system. But what if we told you that "luxury car financing for self-employed no income verification" isn't a myth whispered in hushed tones, but a specialized, legitimate path? It’s a paradigm shift, moving away from rigid documentation to a more holistic assessment of your financial strength. This article is your definitive guide, cutting through the noise and empowering you to confidently step into the driver's seat of your dream vehicle. We'll demystify the process, highlight what lenders truly look for, and equip you with the knowledge to navigate this specialized financing landscape. Your luxury chariot awaits, and it doesn't require a traditional pay stub opera.

Key Takeaways

- Securing a luxury car loan without traditional income verification is absolutely possible for self-employed individuals, but it demands a strategic approach.

- Lenders will focus on alternative proofs of financial stability, such as your credit profile, available assets, and consistent business bank statements.

- Specialized lenders, dealership finance departments, and even some credit unions are more likely to offer flexible solutions than traditional banks.

- Be prepared for potentially higher interest rates due to the perceived increased risk, but always negotiate fiercely.

- Diligent management and proactive strengthening of your credit score are paramount to success in this unique financing environment.

Cracking the Code: How 'No Income Verification' Actually Works for the Self-Made

The phrase "no income verification" can conjure images of reckless lending or shady deals, but for the self-employed, it’s far from it. Let's start by debunking the myth: it's not truly *no verification*. Instead, it's about *alternative verification* – a crucial and nuanced distinction. Lenders aren't simply handing out luxury car loans based on a handshake and a dream. They are, however, willing to look beyond the traditional W-2 or employer-issued pay stub to assess your financial capacity.

From a lender's perspective, the primary goal is risk assessment. A W-2 provides a clear, consistent snapshot of income, making their job straightforward. Without that comfort blanket, they need to piece together a different picture of your financial stability and ability to repay the loan. They're looking for patterns, consistency, and evidence of substantial wealth or cash flow that mitigates the absence of a standard employment record. This means they'll scrutinize your overall financial health, not just a single line item on a pay stub. They understand that entrepreneurs often have significant write-offs that reduce their taxable income, which might not reflect their actual cash flow or purchasing power.

Why has this niche market emerged? The "why" is simple: market demand. Canada boasts a vibrant and growing population of affluent self-employed individuals, from tech consultants and creative professionals to established business owners and property investors. These individuals contribute significantly to the economy, drive innovation, and often have substantial assets and robust cash flow, even if their declared taxable income appears modest. Specialized lenders and forward-thinking dealerships recognize this segment's purchasing power and have adapted their underwriting criteria to serve it. They understand that a traditional bank's 'no' isn't necessarily a reflection of your financial health, but a limitation of their rigid systems. This specialization fills a critical gap, empowering you to access the financing needed for the luxury vehicle that complements your lifestyle and business success.

The Pillars of Approval: What Lenders *Actually* Look For When Pay Stubs Are Absent

When the traditional pay stub is out of the picture, lenders pivot their focus to other, equally compelling indicators of financial responsibility and repayment capacity. These are your pillars of approval, and understanding them is key to successfully securing your luxury ride.

Credit Score as Your Silent Partner: The Undeniable Power of a Stellar History

Your credit score becomes arguably the most critical piece of your financial puzzle when traditional income verification is absent. A high credit score (generally 700+ for luxury financing, often aiming for 750 or higher) tells lenders that you are a reliable borrower who consistently honours financial commitments. It's a testament to your past behaviour, indicating a low risk of default. This becomes your primary proxy for financial stability, demonstrating a history of managing debt responsibly, even if your income sources are diverse. Pro Tip: Proactive Credit Health Don't wait until you're ready to apply. Regularly monitor your credit report for errors, pay all your bills on time, keep your credit utilization low (ideally below 30% of your available credit), and avoid opening too many new credit lines simultaneously. Consider using credit monitoring services to stay on top of any changes. A meticulously maintained credit score is your most powerful asset in this scenario. For more insights into what goes into your score, check out our guide on The Truth About the Minimum Credit Score for Ontario Car Loans.

Asset-Based Lending: Your Wealth, Not Your Wage

For the self-employed, wealth often resides in assets rather than a fixed salary. Asset-based lending leverages this reality. Lenders are interested in your liquid assets – substantial savings accounts, investment portfolios (stocks, bonds, mutual funds), or brokerage accounts. These demonstrate a robust financial buffer and the ability to cover loan payments should your business experience a temporary dip. Beyond liquid assets, real estate equity can also play a significant role. If you own property with substantial equity, this can be used as collateral or simply as a strong indicator of your net worth. Understanding the concept of pledged assets is crucial here; you might offer certain assets as security for the loan, reducing the lender's risk and potentially leading to more favourable terms. This approach shifts the focus from "how much do you earn?" to "how much do you own?".

The Down Payment Dominance: Why a Significant Upfront Investment is Your Strongest Negotiating Chip

A substantial down payment is more than just a reduction in your loan amount; it's a powerful signal to lenders. It demonstrates your serious commitment to the purchase, reduces the loan-to-value (LTV) ratio, and significantly lowers the lender's risk exposure. For luxury vehicles, especially without traditional income verification, a down payment of 20% or even 30%+ can dramatically improve your approval odds and unlock better interest rates. Maximizing your down payment directly impacts your monthly payments and the total interest paid over the life of the loan. From a psychological standpoint, a large upfront investment instils confidence in the lender, showing them you have significant skin in the game and are less likely to default. It effectively tells them, "I am a serious, financially capable buyer."

Business Bank Statements: The New Income Proof

While pay stubs are absent, your business bank statements become a powerful, alternative form of income verification. Lenders will typically request 6-12 months of statements, meticulously scrutinizing them for consistent cash flow, regular deposits, and overall profitability. They're looking for a clear pattern of healthy account balances, transaction volume that aligns with your business activities, and recurring income that demonstrates your business's viability and your capacity to handle loan payments. They want to see evidence of a well-managed business, not just sporadic large deposits. For more on how your banking activity proves your financial health, consider exploring our article on Self-Employed? Your Bank Statement is Our 'Income Proof'. Pro Tip: Clean Books, Clear Path Maintain impeccably organized and consistent financial records. Avoid large, irregular transfers between personal and business accounts that could obscure your true cash flow. Keep personal expenses separate from business expenses as much as possible. Lenders appreciate transparency and clarity, which makes their assessment process much smoother. Professional Network & References: Sometimes, your reputation precedes your paperwork. While less common for standard auto loans, for very high-net-worth individuals or through niche lenders, professional references or a strong business network can occasionally serve as supplemental proof of your standing and reliability. This is particularly true in smaller, specialized lending environments where relationships can carry significant weight.

Navigating the Ecosystem: Who Offers These Specialized Loans?

Finding the right lender is paramount when seeking luxury car financing without traditional income verification. Not all financial institutions are created equal in their willingness or ability to assess non-W-2 income.

The Dealership Advantage: In-House Finance Specialists

Your local luxury car dealership is often your first and best point of contact. Why? They have a powerful incentive to close the sale. Dealerships work with a diverse network of lenders, including those that specialize in non-traditional financing and even subprime institutions, if needed. Their finance specialists are adept at packaging applications to highlight your strengths and often have established relationships with specific lenders who are more flexible with self-employed applicants. Furthermore, many luxury brands have their own captive finance arms (e.g., Mercedes-Benz Financial Services, BMW Financial Services, Audi Financial Services, Porsche Financial Services). These entities are often more understanding of the unique financial profiles of their target clientele – which frequently includes successful entrepreneurs and business owners. They are sometimes willing to offer more creative financing solutions, especially for brand loyalists or those with significant down payments.

Boutique Lenders & Specialty Finance Companies: The True Niche Players

Beyond the dealerships, a growing number of boutique lenders and specialty finance companies have carved out a niche specifically for non-traditional borrowers. These firms are less constrained by the rigid underwriting guidelines of large banks and are often more flexible in their criteria. They understand the intricacies of self-employment and are equipped to evaluate a broader range of financial indicators. While their flexibility is a huge advantage, it's important to note that these lenders may come with potentially higher interest rates due to the specialized nature of the loans and the perceived increased risk. Identifying reputable players is crucial; look for those with established histories, transparent processes, and positive customer reviews. Pro Tip: Vet Your Lender Be vigilant when choosing a finance partner. Red flags include "guaranteed approval" promises (no legitimate lender can guarantee approval without assessing your profile), requests for upfront fees before any approval, or a lack of transparency regarding terms and conditions. Green lights include clear communication, a professional online presence, a history of working with self-employed clients, and a willingness to explain their underwriting process.

Credit Unions: The Underestimated Ally

Don't overlook credit unions in your search. As member-focused institutions, they often take a more personalized approach to loan applications. If you have an existing banking relationship with a credit union, they may already have a deeper understanding of your financial history and business operations, leading to a more understanding review of your unique situation. While their criteria are still stringent, they might offer more flexibility than large commercial banks, sometimes even providing competitive rates if you meet their (albeit still robust) requirements.

Avoiding the Predatory Pitfalls: Identifying and Sidestepping High-Interest Traps and Scams

In the pursuit of specialized financing, it's vital to remain cautious. The market for non-traditional loans can attract less scrupulous operators. Be wary of lenders who pressure you into quick decisions, demand excessive upfront fees, or refuse to provide clear, written documentation of all terms. Always compare offers, read the fine print, and ensure you understand the total cost of the loan before committing. If an offer seems too good to be true, it likely is.

The Cost of Convenience: Deconstructing Rates, Fees, and Hidden Charges

Securing a luxury car loan without traditional income verification offers unparalleled convenience and flexibility, but it's important to have a clear understanding of the financial implications. This specialized path often comes with a different cost structure than conventional loans.

Interest Rates: The Premium for Flexibility

One of the most significant differences you'll encounter is the interest rate. Because lenders are taking on a higher perceived risk by not having a standard W-2 income to verify, they typically charge higher interest rates compared to traditional, fully-verified loans. This premium for flexibility is how they mitigate that risk. Several factors will influence your specific rate:

- Credit Score: A stellar credit score can significantly offset the lack of traditional income verification, often leading to lower rates.

- Down Payment Size: A larger down payment reduces the loan amount and the lender's risk, which can translate into a better rate.

- Loan Term: Shorter loan terms generally have lower interest rates, but higher monthly payments.

- Vehicle Age & Mileage: Newer, lower-mileage luxury cars are seen as less risky collateral, often attracting better rates.

- Lender Risk Assessment: Each lender has its own algorithm for assessing risk, so rates can vary widely.

Origination Fees & Documentation Charges: What to Expect, How They're Calculated, and Strategies for Negotiation

Many specialized loans, particularly from boutique lenders, may include origination fees or documentation charges. These are fees charged by the lender for processing your loan application and setting up the loan. They can be a flat fee or a percentage of the loan amount. Always ask for a full breakdown of all fees. While some fees are non-negotiable, others, especially origination fees, might be subject to negotiation, particularly if you have a strong overall financial profile or are making a substantial down payment. Don't be afraid to ask if they can be waived or reduced.

Prepayment Penalties: Freedom or Fetter? Understanding the Fine Print Regarding Early Loan Repayment

Before signing any loan agreement, meticulously check for prepayment penalties. Some lenders include clauses that charge you a fee if you pay off your loan early, designed to recoup the interest they would have earned. For self-employed individuals whose income might fluctuate, or who anticipate a significant windfall, the ability to pay off a loan early without penalty can be a huge advantage. Ensure you understand this clause fully and negotiate its removal if possible, or factor it into your decision-making.

Total Cost of Ownership Beyond the Payment: Beyond the loan, consider insurance implications, maintenance costs, and depreciation for luxury vehicles.

Remember that the loan payment is only one part of owning a luxury vehicle. These cars often come with higher insurance premiums, particularly for high-performance models or newer vehicles. Maintenance costs can also be significantly higher than for standard cars, requiring specialized parts and labour. Furthermore, luxury vehicles, like all cars, depreciate. Understanding the total cost of ownership, including these factors, is crucial for a realistic financial plan. Pro Tip: The APR vs. Stated Rate When comparing loan offers, always focus on the Annual Percentage Rate (APR), not just the stated interest rate or the monthly payment. The APR includes the interest rate plus certain fees, giving you the true, comprehensive cost of borrowing over the loan's term. This is the most accurate metric for comparing different loan products. For insights on managing and potentially lowering your car loan costs over time, read our article on Approval Secrets: How to Refinance Your Canadian Car Loan with Bad Credit.

Strategic Vehicle Selection: Does Brand Matter for Approval?

When pursuing luxury car financing without traditional income verification, your choice of vehicle can subtly, yet significantly, influence your approval odds and loan terms. It's not just about what you can afford, but also what a lender perceives as a sound investment.

High-Demand vs. Niche Luxury: How a Vehicle's Resale Value, Market Liquidity, and Perceived Reliability Influence Lender Confidence

Lenders prefer to finance vehicles that hold their value well and are relatively easy to resell in case of default. High-demand luxury brands and models with strong resale values (e.g., certain Lexus, BMW, Mercedes-Benz, or Audi models) will generally be viewed more favourably. Vehicles with proven reliability also reduce a lender's risk. Conversely, extremely niche or highly customized luxury cars, or those with a reputation for rapid depreciation, might be harder to finance or come with less attractive terms, as their market liquidity (how easily they can be sold) is lower.

Age and Mileage Considerations: Why Newer, Lower-Mileage Luxury Cars Are Often Easier (and Cheaper) to Finance

Generally, newer luxury cars with lower mileage are easier to finance. They are considered more reliable, require less immediate maintenance, and have a longer lifespan, making them more valuable collateral for the lender. Older, higher-mileage luxury vehicles, while potentially more affordable upfront, carry a higher risk of mechanical issues and rapid depreciation, which lenders factor into their risk assessment. This can result in higher interest rates, shorter loan terms, or require a larger down payment.

Specific Brands & Their Financing Arms: A Brief Overview

Many luxury brands operate their own captive finance companies, which can be a significant advantage for self-employed buyers.

- Mercedes-Benz Financial Services, BMW Financial Services, Audi Financial Services, Porsche Financial Services: These captive finance arms are often more attuned to the financial profiles of their target demographic, including high-net-worth self-employed individuals. They may have specific programs or more flexible underwriting for their brand's loyal customers.

- Lexus Financial Services: Known for reliability and strong resale values, Lexus can be a strong contender for favourable financing terms, even with alternative income verification.

- Tesla: As a relatively newer player with a unique sales model, Tesla financing (or third-party lenders they partner with) will heavily weigh credit score and assets, as their vehicles hold value well but also have a distinct market.

These captive finance companies understand that their clients' financial lives may not fit neatly into traditional boxes, and they have an incentive to keep customers within their brand ecosystem. Pro Tip: Test Drive Your Finances First Before you even step foot on a dealership lot or fall in love with a specific model, focus on securing pre-approval for a general loan amount. This crucial step gives you a clear understanding of your budget, interest rate, and terms. It empowers you to negotiate with confidence and avoids the disappointment of finding your dream car only to discover it's beyond your approved financing.

The Art of Presentation: Crafting Your Financial Narrative

When you're self-employed and seeking luxury car financing without a traditional pay stub, your application isn't just a collection of documents; it's a narrative. You need to tell a compelling story of financial stability, success, and reliability.

Beyond the Numbers: The Story of Your Success

Lenders are human, and a well-crafted narrative can make a significant difference. Prepare a concise, compelling summary of your business. Highlight its stability, your industry experience, and your future projections. Emphasize long-term client relationships, consistent project flow, or an established presence in your market. Explain how your business generates income and why it's sustainable. This qualitative data helps humanize your application and provides context for the numbers you're presenting. It shows the lender you're a savvy business owner, not just an applicant with unconventional income.

Documentation That Speaks Volumes (Without a W-2)

This is where your meticulous preparation truly shines. Gather a comprehensive suite of documents that, collectively, paint a clear picture of your financial health:

- Comprehensive Bank Statements: Provide 6-12 months of both personal and business bank statements. Lenders will scrutinize these for consistent deposits, healthy average balances, and responsible money management.

- Recent Tax Returns: Even if your tax returns show significant write-offs that reduce your taxable income, they confirm legitimate business activity and adherence to financial regulations. Be prepared to explain any discrepancies between taxable income and actual cash flow.

- Proof of Assets: Include statements for investment accounts (brokerage, mutual funds, RRSPs, TFSAs), property deeds, or trust documents. These demonstrate your net worth and serve as a financial safety net.

- Business Licenses & Registrations: Official documentation proves your business is legitimate and operating legally.

- Significant Contracts & Invoices: Copies of long-term client contracts, recent substantial invoices, or proof of recurring revenue streams can demonstrate predictable future income.

- Professional References: While less common, for niche lenders, professional references from accountants, lawyers, or long-standing business partners can sometimes add credibility.

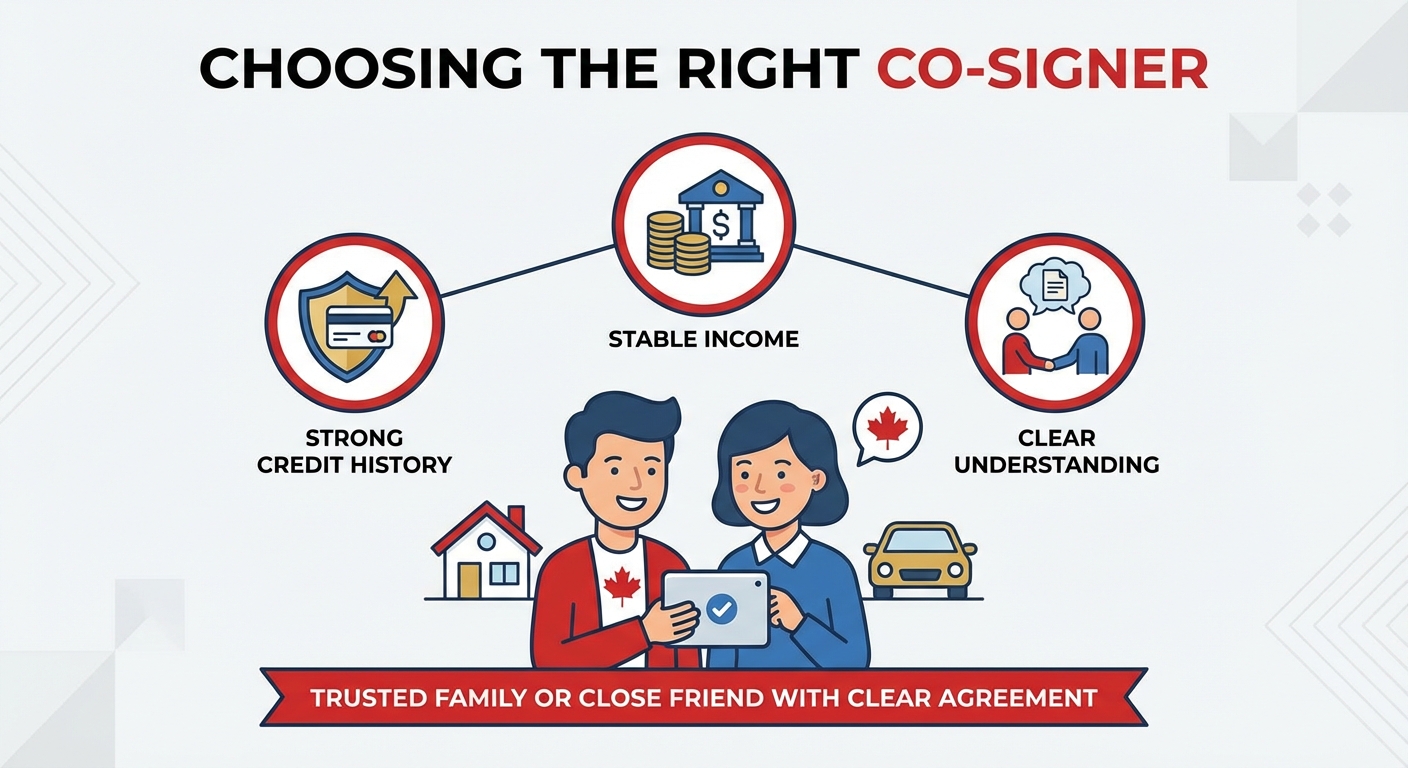

The Power of a Co-Signer (When Necessary): A Strategic Consideration

If, after assembling your strongest financial narrative, you still face challenges with approval or securing favourable terms, a co-signer with excellent credit and a stable income can be a strategic consideration.

- Implications & Responsibility: Understand that a co-signer is equally responsible for the loan. If you default, their credit will be negatively impacted, and they will be legally obligated to make the payments. This is a significant commitment for both parties.

- When It's Viable: A co-signer is best used as a strategy to enhance approval odds or secure a better interest rate, rather than a last resort for an otherwise unapprovable loan. It can bridge the gap if you have a strong down payment and assets, but perhaps a shorter business history or a slightly less-than-perfect credit score.

- Choosing the Right Co-Signer: Select a co-signer with a strong credit history, stable income, and a clear understanding of their responsibilities. Ideally, this would be a trusted family member or close friend with whom you have a clear agreement.

Your Next Steps to Approval: A Blueprint for Success

The journey to your luxury vehicle, free from traditional pay stub constraints, is within reach. By following this blueprint, you can navigate the process with confidence and clarity.

Step 1: Financial Self-Assessment

Begin with an honest and thorough evaluation of your financial standing. Scrutinize your credit score, identify all available assets (liquid and illiquid), and meticulously track your consistent cash flow over the past 6-12 months. Understand your strengths and any potential weaknesses before approaching lenders.

Step 2: Documentation Assembly

This is where your preparation pays off. Meticulously gather every piece of alternative proof of financial stability and capacity discussed earlier – bank statements, tax returns, investment portfolio summaries, business licenses, and any significant contracts. Organize them clearly and logically.

Step 3: Research & Lender Matching

Don't cast a wide net indiscriminately. Identify specialized lenders and dealerships known for accommodating self-employed, no-income-verification scenarios. Leverage online reviews, financial forums, and direct inquiries to find partners who understand your unique financial structure.

Step 4: Pre-Approval Pursuit

Aim to secure a pre-approval offer. This step is invaluable as it solidifies your buying power, gives you a firm budget, and demonstrates to dealerships that you are a serious and qualified buyer before you even start serious car shopping.

Step 5: Negotiation Mastery

Once you have an offer, don't simply accept it. Confidently negotiate on interest rates, fees, and loan terms. Your strong financial narrative, substantial down payment, and pre-approval can be powerful leverage. Remember, everything is negotiable until the contract is signed.

Step 6: Due Diligence & Finalization

Before putting pen to paper, read every word of the contract. Understand all clauses, especially those pertaining to interest rates, fees, prepayment penalties, and any specific conditions related to alternative income verification. Clarify any ambiguities until you are completely comfortable. Only then should you sign.