The Consumer Proposal Car Loan You Were Told Was Impossible.

Table of Contents

- The Consumer Proposal Car Loan You Were Told Was Impossible.

- The Unspoken Truth: Yes, Your Consumer Proposal Car Loan Isn't a Myth

- Key Takeaways: Your Fast Track to Understanding Car Loans in a Consumer Proposal

- Beyond the 'No': Why You Were Misled About Car Loans and Consumer Proposals

- Phase 1: Securing a Car Loan *During* Your Active Consumer Proposal

- Phase 2: Unlocking Better Options *After* Your Consumer Proposal is Complete

- The Lender Landscape: Who's Willing to Say 'Yes' and What They Look For

- Crafting Your 'Impossible' Application: A Step-by-Step Guide to Approval

- The True Cost of Borrowing: Navigating Interest Rates, Fees, and Loan Terms

- Choosing Your Ride: New vs. Used, Luxury vs. Necessity

- Beyond the Purchase: Insurance, Maintenance, and Your Financial Future

- Your Next Steps to Approval: Turning 'Impossible' into 'I Did It'

- FAQ: Unpacking Common Concerns

The Consumer Proposal Car Loan You Were Told Was Impossible.

The Unspoken Truth: Yes, Your Consumer Proposal Car Loan Isn't a Myth

For many Canadians navigating the complexities of a consumer proposal, the idea of securing a car loan often feels like a distant, impossible dream. You’ve likely heard the stern warnings, the "no way" from friends, family, or even some financial advisors. The common narrative suggests that once you enter a consumer proposal, your access to credit, especially for a significant purchase like a vehicle, vanishes into thin air. But what if we told you that this widespread belief is, in fact, a myth? What if the car loan you were told was impossible is not only achievable but could also be a strategic step towards rebuilding your financial health?

At SkipCarDealer.com, we understand the challenges and the critical need for reliable transportation, especially in Canada where a vehicle is often essential for work, family, and daily life. We’re here to challenge that misconception head-on, offering a clear, practical roadmap to securing a car loan during or after a consumer proposal. This isn't about magic; it's about understanding the system, knowing your options, and applying the right strategies. Let's peel back the layers of misinformation and show you how to drive away with the financing you need, proving the naysayers wrong.

Key Takeaways: Your Fast Track to Understanding Car Loans in a Consumer Proposal

- It's Possible: Getting a car loan during or after a consumer proposal is achievable with the right strategy.

- Expect Higher Rates: Initial interest rates will likely be higher, but can improve over time.

- Alternative Lenders are Key: Traditional banks may be hesitant; explore specialized lenders.

- Down Payment Power: A significant down payment greatly improves approval odds and reduces costs.

- Credit Rebuilding Opportunity: A responsibly managed car loan can help restore your credit score.

- Preparation is Paramount: Gather documents, understand your budget, and research lenders before applying.

Beyond the 'No': Why You Were Misled About Car Loans and Consumer Proposals

The persistent myth that a car loan is unattainable during or after a consumer proposal stems from several factors, primarily a misunderstanding of how credit works post-insolvency and the cautious approach of mainstream lenders. It’s not that it's truly impossible; it's that it requires a different approach and a willingness to look beyond conventional wisdom.

The Shadow of the R7 Rating: Understanding its immediate impact and how lenders perceive it.

When you file a consumer proposal, your credit report typically receives an R7 rating. This is a significant red flag for many lenders, indicating that you are making reduced payments under a debt consolidation program. For traditional banks, an R7 rating signals a higher risk, often leading to automatic denials. They see a history of financial difficulty and are less willing to take on additional risk. This rating can linger on your credit report for up to three years after your proposal is completed, or six years from the date you filed, whichever comes first. This perceived "shadow" is what scares many people and lenders away. However, it’s crucial to understand that an R7 isn't a permanent scarlet letter; it's a temporary marker that can be overcome with strategic action. For more on how your credit score evolves after a proposal, check out our guide on Post-Proposal Car Loan: Your Credit Score Just Got a Mulligan.

The Fear Factor: Why some advise against it, and what they're missing about credit rebuilding.

Some financial advisors, while well-intentioned, may caution against taking on new debt during or immediately after a consumer proposal. Their primary concern is preventing you from falling back into financial distress. However, what they sometimes miss is the strategic power of responsible borrowing. A car loan, when managed correctly, isn't just a means of transportation; it's a powerful tool for credit rebuilding. By making consistent, on-time payments, you demonstrate financial responsibility and gradually repair your credit score. Advising against all new credit can inadvertently prolong the credit rebuilding process, keeping you in a financially vulnerable position longer than necessary.

The Long Game: How strategic borrowing can transform your financial future and prove the 'nay-sayers' wrong.

Securing a car loan after a consumer proposal is playing the long game. It's about taking a calculated risk that, with discipline, pays off significantly. Each on-time payment you make on your car loan is a positive entry on your credit report, slowly but surely replacing the negative history. Over time, this consistent positive behaviour will attract more favourable lending terms, lower interest rates, and broader financial opportunities. It’s a testament to your commitment to financial recovery and a clear message to future lenders that you are a responsible borrower. Don't let the 'impossible' narrative deter you; instead, see it as an opportunity to rewrite your financial story.

Phase 1: Securing a Car Loan *During* Your Active Consumer Proposal

Obtaining a car loan while you are still actively making payments on your consumer proposal is undeniably the more challenging scenario, but it is far from impossible. It requires a clear understanding of the hurdles, a realistic approach to expectations, and a willingness to work with specialized lenders.

The Immediate Hurdles: What lenders see on your credit report right now and how to address it.

During an active consumer proposal, your credit report prominently displays the R7 rating, signalling to lenders your current financial restructuring. This means traditional lenders will almost certainly decline your application. They view your financial situation as currently unstable, even if you are diligently making your proposal payments. To address this, you must be transparent and proactive. Explain your situation clearly to potential lenders, emphasizing your commitment to your proposal payments and your need for reliable transportation. Your goal is to demonstrate stability despite the R7 rating.

Who Will Lend to You? Navigating the world of subprime and alternative lenders specializing in 'second-chance' financing.

Forget the big banks for now. Your best bet during an active consumer proposal lies with subprime and alternative lenders. These lenders specialize in "second-chance" financing and have a business model built around assessing risk differently. They understand that life happens and that people need a chance to rebuild. They look beyond just your credit score, focusing more heavily on your current income, employment stability, and your ability to afford the monthly payments. They are more willing to work with individuals with challenged credit, albeit at higher interest rates to compensate for the increased risk.

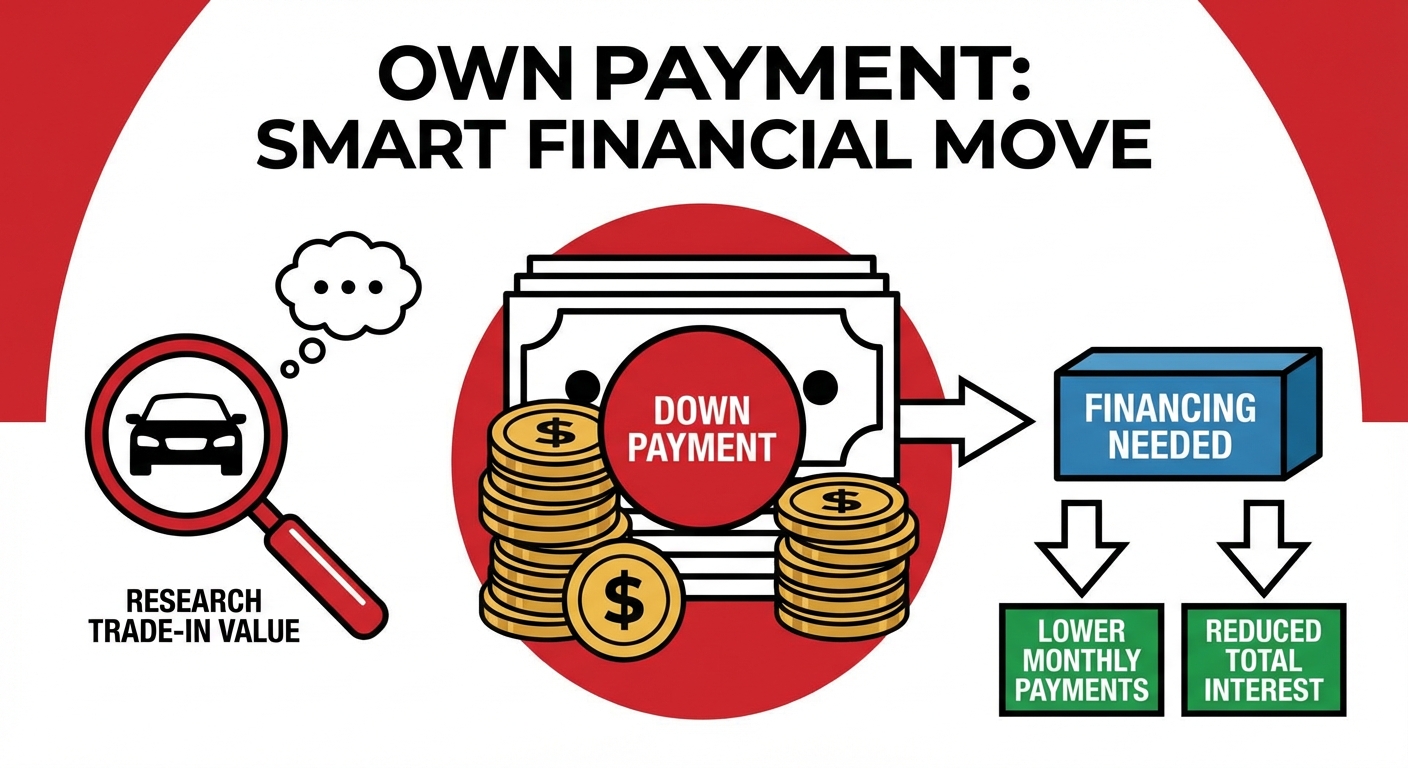

The Power of a Down Payment: Why it's non-negotiable in this phase and how it mitigates lender risk.

During an active consumer proposal, a substantial down payment transforms your loan application. It’s not just helpful; it's often non-negotiable. A down payment significantly reduces the lender's risk by lowering the amount they need to finance. It shows them you have skin in the game, demonstrating financial commitment and stability. The more you can put down, the better your chances of approval, and potentially, the slightly better your interest rate will be. Aim for at least 10-20% of the vehicle's purchase price if at all possible.

Budgeting for Reality: What kind of car can you *truly* afford without jeopardizing your proposal's success?

This is where realism must trump desire. While in a consumer proposal, your budget is already constrained. Taking on a car loan that strains your finances could jeopardize your proposal's success, which is the last thing you want. Focus on affordability. This means considering a reliable, used vehicle rather than a brand-new one. Calculate not just the monthly loan payment, but also insurance, fuel, and maintenance costs. Your goal is to secure essential transportation, not to impress. A responsible car choice now sets you up for financial success later.

Pro Tip: Prioritize Needs Over Wants – Focus on reliable, affordable transportation that won't strain your budget or risk your proposal's success. Avoid luxury or excessive features at this stage. Your primary objective is to maintain your proposal payments and rebuild credit, not to acquire a status symbol.

Phase 2: Unlocking Better Options *After* Your Consumer Proposal is Complete

Once you’ve successfully completed your consumer proposal, a significant shift occurs in your financial landscape. While the R7 rating may still linger on your credit report for a period, the "active" status is gone, and you emerge with a fresh start, opening doors to better financing options.

The Fresh Start Advantage: How completing your proposal changes your credit profile and opens new doors.

Completing your consumer proposal marks a pivotal moment. You are officially discharged from your agreed-upon debts, and this positive resolution is noted on your credit report. While the R7 rating remains for a few years, the fact that your proposal is *completed* demonstrates to lenders that you fulfilled your obligations. This significantly improves your standing compared to being in an active proposal. It signals stability and commitment, making you a more attractive borrower.

Expanding Your Lender Horizon: Exploring credit unions and some traditional banks that may now consider you.

With your proposal successfully completed, your options expand beyond just subprime lenders. Credit unions, known for their community-focused approach and willingness to work with members, may now be a viable option. They often assess applicants on a more personal basis than large banks. Some traditional banks, particularly those with specific programs for credit rebuilding, might also consider your application, especially if you have a strong down payment and stable income. For further insights into navigating this post-proposal period, explore Discharged? Your Car Loan Starts Sooner Than You're Told.

The Importance of Credit Rebuilding: Actions taken post-CP that pave the way for significantly better rates and terms.

Completing your proposal is just the beginning of your credit rebuilding journey. To truly unlock better rates and terms for future loans, you must actively work on improving your credit score. This includes:

- Obtaining a secured credit card and using it responsibly (small purchases, paid in full monthly).

- Ensuring all other bills (utilities, phone) are paid on time.

- Avoiding new, unnecessary debt.

- Monitoring your credit report for errors.

These actions demonstrate consistent financial responsibility, which lenders value immensely.

Leveraging Your Payment History: Demonstrating responsibility to potential lenders with a clean slate.

Your consumer proposal completion effectively gives you a cleaner slate. Any new credit you take on, such as a car loan, becomes a powerful tool to build a positive payment history. Lenders want to see consistency. By making every car loan payment on time, you are actively creating a track record of reliability. This history will eventually overshadow the past challenges, paving the way for lower interest rates and more favourable terms when you need to refinance or apply for future credit.

Pro Tip: Don't Jump at the First Offer – Your negotiating power increases post-CP. Shop around and compare multiple pre-approvals to secure the best rates and terms, as competition can work in your favour. Leverage any positive payment history you've built since your discharge.

The Lender Landscape: Who's Willing to Say 'Yes' and What They Look For

Understanding the different types of lenders and their specific criteria is crucial when seeking a car loan with a consumer proposal history. Not all lenders are created equal, and knowing where to focus your efforts can save you time and frustration.

Traditional Banks (The Tough Sell): Why they're often the hardest to convince and what might change their mind (e.g., strong co-signer, significant down payment).

For most traditional Canadian banks, an active or recently discharged consumer proposal is a significant hurdle. They operate with stricter lending guidelines and often use automated systems that flag R7 ratings as high risk. It's not impossible, but it requires exceptional circumstances. A very large down payment (30% or more), a strong creditworthy co-signer, or a long-standing relationship with the bank might sway them. However, for most, it's best to temper expectations and consider other avenues initially.

Credit Unions (Your Potential Ally): How their community-focused approach can be an advantage and their flexibility.

Credit unions often stand apart from big banks due to their member-focused, community-oriented structure. They tend to be more flexible in their lending decisions and may take a more holistic view of your financial situation rather than relying solely on your credit score. If you have a history with a credit union or can demonstrate a strong commitment to your financial recovery, they might be more willing to work with you, especially after your proposal is completed. They value relationships and often have programs designed to help members rebuild credit.

Alternative & Subprime Lenders (Your Most Likely Path): Understanding their business model, higher interest rates, and the value they place on current income.

These are your primary allies, especially during an active consumer proposal. Alternative and subprime lenders specialize in providing financing to individuals with challenged credit. Their business model accounts for higher risk by charging higher interest rates. What they look for is your current ability to pay: stable employment, verifiable income, and a reasonable debt-to-income ratio (DTI). They understand that past financial difficulties don't necessarily predict future behaviour, especially if you're actively rebuilding. Many dealerships work directly with these lenders, making the application process seamless.

Dealership Finance (Convenience vs. Cost): The pros and cons of in-house financing options and potential hidden markups.

Many dealerships offer in-house financing or have relationships with a network of lenders, including subprime options. This can be incredibly convenient, allowing you to apply for a loan and purchase a vehicle all in one place. However, it's crucial to be cautious. While convenient, dealership financing might sometimes come with higher interest rates or additional fees compared to securing a pre-approval elsewhere. Always compare their offers with any pre-approvals you've obtained independently.

Secured vs. Unsecured Loans: What's the difference and why a secured car loan is almost always the only option in this context.

A secured loan is backed by an asset, in this case, the car itself. If you default on the loan, the lender can repossess the vehicle. An unsecured loan, like a credit card, has no collateral. When you have a consumer proposal history, almost all car loans you'll be offered will be secured loans. This is because the vehicle acts as collateral, significantly reducing the lender's risk and making them more willing to approve your application. Understanding this distinction is key to setting realistic expectations.

Pro Tip: Consider a Co-Signer Strategically – If you have a trusted individual with strong credit willing to co-sign, it can significantly improve your chances and secure better rates. However, ensure both parties fully understand the legal and financial obligations; the co-signer is equally responsible for the debt.

Crafting Your 'Impossible' Application: A Step-by-Step Guide to Approval

The key to securing a car loan with a consumer proposal history isn't just finding the right lender; it's about presenting yourself as a responsible, low-risk borrower. A well-prepared application can make all the difference.

The Pre-Approval Power Play: Why getting pre-approved is your secret weapon for negotiation and clarity.

Getting pre-approved for a car loan before you even step foot in a dealership is a game-changer. It gives you a clear understanding of how much you can borrow, at what interest rate, and under what terms. This knowledge empowers you to shop for a vehicle within your budget, and it gives you leverage when negotiating with dealerships. You walk in as a serious buyer with financing already in hand, rather than someone hoping to get approved.

Documentation Checklist: What you *must* have ready (proof of income, CP documents, bank statements, proof of residency).

Preparation is paramount. Lenders specializing in challenged credit will want to see proof of your current financial stability. Have the following documents readily available:

- Proof of Income: Recent pay stubs (2-3 months), employment letter, T4s, or tax assessments if self-employed.

- Consumer Proposal Documents: Your proposal agreement, and ideally, proof of consistent payments or discharge papers.

- Bank Statements: Recent statements (3-6 months) to show financial activity and stability.

- Proof of Residency: Utility bills, lease agreement, or mortgage statements.

- Identification: Valid Canadian driver's licence and another piece of government-issued ID.

For more detailed information on necessary paperwork, especially in Alberta, check out Approval Secrets: Exactly What Paperwork You Need for Alberta Car Financing.

Showcasing Stability: Highlighting consistent employment, residential history, and other positive financial indicators.

Lenders are looking for stability. Emphasize any factors that demonstrate this:

- Consistent Employment: A long tenure at your current job is a huge plus.

- Residential History: Living at the same address for several years shows stability.

- Other Bills: Proof of on-time payments for utilities, phone, or rent can also help.

These elements paint a picture of a reliable individual, even with a past consumer proposal.

The Down Payment Dialogue: How much is enough, where can you get it, and its impact on your loan terms.

As discussed, a down payment is critical. Aim for at least 10-20% of the vehicle's price. Where can you get it? Savings, a tax refund, or selling an existing asset are common sources. A larger down payment not only increases your approval odds but also reduces your loan amount, leading to lower monthly payments and less interest paid over the life of the loan. It's a direct way to mitigate lender risk.

Understanding Your Debt-to-Income (DTI) Ratio: Why it's critical for lenders and practical steps to improve it.

Your Debt-to-Income (DTI) ratio is a key metric for lenders. It compares your total monthly debt payments to your gross monthly income. Lenders typically prefer a DTI below 40-45%. To improve your DTI, focus on increasing your income (if possible) or, more practically, reducing other monthly debts. Even small reductions in credit card balances or other outstanding loans can make a difference. Calculate your DTI before applying to understand where you stand.

Pro Tip: Be Transparent and Honest – Disclose your consumer proposal upfront. Lenders appreciate honesty and it builds trust, rather than having them discover it later which can lead to denial. Explain your situation confidently and highlight your commitment to financial recovery.

The True Cost of Borrowing: Navigating Interest Rates, Fees, and Loan Terms

Securing a car loan with a consumer proposal history involves more than just the monthly payment. Understanding the full cost of borrowing is paramount to making an informed decision and avoiding financial surprises.

Decoding Interest Rates: What to expect, why they're higher for challenged credit, and how they're calculated.

When you have a consumer proposal on your record, you should expect interest rates to be significantly higher than someone with excellent credit. This is simply a reflection of the increased risk lenders perceive. Rates can range from 9.99% to upwards of 29.99% or even higher, depending on your specific situation, the lender, and the vehicle. Interest is typically calculated on the remaining principal balance of your loan. Understanding that a higher interest rate means a larger portion of your early payments goes towards interest rather than the principal is crucial.

APR vs. Interest Rate: The crucial difference you need to understand for comparing loan offers.

While the interest rate tells you the cost of borrowing money, the Annual Percentage Rate (APR) provides a more comprehensive picture. APR includes not just the interest rate but also any additional fees associated with the loan, expressed as an annual percentage. Always compare APRs when looking at different loan offers, as it gives you the true annual cost of the loan and allows for a more accurate comparison between lenders.

The Long and Short of It: Analyzing loan terms (36, 48, 60+ months) and their impact on total cost vs. monthly payments.

Loan terms dictate how long you have to repay the loan. Shorter terms (e.g., 36 or 48 months) result in higher monthly payments but significantly lower total interest paid over the life of the loan. Longer terms (e.g., 60, 72, or even 84 months) offer lower monthly payments, making the car more "affordable" on a month-to-month basis, but you'll pay substantially more in interest over the long run. With higher interest rates common after a consumer proposal, opting for the shortest term you can comfortably afford is often the most financially prudent choice to minimize total cost.

Unmasking Hidden Fees: Administration fees, PPSA registrations, extended warranties, credit insurance – what to watch out for and how to negotiate.

Be vigilant for additional fees that can inflate the total cost of your loan. These might include:

- Administration Fees: For processing your loan.

- PPSA (Personal Property Security Act) Registration: To register the car as collateral.

- Extended Warranties: Often optional, but sometimes pushed hard. Consider if it's truly necessary.

- Credit Insurance (Loan Protection): Covers payments if you lose your job or become disabled. While it offers peace of mind, it adds significantly to your monthly payment and total cost.

Question every fee. Some may be non-negotiable (like PPSA), but many others, especially extended warranties and credit insurance, are optional and can often be negotiated down or declined entirely.

The Power of Early Repayment: Strategies to save on interest and accelerate your credit recovery.

If your loan agreement allows for early repayment without penalties (which most do in Canada for car loans), seize the opportunity. Paying even a small extra amount on your principal each month can significantly reduce the total interest you pay and shorten your loan term. This strategy not only saves you money but also accelerates the positive impact on your credit score, as you demonstrate even greater financial discipline.

Pro Tip: Always Read the Fine Print – Before signing anything, meticulously review the entire loan agreement. Question anything you don't understand, especially regarding interest calculations, fees, early repayment penalties, and any clauses related to default. Don't be rushed; take your time to understand every detail.

Choosing Your Ride: New vs. Used, Luxury vs. Necessity

The type of vehicle you choose has a direct impact on your loan approval, interest rate, and overall financial burden, especially when navigating a consumer proposal history. Smart choices here are crucial.

The Used Car Advantage: Why a reliable pre-owned vehicle is often the smartest choice for budget and approval.

For individuals with a consumer proposal history, a reliable used car is almost always the most sensible option.

- Lower Purchase Price: Immediately reduces the amount you need to borrow.

- Less Depreciation: Used cars have already experienced their steepest depreciation, meaning your car will hold its value better.

- Lower Insurance Costs: Generally, insurance premiums are lower for used vehicles.

- Easier Approval: Lenders are more comfortable financing a lower-value asset, especially when you're a higher-risk borrower.

Focus on well-maintained, pre-owned vehicles that meet your needs without breaking the bank.

New Car Dreams: When might it be possible, and the significant trade-offs in terms of cost and depreciation.

While a new car might seem appealing, it comes with significant drawbacks for someone rebuilding credit. New cars depreciate rapidly the moment they leave the lot. This means you immediately owe more than the car is worth, a situation known as being "upside down" on your loan. For someone with challenged credit, the higher loan amount, higher interest rates, and rapid depreciation make a new car a financially risky proposition. It's generally advisable to defer new car purchases until your credit is fully restored and you can secure prime lending rates.

Practicality Over Prestige: Focusing on features that meet your needs without overextending your budget or attracting higher rates.

This is not the time for luxury or excessive features. Your priority should be safe, reliable, and fuel-efficient transportation. A basic sedan, hatchback, or a compact SUV that gets you from point A to B without constant repairs is the ideal choice. Avoid premium models, powerful engines, or unnecessary upgrades that only increase the price and, consequently, your loan amount and interest payments. Every extra dollar borrowed with a high interest rate compounds the cost.

The Trade-In Factor: How your existing vehicle can reduce your new loan amount and boost your down payment.

If you have an existing vehicle, using it as a trade-in can be a powerful strategy. The trade-in value acts as a direct reduction of the purchase price or a significant boost to your down payment. This lowers the amount you need to finance, which in turn reduces your monthly payments and the total interest paid. Ensure you research your vehicle's trade-in value beforehand so you know what to expect and can negotiate effectively.

Beyond the Purchase: Insurance, Maintenance, and Your Financial Future

A car loan is just one piece of the puzzle. To truly achieve long-term financial stability and maximize your credit rebuilding efforts, you must consider the broader financial implications of vehicle ownership.

The Insurance Premium Punch: Expect higher rates with challenged credit and budget accordingly for comprehensive coverage.

Just as lenders view you as a higher risk, so do insurance companies. Expect your car insurance premiums to be higher, especially with a challenged credit history. This is a non-negotiable cost of vehicle ownership. Budgeting for comprehensive insurance is crucial, not just for legal compliance but for protecting your investment and preventing further financial setbacks in case of an accident or theft. Obtain quotes for the specific vehicle you're considering *before* finalizing your purchase.

Maintenance Matters: Factoring in ongoing costs for repairs, servicing, and unexpected issues.

A car is a depreciating asset that requires ongoing investment. Budget for regular maintenance (oil changes, tire rotations, brake checks) and set aside an emergency fund for unexpected repairs. Even a reliable used car will eventually need new tires or a major service. Neglecting maintenance can lead to larger, more expensive problems down the road, potentially jeopardizing your ability to make loan payments. Being proactive about maintenance protects your vehicle and your finances.

Your Car Loan as a Credit Builder: How consistent, on-time payments transform your credit score and open future opportunities.

This is the true long-term benefit of securing a car loan after a consumer proposal. Each and every on-time payment you make is reported to credit bureaus, slowly but surely building a positive payment history. This consistent positive behaviour is the most powerful factor in improving your credit score. As your score improves, you'll gain access to better financial products, lower interest rates, and more opportunities, truly transforming your financial future.

Future Refinancing Opportunities: When and how to seek better terms down the road once your credit improves.

Once you've made 12-24 months of consistent, on-time payments on your car loan and your credit score has shown significant improvement, you may be eligible to refinance your loan. Refinancing allows you to secure a lower interest rate, which can dramatically reduce your monthly payments and the total amount of interest you pay over the remaining term. This is a smart strategy to pursue once your credit has stabilized and improved. For more details on this, check out our guide on Approval Secrets: How to Refinance Your Canadian Car Loan with Bad Credit.

Pro Tip: Get Insurance Quotes *Before* You Buy – The cost of insurance can significantly impact your overall vehicle budget, especially with a challenged credit history. Obtain multiple quotes for your target vehicle before finalizing your purchase to avoid sticker shock and ensure it fits within your overall budget.

Your Next Steps to Approval: Turning 'Impossible' into 'I Did It'

The journey from consumer proposal to car loan approval is not a myth; it's a testament to resilience and strategic planning. You now have the knowledge and the roadmap. It's time to take action and turn that perceived impossibility into a personal triumph.

Assess Your Readiness: Are you truly prepared financially and mentally for this commitment?

Before you dive in, take an honest look at your financial situation. Can you comfortably afford the monthly payments, insurance, and maintenance without jeopardizing your consumer proposal or other essential living expenses? Are you mentally prepared for the commitment of consistent, on-time payments? Self-assessment is the first, crucial step.

Research, Research, Research: Lenders, vehicles, insurance – knowledge is your greatest asset.

Don't rush the process. Spend time researching alternative lenders, understanding their requirements, and comparing their pre-approval offers. Research reliable, affordable used vehicles that fit your budget and needs. Obtain multiple insurance quotes. The more informed you are, the better decisions you'll make and the stronger your position will be.

Prepare Your Documents: Have everything organized and ready to present a professional application.

Gather all necessary documentation well in advance. Having your proof of income, consumer proposal documents, bank statements, and ID organized will make the application process smoother and demonstrate your preparedness and seriousness to lenders.

Apply Strategically: Start with pre-approvals, compare offers, and don't settle for the first 'yes'.

Begin with pre-approvals from a few different alternative lenders or credit unions. This allows you to compare terms, rates, and fees without committing. Don't feel pressured to accept the first offer you receive. Leverage competition to secure the best possible terms for your situation.

Maintain Diligence: Make every payment on time, every time – this is your credit rebuilding cornerstone.

Once approved, your most important task is to make every single payment on time, without fail. This consistent positive payment history is the cornerstone of your credit rebuilding journey. It will not only ensure you keep your vehicle but, more importantly, will steadily improve your credit score, opening doors to a brighter financial future.