Bad Credit Early Lease Buyout Options 2026 | Ontario & Canada

Table of Contents

- Bad Credit Early Lease Buyout Options 2026 | Ontario & Canada

- Key Takeaways

- I. Navigating the Road Ahead: Key Takeaways for Your Early Lease Buyout

- II. The Bad Credit Dilemma: Why an Early Lease Buyout Might Be Your Best Move in Canada

- Escaping High Monthly Payments: How Restructuring Can Provide Immediate Financial Relief

- Avoiding Costly Lease Penalties: Weighing Buyout Costs Against Early Termination Fees

- Building Equity & Credit: Turning a Depreciating Asset into a Stepping Stone for Financial Recovery

- Taking Ownership: The Freedom from Mileage Limits, Wear-and-Tear Charges, and Modification Restrictions

- Changing Needs: When Your Leased Vehicle No Longer Fits Your Lifestyle or Budget

- III. Deconstructing the 'Early Lease Buyout' for the Bad Credit Borrower

- What Exactly is an Early Lease Buyout? Beyond the Basics, Focusing on the 'Early' Aspect and Its Implications

- Understanding Your Lease Agreement: Decoding the Payout Quote, Residual Value, and Remaining Payments

- The 'Early' Factor: Calculating the True Cost of Breaking Free from your current lease

- IV. The Approval Gauntlet: Securing Financing with Less-Than-Perfect Credit in Canada

- Your Credit Score: What Lenders Really See (and How to Improve It, Even Slightly)

- Beyond the Score: Factors That Influence Bad Credit Approval

- Who Will Lend to You? Exploring Bad Credit Auto Lenders Across Canada

- Strategies for Strengthening Your Application

- V. The Real Costs of an Early Buyout with Bad Credit: Unmasking the Numbers

- Interest Rates: What to Expect with Bad Credit (and How to Shop Smartly)

- Hidden Fees & Charges: Administrative, Documentation, and Early Termination Penalties (if applicable)

- Negative Equity: When Your Car is Worth Less Than You Owe – Strategies for Managing the Gap

- Taxes and Registration: Provincial Variations (e.g., Ontario HST, Quebec Sales Tax, Alberta's lack of provincial sales tax)

- Insurance Implications: How Ownership Changes Affect Your Premiums and Coverage Requirements

- VI. Your Step-by-Step Action Plan: From Payout Quote to New Ownership

- Step 1: Obtain Your Official Lease Payout Quote (the 'Buyout Price')

- Step 2: Assess Your Vehicle's Current Market Value (using tools like Clutch.ca, AutoTrader, Canadian Black Book)

- Step 3: Secure Financing for the Buyout (Applying to Multiple Bad Credit Lenders)

- Step 4: Negotiating the Best Terms (Even with Bad Credit, There's Room to Improve Your Deal)

- Step 5: Completing the Paperwork & Transfer of Ownership from the Lessor

- Step 6: Registering Your Vehicle in Your Name at the Provincial Authorities (e.g., ServiceOntario)

- VII. Provincial Perspectives: Early Buyouts Across Canada (with a Focus on Ontario)

- Ontario Specifics: Understanding OMVIC Regulations, HST, and the Local Lender Landscape (e.g., options in Toronto, Ottawa, Hamilton)

- Western Canada Considerations: British Columbia (Vancouver), Alberta (Edmonton, Calgary) – Unique Regulations and Market Differences

- Quebec & The Maritimes: Specific Aspects of Lease Buyouts, Consumer Protection, and Tax Structures

- Navigating Dealer Networks and Provincial Consumer Protection Laws

- VIII. Beyond the Buyout: Alternative Strategies When Bad Credit Makes it Tough

- Lease Transfer: Is it a Viable Option with Bad Credit? (Challenges and potential solutions for finding a willing transferee)

- Selling Your Leased Vehicle to a Third Party (e.g., Clutch.ca, other dealerships): The process and implications for your credit

- Voluntary Repossession: The Last Resort and Its Severe Credit Impact

- Improving Your Credit Score First: A Strategic Delay for Better Future Options

- IX. Your Next Steps to Approval: Empowering Your Decision

- Consolidate Your Information: Gather all necessary documents.

- Shop Around Aggressively: Compare offers from multiple lenders.

- Don't Settle: Negotiate terms, even with bad credit.

- Prioritize Financial Health: Use this opportunity to improve your credit standing.

- Seek Professional Advice: When in doubt, consult a financial advisor.

- X. Frequently Asked Questions About Early Lease Buyouts with Bad Credit in Canada

Bad Credit Early Lease Buyout Options 2026 | Ontario & Canada

An early car lease buyout with bad credit in Canada involves securing a new loan to purchase your leased vehicle before the lease term ends, despite having a less-than-ideal credit history. This process allows you to take ownership, avoid potential end-of-lease fees, and potentially improve your financial standing, though it often comes with higher interest rates and requires careful navigation of specialized lenders and your lease agreement.

Key Takeaways

- It's Possible, But Requires Strategy: Don't dismiss the idea of an early lease buyout outright, even with bad credit. Strategic planning, understanding your options, and choosing the right lender are paramount.

- Bad Credit Means Higher Costs: Be prepared for elevated interest rates and potential additional fees. Transparency about these costs is essential for sound financial planning.

- Lender Choice is Crucial: Traditional banks may be less accessible. Specialized bad credit auto lenders, often found through dealerships or online platforms, are typically your best bet.

- Due Diligence Pays Off: Thoroughly understand your current lease contract, including the payout quote, residual value, and any early termination clauses. Knowledge is power in negotiations.

- Alternatives Exist: If a direct buyout proves too challenging or expensive, explore other options like lease transfers or selling the vehicle to a third party to mitigate financial strain.

I. Navigating the Road Ahead: Key Takeaways for Your Early Lease Buyout

Embarking on an early car lease buyout journey, especially when your credit history isn't sparkling, can feel like navigating a complex maze. But it's far from impossible. For many Canadians, particularly those in Ontario facing financial shifts, an early buyout presents a strategic exit from a lease that no longer serves them. The key is to approach this decision armed with knowledge and a clear strategy. You might be wondering if your "bad credit" label automatically closes doors. The answer, encouragingly, is no. However, it does mean the path will likely involve more careful planning, a deeper dive into your financial specifics, and a keen eye for detail. Expect to encounter higher costs due to increased risk, but also know that specialized lenders exist to help individuals in your exact situation. Understanding your current lease agreement inside and out is your first, non-negotiable step. Furthermore, if a direct buyout isn't the right fit, there are always alternative avenues to explore. This guide is designed to illuminate each turn, helping you make an informed decision for your financial future.

II. The Bad Credit Dilemma: Why an Early Lease Buyout Might Be Your Best Move in Canada

Life changes, and so do financial circumstances. What seemed like a manageable lease payment a year or two ago might now feel like a heavy burden, especially if your credit has taken a hit. For many Canadians, an early lease buyout, even with bad credit, isn't just an option—it’s a necessary strategic move to regain financial control. Why consider this path?

Escaping High Monthly Payments: How Restructuring Can Provide Immediate Financial Relief

Your current lease payment might be straining your budget. An early buyout allows you to finance the remaining value of the car, potentially at a different interest rate and over a new, longer term. This restructuring can lead to lower monthly payments, freeing up crucial cash flow. Imagine reducing your car payment from $600 to $450 per month – that's $150 back in your pocket every single month, which can make a significant difference when managing other debts or building savings.

Avoiding Costly Lease Penalties: Weighing Buyout Costs Against Early Termination Fees

Lease agreements are notorious for their end-of-term penalties. Excessive mileage, minor dents and scratches, worn tires, or even not returning the car perfectly clean can result in hundreds, if not thousands, of dollars in fees. If you foresee these penalties, buying out your lease early might actually be cheaper than paying those charges and early termination fees. Always compare the total buyout cost (including new financing interest) against the sum of remaining payments plus estimated end-of-lease penalties.

Building Equity & Credit: Turning a Depreciating Asset into a Stepping Stone for Financial Recovery

When you lease, you're essentially renting. You build no equity. By buying out your lease, you convert that rental into an asset. As you make loan payments, you build equity in the vehicle. More importantly, making consistent, on-time payments on your new auto loan is a powerful way to rebuild and improve your credit score, laying the groundwork for better financial opportunities in the future. For more on improving your credit, check out our guide on Your 'Bad Credit' Isn't a Wall. It's a Speed Bump to Your New Car, Toronto.

Taking Ownership: The Freedom from Mileage Limits, Wear-and-Tear Charges, and Modification Restrictions

Ownership brings freedom. No more worrying about exceeding those strict mileage limits, which can cost 10-20 cents per kilometre. No more fretting over every ding or scratch. Want to customize your vehicle, add a roof rack, or tint the windows? As the owner, you have that flexibility without facing lease violations.

Changing Needs: When Your Leased Vehicle No Longer Fits Your Lifestyle or Budget

Perhaps your family grew, or your commute changed, or your job now requires a different type of vehicle. An early buyout allows you to adapt. You take ownership, and then you have the flexibility to sell the car privately, trade it in for another vehicle that suits your new needs, or simply keep it if it still serves a purpose, but now with lower payments.

III. Deconstructing the 'Early Lease Buyout' for the Bad Credit Borrower

The concept of an early lease buyout can seem daunting, especially when compounded by bad credit. But let’s break it down. Understanding the mechanics is the first step towards successfully navigating this process.

What Exactly is an Early Lease Buyout? Beyond the Basics, Focusing on the 'Early' Aspect and Its Implications

An early lease buyout means you're purchasing your leased vehicle before your contract's scheduled end date. You are essentially paying off the remaining balance of the lease, which typically includes the residual value (the car's estimated value at the end of the lease), plus any outstanding monthly payments, taxes, and sometimes administrative or early termination fees. For someone with bad credit, this isn't just about convenience; it's about finding a lender willing to finance this specific amount, often requiring a new loan. The "early" aspect means you're breaking the original agreement, which sometimes comes with its own set of costs that must be factored into the overall decision.

Understanding Your Lease Agreement: Decoding the Payout Quote, Residual Value, and Remaining Payments

Your lease agreement is the foundation of this entire process. You need to obtain an "official lease payout quote" or "buyout quote" directly from your leasing company. This document is critical. It will detail: * Residual Value: This is the predetermined value of the vehicle at the end of your original lease term. It's a significant component of your buyout price. * Remaining Payments: The sum of all your scheduled monthly payments still outstanding on the lease. * Early Termination Fees: Some lease contracts include a penalty for ending the lease prematurely. Not all do, but it's crucial to check. * Sales Tax: Applied to the buyout price, this can be a substantial amount depending on your province (e.g., 13% HST in Ontario). * Administrative Fees: Small charges for processing the buyout. Understanding these components allows you to calculate the true cost of taking ownership. For further reading on financing the residual, especially in Toronto, consider our article on Your Lease Is Over. The Car's Story Isn't. Finance Full Residual, Toronto.

The 'Early' Factor: Calculating the True Cost of Breaking Free from your current lease

The "early" factor introduces complexities. While you save on potential end-of-lease wear-and-tear charges and mileage penalties, you might incur other costs. The most significant is often the interest rate on your new buyout loan, which will likely be higher due to your bad credit. You're effectively trading one financial commitment for another, aiming for one that is more manageable or strategically beneficial. The goal is to ensure the new loan's total cost (principal + interest) is less than the sum of remaining lease payments + estimated end-of-lease penalties + the cost of a new car if you were to walk away from the lease.

IV. The Approval Gauntlet: Securing Financing with Less-Than-Perfect Credit in Canada

Securing financing is arguably the biggest hurdle when attempting an early lease buyout with bad credit. Lenders assess risk, and a low credit score signals higher risk. However, it’s not an insurmountable barrier. Understanding how lenders evaluate applications and knowing where to look are your keys to success.

Your Credit Score: What Lenders Really See (and How to Improve It, Even Slightly)

Your credit score (e.g., an Equifax or TransUnion score) is a three-digit number that summarizes your creditworthiness. For lenders, it's a quick indicator of how likely you are to repay a loan. With bad credit, scores typically fall below 660, sometimes even below 580. Lenders see: * Payment History: Are payments made on time? Defaults, bankruptcies, or consumer proposals heavily impact this. * Amounts Owed: Your debt-to-credit ratio. High balances on credit cards are a red flag. * Length of Credit History: Longer, positive histories are better. * New Credit: Too many recent applications can be detrimental. * Credit Mix: A healthy mix of credit (credit cards, lines of credit, loans) shows responsible management. While a significant improvement takes time, even minor positive changes like paying down a small credit card balance or correcting errors on your credit report can help.

Beyond the Score: Factors That Influence Bad Credit Approval

Lenders specializing in bad credit look beyond just the score. They understand that life happens. They will assess: * Income Stability: Consistent employment and verifiable income are crucial. Lenders want to see that you can reliably make payments. * Debt-to-Income Ratio: Your total monthly debt payments divided by your gross monthly income. A lower ratio (ideally below 40-45%) indicates more disposable income for a new loan. * Employment History: A long, stable work history at the same employer is highly favourable. * Down Payment: A significant down payment reduces the loan amount and the lender's risk, making you a more attractive borrower. * Residency Stability: Proof of stable residence (e.g., property ownership, long-term rental) can also be a positive factor.

Who Will Lend to You? Exploring Bad Credit Auto Lenders Across Canada

The landscape of auto lenders for bad credit is diverse: * Traditional Banks (e.g., RBC, TD, BMO): Generally prefer borrowers with good to excellent credit (680+). While possible, securing a bad credit auto loan directly from a major bank for a lease buyout is often challenging unless you have an existing strong relationship or substantial assets. Their interest rates are typically the lowest for prime borrowers. * Subprime Lenders: These are financial institutions that specialize in lending to individuals with lower credit scores. They accept higher risk and, in turn, charge higher interest rates. Many dealerships have established relationships with these lenders. * Dealership Finance Departments: Often your best first stop. Dealerships, like SkipCarDealer.com, work with a network of prime and subprime lenders. They can "shop around" your application to find the best possible terms for your situation. They understand the nuances of bad credit financing. * The Rise of Online Lenders Specializing in Bad Credit Auto Loans (e.g., options available in the Greater Toronto Area): Numerous online platforms have emerged, streamlining the application process. They often have proprietary algorithms to assess risk beyond traditional credit scores and can provide quick pre-approvals. They are very convenient, especially for those in urban centres like Toronto, Ottawa, or Hamilton looking for quick solutions. Here's a simplified comparison of typical interest rate ranges:

| Lender Type | Credit Score Range | Typical Interest Rate Range (Annual Percentage Rate - APR) |

|---|---|---|

| Traditional Bank (Prime) | 680+ | 6.99% - 8.99% |

| Traditional Bank (Subprime) | 600-679 | 9.99% - 14.99% (less common) |

| Subprime Lender / Dealership (Managed Risk) | 500-650 | 15.99% - 29.99% |

| Online Bad Credit Specialist | 450-600 | 19.99% - 39.99% (can vary widely) |

Note: These rates are illustrative and can fluctuate based on market conditions, specific lender policies, loan amount, term, and individual applicant risk profile.

Strategies for Strengthening Your Application

Even with bad credit, you can improve your chances: * Finding a Co-Signer: * Pros: A co-signer with good credit significantly reduces the lender's risk, potentially securing you a lower interest rate and approval. * Cons: The co-signer is equally responsible for the loan. If you miss payments, their credit score will be negatively impacted, and they could be pursued for repayment. This is a significant responsibility and should only be undertaken with someone you trust implicitly. * Responsibilities: Both parties are legally obligated. * The Power of a Down Payment: Putting down a lump sum reduces the amount you need to borrow, thereby lowering the lender's risk. Even a few hundred or a thousand dollars can make a difference. It also reduces your monthly payments and total interest paid. * Proof of Income & Stability: Gather all necessary documents to clearly demonstrate your financial health: recent pay stubs (3-6 months), employment letters, bank statements, and tax returns (Notice of Assessment). The more comprehensive and stable your financial picture, the better. For those with variable income, like gig workers, lenders specializing in such situations can be helpful.

V. The Real Costs of an Early Buyout with Bad Credit: Unmasking the Numbers

Understanding the financial implications is critical before committing to an early lease buyout with bad credit. The costs extend beyond just the purchase price of the vehicle.

Interest Rates: What to Expect with Bad Credit (and How to Shop Smartly)

As discussed, bad credit borrowers face significantly higher interest rates. While a prime borrower might secure a loan at 7-9%, someone with a low credit score might be looking at 18-30% or even higher. This dramatically increases the total cost of the loan over its term. Let's illustrate with an example: Buyout Price: $20,000 (after all lease calculations) Loan Term: 60 months (5 years)

| Credit Profile | Interest Rate (APR) | Monthly Payment (approx.) | Total Interest Paid (approx.) | Total Cost (Principal + Interest) |

|---|---|---|---|---|

| Good Credit (700+) | 7.99% | $404 | $4,240 | $24,240 |

| Bad Credit (550) | 24.99% | $585 | $15,100 | $35,100 |

This table clearly demonstrates how a higher interest rate can add over $10,000 in interest alone over a 5-year loan term for the same principal amount. Shopping Smartly: Apply to multiple lenders. Do this within a short timeframe (e.g., 14-30 days) to minimize the impact on your credit score from multiple inquiries, as they will often be counted as a single search for a specific type of loan. Compare not just the interest rate, but also the total cost of the loan, including all fees.

Hidden Fees & Charges: Administrative, Documentation, and Early Termination Penalties (if applicable)

Beyond interest, be vigilant for various fees: * Administrative Fees: Charged by the leasing company for processing the buyout. Typically a few hundred dollars. * Documentation Fees (Doc Fees): Charged by the dealership or lender for preparing loan documents. These vary by province and dealership, often ranging from $200-$700. * Early Termination Penalties: While less common for a full buyout than a walk-away termination, some leases might have a clause. Always verify. * Lien Registration Fees: Fees to register the new lien on the vehicle, varying by province.

Negative Equity: When Your Car is Worth Less Than You Owe – Strategies for Managing the Gap

Negative equity occurs when your car's market value is less than the amount you owe on the lease buyout. This is common with new cars due to immediate depreciation. If your payout quote is $22,000 but the car is only worth $18,000, you have $4,000 in negative equity. Strategies for Managing the Gap: 1. Roll it into the new loan: The most common approach. The $4,000 negative equity is added to your new car loan, increasing your principal and monthly payments. 2. Pay the difference out of pocket: If you have savings, paying the negative equity upfront avoids accruing interest on it. 3. Negotiate: While difficult with a lease buyout, if you're working with a dealership on a trade-in, they might be able to absorb some of the negative equity into a new vehicle purchase (though this is less direct for a straight buyout).

Taxes and Registration: Provincial Variations (e.g., Ontario HST, Quebec Sales Tax, Alberta's lack of provincial sales tax)

Sales tax is applied to the buyout price of the vehicle. This is a significant cost that many overlook. * Ontario: You will pay 13% Harmonized Sales Tax (HST) on the total buyout amount. * Quebec: You will pay 5% GST + 9.975% QST, totalling 14.975% sales tax. * Alberta: You only pay 5% GST, as there is no provincial sales tax. * British Columbia: You pay 5% GST + 7% PST, totalling 12% sales tax. Beyond sales tax, you'll need to pay provincial vehicle registration fees to transfer ownership into your name. These are typically annual fees but involve a transfer fee when buying out the car.

Insurance Implications: How Ownership Changes Affect Your Premiums and Coverage Requirements

When you lease, the leasing company requires specific coverage levels (e.g., collision and comprehensive with high limits). As the owner, you still need full coverage if you have a loan, as the lender will require it. However, you might have more flexibility in choosing your insurer or adjusting deductibles down the line once the loan is paid off. Your insurance premium might change based on the car's updated declared value, your new ownership status, and any changes in usage (e.g., if you were previously driving less than the lease mileage). Always get an insurance quote for the new ownership status before finalizing the buyout.

VI. Your Step-by-Step Action Plan: From Payout Quote to New Ownership

An early lease buyout, particularly with bad credit, requires a structured approach. Follow these steps to navigate the process effectively.

Step 1: Obtain Your Official Lease Payout Quote (the 'Buyout Price')

Contact your current leasing company directly (e.g., Ford Credit, Honda Financial Services, Toyota Financial Services). Request a detailed, official "early lease buyout quote" or "payout quote." This quote is valid for a limited time (e.g., 7-10 days), so act quickly once you have it. Ensure it includes the residual value, remaining payments, any early termination fees, and applicable taxes.

Step 2: Assess Your Vehicle's Current Market Value (using tools like Clutch.ca, AutoTrader, Canadian Black Book)

Knowing your car's worth is crucial. Is it more or less than your buyout price? * Clutch.ca: Offers instant cash offers for your vehicle. * AutoTrader.ca: Allows you to browse similar vehicles for sale in your area to get a sense of market value. * Canadian Black Book (CBB): Provides wholesale and retail valuations for vehicles based on condition, mileage, and region. * Dealership Appraisal: Many dealerships offer free appraisals. This step helps you understand if you have positive equity (market value > buyout price) or negative equity (market value < buyout price), which will influence your financing needs.

Step 3: Secure Financing for the Buyout (Applying to Multiple Bad Credit Lenders)

This is where SkipCarDealer.com comes in. With your payout quote in hand, apply for an auto loan. Given your bad credit, focus on: * Dealership finance departments that specialize in bad credit. * Online bad credit auto loan specialists. * Subprime lenders. Apply to several places within a short window to compare offers. Be transparent about your credit situation. Provide all requested documentation promptly, including proof of income, employment, and residency.

Step 4: Negotiating the Best Terms (Even with Bad Credit, There's Room to Improve Your Deal)

Don't accept the first offer. Even with bad credit, there's often some room for negotiation, especially if you have multiple offers. * Interest Rate: Try to negotiate a slightly lower rate. Highlight any positive aspects of your application (stable income, good down payment). * Loan Term: A shorter term means higher monthly payments but less total interest. A longer term means lower payments but more interest. Find a balance that fits your budget. * Fees: Ask if any administrative or documentation fees can be reduced or waived. * Down Payment: If you can increase your down payment, it will directly reduce your loan amount and total interest.

Step 5: Completing the Paperwork & Transfer of Ownership from the Lessor

Once financing is approved, the new lender (or dealership facilitating the buyout) will handle paying off your original leasing company. You will sign new loan documents. The leasing company will then release their ownership interest in the vehicle.

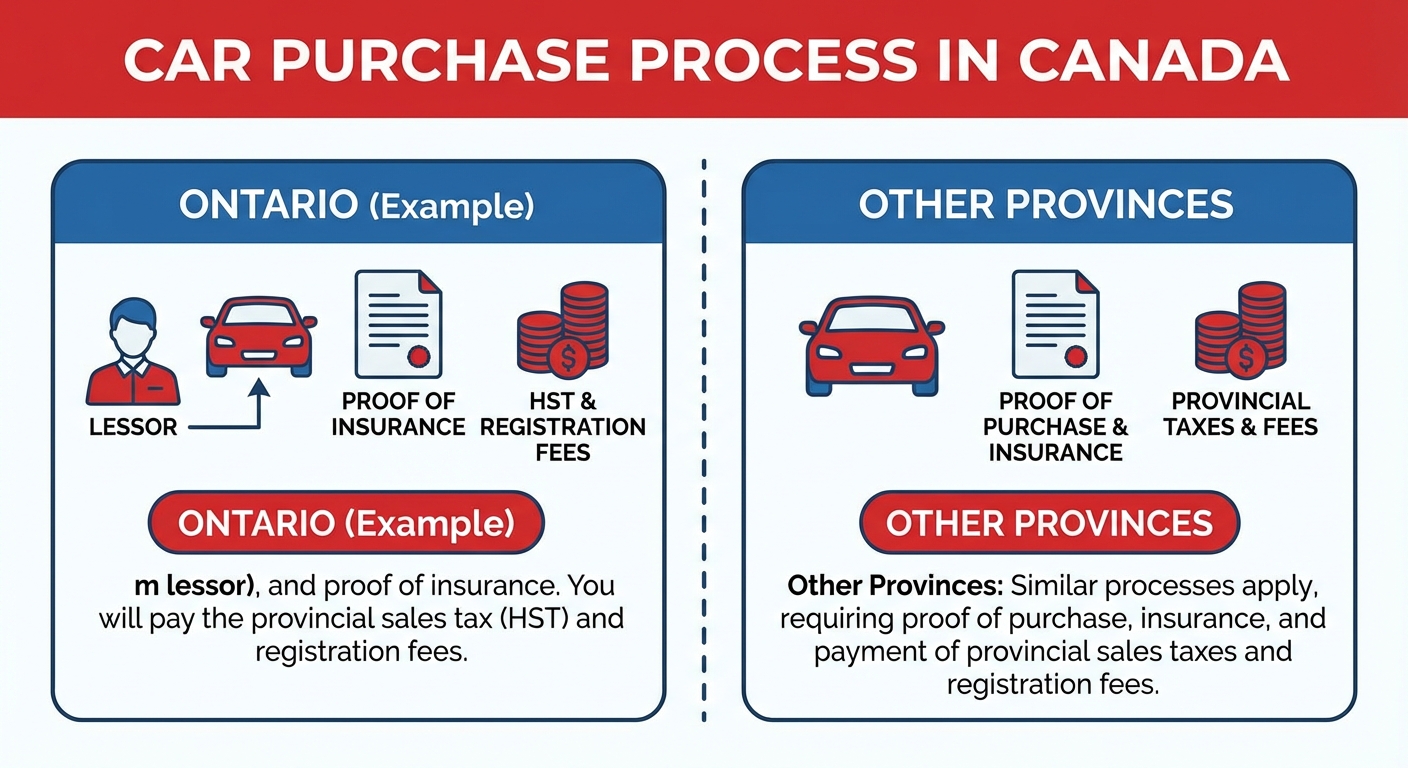

Step 6: Registering Your Vehicle in Your Name at the Provincial Authorities (e.g., ServiceOntario)

After the buyout is complete and the lien is transferred, you must register the vehicle in your name with your provincial authority.

* Ontario: Visit a ServiceOntario centre. You'll need the Bill of Sale, the vehicle's Used Vehicle Information Package (UVIP) (if applicable, often not for a direct buyout from lessor), and proof of insurance. You will pay the provincial sales tax (HST) and registration fees.

* Other Provinces: Similar processes apply, requiring proof of purchase, insurance, and payment of provincial sales taxes and registration fees.

VII. Provincial Perspectives: Early Buyouts Across Canada (with a Focus on Ontario)

While the general principles of an early lease buyout remain consistent across Canada, specific regulations, taxes, and market conditions can vary significantly by province.

Ontario Specifics: Understanding OMVIC Regulations, HST, and the Local Lender Landscape (e.g., options in Toronto, Ottawa, Hamilton)

Ontario is Canada's largest automotive market, and its regulations are robust. * OMVIC (Ontario Motor Vehicle Industry Council): This is Ontario's automotive regulator. If you're dealing with a registered dealership to facilitate your buyout or a subsequent trade-in, OMVIC provides consumer protection. They ensure fair dealing and transparency. Always ensure you're dealing with an OMVIC-registered dealer. * HST (Harmonized Sales Tax): As mentioned, a 13% HST is applied to the full buyout price in Ontario, which can be a substantial cost. * Local Lender Landscape: Major urban centres like Toronto, Ottawa, and Hamilton have a high concentration of dealerships and specialized bad credit lenders. This competition can sometimes work in your favour, allowing you to shop for better rates. Many online bad credit auto loan platforms also have strong presences in Ontario, offering tailored solutions for residents. For residents of Toronto, especially those with challenging credit, various options are available, including those discussed in our article, 450 Credit? Good. Your Keys Are Ready, Toronto.

Western Canada Considerations: British Columbia (Vancouver), Alberta (Edmonton, Calgary) – Unique Regulations and Market Differences

* British Columbia (Vancouver): In BC, you'll pay 7% PST (Provincial Sales Tax) on top of 5% GST on the buyout price. Consumer protection is provided by the Vehicle Sales Authority of BC (VSA). The market in Vancouver is competitive, with many dealerships and brokers. Given the high cost of living, managing vehicle payments through a buyout can be an attractive option for many. * Alberta (Edmonton, Calgary): Alberta stands out with only 5% GST on vehicle purchases, making the tax component of a buyout significantly lower than in other provinces. The Alberta Motor Vehicle Industry Council (AMVIC) regulates the industry. With robust economies in Calgary and Edmonton, there's a strong market for both prime and subprime lending.

Quebec & The Maritimes: Specific Aspects of Lease Buyouts, Consumer Protection, and Tax Structures

* Quebec: Quebec has a unique tax structure with 5% GST and 9.975% QST, applied sequentially, totaling 14.975%. The Office de la protection du consommateur (OPC) oversees consumer protection. Quebec's civil law system can also influence contract interpretations, so it's wise to be extra diligent. * The Maritimes (New Brunswick, Nova Scotia, Prince Edward Island, Newfoundland & Labrador): These provinces all apply HST (15% in NB, NS, NL, and PEI). Regulations are generally overseen by provincial consumer affairs departments. The market for bad credit auto loans may be slightly less competitive than in larger urban centres, but specialized online lenders still serve these regions.

Navigating Dealer Networks and Provincial Consumer Protection Laws

Regardless of your province, always ensure you're dealing with a licensed and reputable dealer or lender. Check their registration with the relevant provincial regulatory body (e.g., OMVIC in Ontario, AMVIC in Alberta, VSA in BC). These bodies exist to protect consumers and ensure fair practices. Understanding your provincial consumer protection laws gives you leverage and recourse if issues arise during the buyout process.

VIII. Beyond the Buyout: Alternative Strategies When Bad Credit Makes it Tough

Sometimes, despite your best efforts, a direct early lease buyout might not be feasible or financially advantageous with bad credit. In such cases, exploring alternative strategies can provide relief and help you manage your automotive needs without further damaging your credit.

Lease Transfer: Is it a Viable Option with Bad Credit? (Challenges and potential solutions for finding a willing transferee)

A lease transfer involves finding another individual to take over the remainder of your lease contract. * Challenges with Bad Credit: The biggest hurdle is that most leasing companies require the new transferee to undergo a credit check. If your credit is poor, it might deter potential transferees who worry about being associated with a lease that has a history of financial difficulty (even if it's yours, not the car's). Furthermore, some lessors might hold the original lessee (you) secondarily liable if the new lessee defaults. * Potential Solutions: * Incentives: Offer a cash incentive to the new transferee to make the deal more attractive. * Focus on the car's appeal: Highlight the vehicle's desirable features, low mileage, or remaining warranty. * Lease transfer platforms: Websites like LeaseBusters.com specialize in connecting individuals looking to get out of their leases with those seeking short-term lease opportunities. However, the credit check for the transferee remains a critical step.

Selling Your Leased Vehicle to a Third Party (e.g., Clutch.ca, other dealerships): The process and implications for your credit

You might be able to sell your leased vehicle directly to a third party (like a dealership or an online car buyer such as Clutch.ca). * The Process: 1. Obtain your official lease payout quote from your lessor. 2. Get an appraisal or offer from a third-party buyer. 3. If the third-party offer is higher than your payout quote, they will pay the lessor directly, and you receive the difference (positive equity). 4. If the third-party offer is lower than your payout quote (negative equity), you will need to pay the difference to the lessor to complete the sale. * Implications for Your Credit: If you have positive equity, this can be a clean exit. If you have negative equity and pay it off, it also helps your financial standing. However, if you're unable to cover the negative equity, it might still lead to further financial strain. This option can be a clean break from the lease without taking on a new loan yourself.

Voluntary Repossession: The Last Resort and Its Severe Credit Impact

Voluntary repossession (or voluntary surrender) means you return the vehicle to the leasing company because you can no longer afford the payments. This should be considered an absolute last resort. * Severe Credit Impact: A voluntary repossession will severely damage your credit score, potentially by hundreds of points, and remain on your credit report for 6-7 years. It signals to future lenders that you defaulted on a significant financial obligation. * Financial Consequences: You will still be responsible for the difference between the car's value at repossession and the outstanding balance of the lease, plus repossession fees, storage fees, and legal costs. This deficiency balance can be substantial and will be pursued by the leasing company, potentially leading to collections or legal action.

Improving Your Credit Score First: A Strategic Delay for Better Future Options

Sometimes, the best strategy is to wait. If your credit is in truly dire straits, taking a few months to focus intensely on improving it can yield significant benefits. * Pay bills on time: Consistency is key. * Reduce credit card balances: Lowering your credit utilization ratio (amounts owed vs. available credit) can boost your score. * Avoid new credit applications: Limit hard inquiries. * Check your credit report for errors: Dispute any inaccuracies. Even a modest improvement in your credit score can translate into a lower interest rate on a future buyout loan, potentially saving you thousands of dollars over the loan term. This strategic delay might be challenging, but the long-term financial benefits could outweigh the short-term inconvenience. For those with a consumer proposal, there are specific strategies for re-entering the market, as discussed in our guide Your Consumer Proposal Just Qualified You. For a Porsche.

IX. Your Next Steps to Approval: Empowering Your Decision

Navigating an early lease buyout with bad credit in Canada is undoubtedly challenging, but it is achievable with the right approach. The journey is about meticulous planning, diligent research, and proactive engagement with lenders. Your financial future depends on making informed, strategic decisions now.

Consolidate Your Information: Gather all necessary documents.

Before you even speak to a lender, have your ducks in a row. This means your official lease payout quote, recent pay stubs, employment letter, bank statements, and any other proof of income or residency. Being prepared demonstrates responsibility and speeds up the application process.

Shop Around Aggressively: Compare offers from multiple lenders.

Do not settle for the first offer you receive. Apply to several specialized bad credit lenders, dealerships, and online platforms. Compare interest rates, loan terms, and all associated fees. This competitive shopping is your best tool for securing the most favourable terms possible, even with less-than-perfect credit.

Don't Settle: Negotiate terms, even with bad credit.

Remember that every percentage point off your interest rate or every dollar saved on fees adds up significantly over the life of a loan. Use competing offers as leverage. If you can, offer a larger down payment. Negotiation is still possible, and it’s always worth the effort.

Prioritize Financial Health: Use this opportunity to improve your credit standing.

An early lease buyout, if structured correctly, can be a fresh start. By making consistent, on-time payments on your new auto loan, you are actively rebuilding your credit. View this as an investment in your financial future, paving the way for better rates and opportunities down the road.

Seek Professional Advice: When in doubt, consult a financial advisor.

If the complexities feel overwhelming, or you're unsure which path is best, consider consulting a financial advisor. They can offer personalized guidance, help you assess your overall financial picture, and recommend strategies tailored to your specific situation. This small investment can prevent costly mistakes.