Your EI Is Your Down Payment. (Seriously, No Cash Needed.)

Table of Contents

- Key Takeaways

- The EI Advantage: Your Fast-Track Snapshot to a Car Loan

- Yes, It's Possible: Dispelling the Myth of EI as a Deal-Breaker

- The 'No Down Payment' Reality: What You Absolutely Need to Know

- Your Credit Score: The Unsung Hero of EI Financing

- The Lender Landscape: Who's Most Likely to Say 'Yes'?

- The Road Ahead: Why Your EI Doesn't Mean 'Roadblock' for Car Ownership

- Beyond the Stereotype: The Real Reasons You Need a Car on EI

- The EI Mindset Shift: From Temporary Support to Financial Leverage

- Unpacking EI: How Lenders *Really* See Your Temporary Income Stream

- The 'Stability Factor': Why EI Raises Eyebrows (and How to Lower Them)

- EI's Lifespan: Does the Duration of Your Benefits Matter?

- The 'Other Income' Game Changer: Supplementing EI for Stronger Applications

- Zero Down: Is It a Dream or a Deal While on EI?

- The Mechanics of a No Down Payment Loan on EI

- The Downside of No Down: Understanding the Hidden Costs and Trade-offs

- Building a 'Virtual Down Payment': Strategies When Cash Isn't an Option

- Beyond EI: Leveraging Your Entire Financial Profile for Approval

- Credit Score Alchemy: Turning Good Habits into Loan Power

- The Debt-to-Income Ratio: Your Invisible Approval Gatekeeper

- The Co-Signer Advantage: Bringing a Financial Wingman to the Table

- Navigating the Lender Labyrinth: Who's Your Best Bet on EI?

- Traditional Banks & Credit Unions: The High Bar for EI Applicants

- Dealership Finance Departments: Your Potential Ally in the Car Hunt

- Specialty & Subprime Lenders: When Traditional Paths Close, Where Else Can You Look?

- Online Loan Platforms: The Digital Fast Track (with Caveats)

- Smart Car Shopping: Matching Your Ride to Your EI Budget

- New vs. Used: The EI-Friendly Choice for Your Wallet

- Beyond the Sticker Price: Factoring in Insurance, Maintenance, and Fuel

- The 'Sweet Spot' Car: Identifying Affordable, Reliable Models

- The Application Journey: From Paperwork to Keys

- Assembling Your Approval Arsenal: Documents You Can't Afford to Forget

- The Interview: What to Say (and Not Say) to Your Loan Officer

- Life After Loan Approval: Sustainable Car Ownership on EI

- Budgeting for the Road Ahead: Beyond Just Your Car Payment

- Insurance Insights: Protecting Your Investment Without Breaking the Bank

- What If EI Runs Out? Proactive Steps to Safeguard Your Payments

- Your Next Steps to Driving Away with Confidence

- Reaffirming Possibility: Your EI is a Stepping Stone, Not a Stumbling Block

- Building Your Personal 'Approval Checklist'

- The Power of Persistence: Don't Give Up on Your Mobility Needs

- Your Burning Questions Answered: The EI Car Loan FAQ

Navigating life's transitions can be challenging, and finding yourself on Employment Insurance (EI) often brings a unique set of financial considerations. One common concern for many Canadians is how to secure essential transportation, especially when a vehicle is crucial for job searching, family responsibilities, or simply maintaining daily life. The good news? Your EI benefits aren't a roadblock to car ownership. In fact, with the right strategy and understanding, your EI can absolutely serve as the verifiable income stream you need to get approved for a car loan, even with no cash down.

Key Takeaways

- EI is Verifiable Income: Lenders can and do accept Employment Insurance as a legitimate, albeit temporary, income source for car loan applications.

- No Down Payment is Possible: Securing a car loan on EI without a down payment is achievable, especially if you have a strong credit history or a co-signer.

- Credit Score is King: A good credit score significantly improves your chances of approval and helps offset the temporary nature of EI.

- Lender Selection Matters: Dealership finance departments and specialty lenders are often more accommodating to EI recipients than traditional banks.

- Strategy is Key: Presenting a clear financial plan, demonstrating future stability, and choosing an affordable vehicle are crucial for success.

The EI Advantage: Your Fast-Track Snapshot to a Car Loan

Let's cut right to the chase: You're on EI, you need a car, and you don't have a down payment. Is this a pipe dream or a real possibility in Canada? We're here to tell you it's firmly in the realm of possibility, provided you approach it with the right information and a solid plan.

Yes, It's Possible: Dispelling the Myth of EI as a Deal-Breaker

Many people mistakenly believe that being on Employment Insurance automatically disqualifies them from obtaining a car loan. This simply isn't true. While EI is a temporary income, it is a government-regulated, verifiable income stream. Lenders, particularly those who specialize in non-traditional financing, recognize this. Your EI benefits show a consistent, albeit time-limited, ability to make payments. The key is understanding how to present this income effectively and pairing it with other strengths in your financial profile. Forget what you've heard; getting approved for a car loan while on EI is a reality for many Canadians. For more insights into challenging approval scenarios, you might find our article Denied a Car Loan on EI? They Lied. Get Approved Here. particularly helpful.

The 'No Down Payment' Reality: What You Absolutely Need to Know

The concept of a 'no down payment' car loan is enticing, especially when cash reserves might be tight due to being on EI. It's important to understand that while achievable, it often comes with trade-offs. Lenders offering zero-down options typically mitigate their risk by adjusting other aspects of the loan. This can mean higher interest rates or longer loan terms, which ultimately increase the total cost of the vehicle over time. It's not a free lunch, but it can be a necessary and viable path to getting the transportation you need now. The goal is to secure the best possible terms under your current circumstances, fully aware of the implications.

Your Credit Score: The Unsung Hero of EI Financing

When your primary income source is temporary, your credit score steps into the spotlight as one of the most critical factors in your loan application. A strong credit score (generally 650+) signals to lenders that even if your current income is temporary, you have a history of responsible financial behaviour. It indicates reliability and a lower risk profile, which can significantly outweigh concerns about the duration of your EI benefits. Conversely, a lower credit score combined with EI income can make approval much more challenging, often necessitating a co-signer or leading to less favourable terms. Understand your credit score, work to improve it if needed, and be ready to leverage it.

The Lender Landscape: Who's Most Likely to Say 'Yes'?

Not all lenders are created equal, especially when it comes to financing for EI recipients. Traditional banks and larger credit unions often have stricter lending criteria, making them a tougher sell for those relying solely on EI. Your best bet will likely be dealership finance departments and specialty finance companies. Dealerships work with a network of lenders, some of whom specialize in non-traditional income sources. Specialty lenders are specifically designed to help individuals in unique financial situations, often with more flexible approval processes. Knowing where to focus your efforts can save you time and frustration.

The Road Ahead: Why Your EI Doesn't Mean 'Roadblock' for Car Ownership

Life doesn't stop just because your employment situation has changed. For many Canadians, a car isn't a luxury; it's a fundamental tool for navigating daily life. Acknowledging this reality is the first step towards finding a solution, and that solution often involves leveraging your EI benefits strategically.

Beyond the Stereotype: The Real Reasons You Need a Car on EI

The need for a vehicle while on Employment Insurance extends far beyond mere convenience. Consider these crucial aspects:

- Job Search Mobility: Attending interviews, networking events, or even commuting to a new job often requires reliable transportation, especially in areas with limited public transit.

- Family Responsibilities: Picking up children from school, running errands, or taking family members to appointments doesn't pause.

- Medical Appointments: Accessing healthcare, especially for ongoing treatments, can be difficult without a personal vehicle.

- Maintaining Independence: A car provides freedom and reduces reliance on others, which is vital for mental well-being during a transitional period.

- Access to Essential Services: Groceries, banking, and other necessities are often more accessible with a car, particularly outside major urban centres.

Understanding and articulating these needs to a lender can sometimes help them grasp the importance of your application.

The EI Mindset Shift: From Temporary Support to Financial Leverage

It's time to reframe how you view your EI benefits. Instead of seeing them as a temporary handout, consider them a verifiable, consistent income stream that can be used as leverage. When presented correctly, EI demonstrates your ability to manage finances and meet obligations, even if for a limited duration. The key is to pair this income with a clear plan for future employment or other income sources. Lenders want to see stability and a path forward, and your EI, combined with your proactive steps, can paint that picture.

Unpacking EI: How Lenders *Really* See Your Temporary Income Stream

To successfully secure a car loan with EI, you need to understand the lender's perspective. While they acknowledge EI as income, they also have specific concerns. Addressing these concerns proactively is crucial.

The 'Stability Factor': Why EI Raises Eyebrows (and How to Lower Them)

Lenders' primary concern with EI is its temporary nature. Unlike a salaried position, EI has a defined end date, which raises questions about your ability to continue payments once benefits cease. This 'stability factor' is what makes some lenders hesitant. To lower these eyebrows, you need to demonstrate a clear path back to employment. Are you actively job searching? Enrolled in retraining? Do you have a return-to-work date? Providing evidence of these efforts can significantly reassure a lender that your EI is merely a bridge, not a permanent state.

EI's Lifespan: Does the Duration of Your Benefits Matter?

Absolutely, the remaining length of your EI claim plays a significant role in a lender's decision. If you have only a few weeks or months of benefits left, a lender will be much more hesitant than if you have several months remaining. They want to see that your EI income will comfortably cover a substantial portion of the loan term, or at least provide a strong buffer until you secure new employment. If your benefits are nearing their end, it becomes even more critical to present a robust plan for future income or consider a shorter loan term to align with your remaining benefits.

The 'Other Income' Game Changer: Supplementing EI for Stronger Applications

While EI can be your primary income, any additional income you can show will significantly bolster your application. This could include:

- Part-Time Work: Even a few hours a week of verifiable income can make a difference.

- Side Gigs/Freelancing: If you have a legitimate, consistent side hustle, document its earnings.

- Spousal or Partner Income: If you have a spouse or partner with stable employment, their income can be a massive asset, especially if they co-sign.

- Rental Income: Any verifiable income from property you own.

Every dollar of additional, verifiable income strengthens your financial picture and reduces the perceived risk associated with the temporary nature of EI.

Pro Tip 1: The 'Stability Story': Crafting Your EI Narrative for Lenders

Don't just present your EI statements; tell your story. Prepare a brief, honest explanation of your situation: why you're on EI, what steps you're taking to find new employment (e.g., job applications submitted, courses taken, networking efforts), and your expected timeline. Show them you're proactive and have a plan. This narrative, backed by documentation, can humanize your application and build trust with the loan officer. A confident, clear explanation of your future prospects can make all the difference.

Zero Down: Is It a Dream or a Deal While on EI?

The allure of a no down payment car loan is strong, especially when you're managing on EI. Let's explore the reality of this option and what it means for your finances.

The Mechanics of a No Down Payment Loan on EI

How do lenders manage to offer zero-down options, particularly to those on EI? It's often a balancing act of risk. They might:

- Adjust Interest Rates: To compensate for the lack of an upfront payment and the perceived higher risk, the interest rate on your loan might be higher. This allows the lender to recoup more money over the loan term.

- Extend Loan Terms: A longer loan term means lower monthly payments, which can make the loan more affordable on a temporary income. However, it also means you pay more interest over the life of the loan.

- Require Specific Credit Profiles: Applicants with excellent credit scores, even if on EI, are more likely to qualify for zero-down options because their financial history demonstrates reliability.

- Focus on Vehicle Value: Lenders might be more comfortable with a no-down loan on a lower-value, reliable used vehicle, as their exposure is less if something goes wrong.

For individuals looking to avoid a down payment, even in challenging financial situations, exploring options like those discussed in Your Down Payment Just Called In Sick. Get Your Car. can be beneficial.

The Downside of No Down: Understanding the Hidden Costs and Trade-offs

While convenient, a no down payment loan isn't without its potential drawbacks. It's crucial to be aware of these before committing:

| Aspect | Impact of No Down Payment | Consideration for EI Recipients |

|---|---|---|

| Interest Rates | Often higher, as the lender takes on more risk. | Increases monthly payments and total cost, potentially straining an EI budget. |

| Total Cost of Loan | Significantly higher due to increased interest paid over the loan term. | You end up paying more for the car in the long run. |

| Loan Term | May be longer to keep monthly payments affordable. | Extends your financial commitment, potentially beyond your EI benefits. |

| Negative Equity | More likely to be "upside down" (owe more than the car is worth) early on. | If you need to sell the car before the loan is paid off, you might owe money. |

| Approval Odds | Can be harder to secure without strong credit or other compensating factors. | Requires a very strong overall application to offset the lack of a down payment. |

Always calculate the total cost of the loan, not just the monthly payment, to make an informed decision.

Building a 'Virtual Down Payment': Strategies When Cash Isn't an Option

If you can't put down cash, you can still strengthen your application to mimic the security a down payment provides:

- Stellar Credit History: A long history of on-time payments and responsible credit use is your best asset.

- Reliable Co-Signer: A co-signer with excellent credit and stable income can act as a powerful 'virtual down payment' by sharing the risk.

- Lower-Value Vehicle Choice: Opting for a more affordable, reliable used car reduces the overall loan amount, making it less risky for the lender.

- Trade-In Value: If you have an existing vehicle with equity, that can serve as your down payment.

Beyond EI: Leveraging Your Entire Financial Profile for Approval

Your EI income is important, but it's just one piece of the puzzle. Lenders look at your entire financial profile. Understanding and optimizing these other elements can significantly boost your approval chances.

Credit Score Alchemy: Turning Good Habits into Loan Power

Your credit score is a snapshot of your financial responsibility. For someone on EI, a strong score can be the magic ingredient that unlocks approval. Lenders look for:

- Payment History: Consistently paying bills on time is paramount.

- Credit Utilization: Keeping your credit card balances low relative to your limits.

- Length of Credit History: A longer history of responsible credit use is generally better.

- Types of Credit: A mix of credit (e.g., credit cards, lines of credit, previous loans) can be positive.

If your credit score isn't where you want it to be, focus on improving it before applying. For a deeper dive into credit scores, check out The Truth About the Minimum Credit Score for Ontario Car Loans.

The Debt-to-Income Ratio: Your Invisible Approval Gatekeeper

Your Debt-to-Income (DTI) ratio is a critical metric lenders use to assess your ability to manage new debt. It compares your total monthly debt payments (credit cards, existing loans, rent/mortgage) to your gross monthly income (your EI benefits in this case). A lower DTI ratio indicates you have more disposable income to cover a new car payment. Before applying, calculate your DTI and, if it's high, look for ways to reduce existing debt or demonstrate higher income (e.g., through a co-signer's income). Lenders typically prefer a DTI below 40-45%.

The Co-Signer Advantage: Bringing a Financial Wingman to the Table

A co-signer can be a game-changer for EI recipients, especially if your credit is less than perfect or your EI benefits are modest. A co-signer, typically a family member or close friend with strong credit and stable income, agrees to take on legal responsibility for the loan if you default. This significantly reduces the lender's risk. However, it's a serious commitment for the co-signer, as their credit will also be impacted by the loan. Ensure both parties fully understand the responsibilities involved before proceeding.

Pro Tip 2: The Power of the Pre-Approval: Why It's Your Secret Weapon

Getting pre-approved for a car loan before you even step onto a dealership lot is incredibly powerful. A pre-approval tells you exactly how much you can afford, what your estimated interest rate will be, and demonstrates to dealerships that you are a serious buyer with financing already in place. It gives you negotiating power on the vehicle price, as the financing is no longer a question mark. Plus, it limits the number of hard inquiries on your credit report, as you're only seeking one final approval after shopping.

Navigating the Lender Labyrinth: Who's Your Best Bet on EI?

Finding the right lender is half the battle. Different types of lenders have varying appetites for risk and different criteria for approving loans, especially for those on EI.

Traditional Banks & Credit Unions: The High Bar for EI Applicants

While not impossible, securing a car loan from a major bank or credit union solely on EI can be challenging. They often prefer long-term, stable employment and may view EI as too temporary or risky. If you have an existing banking relationship, exceptional credit, and a substantial amount of EI benefits remaining, you might have a chance. However, be prepared for a higher bar and potentially more scrutiny.

Dealership Finance Departments: Your Potential Ally in the Car Hunt

Dealerships are often your best bet. They don't just offer their own financing; they have relationships with a wide network of lenders, including those who specialize in non-traditional income situations like EI. Their finance managers are experts at matching applicants with the right lender. They understand the nuances of EI and can often present your application in the most favourable light. Be aware that while convenient, rates might not always be the absolute lowest compared to if you had prime credit and stable full-time employment.

Specialty & Subprime Lenders: When Traditional Paths Close, Where Else Can You Look?

These lenders specialize in helping individuals who don't fit the mold of traditional prime borrowers. This includes those with lower credit scores, unique income situations (like EI), or past financial challenges. While they offer higher approval odds, it's common for their interest rates to be higher to compensate for the increased risk. It's crucial to understand all terms and conditions with these lenders. They can be a lifeline for getting approved, but diligent comparison shopping is essential. For those with challenging credit, articles like Zero Credit? Perfect. Your Canadian Car Loan Starts Here. offer valuable guidance.

Online Loan Platforms: The Digital Fast Track (with Caveats)

Online loan platforms offer speed and convenience, allowing you to apply from home and often receive quick decisions. Many of these platforms also work with a network of lenders, including specialty lenders, making them a good option for EI recipients. However, exercise caution: always verify the legitimacy of the lender, read reviews, and be vigilant about understanding all fees and terms before committing. The ease of application shouldn't overshadow the need for due diligence.

Pro Tip 3: Decoding the Fine Print: Interest Rates, Terms, and Fees Explained

Before you sign anything, thoroughly understand the Annual Percentage Rate (APR), the total loan term, and any associated fees. The APR includes both the interest rate and other charges, giving you a truer picture of the loan's cost. A longer term means lower monthly payments but more interest paid overall. Look out for administrative fees, origination fees, or early repayment penalties. Don't be afraid to ask questions until you fully grasp every detail. Knowledge is power, especially when it comes to your money.

Smart Car Shopping: Matching Your Ride to Your EI Budget

When your income is temporary, smart budgeting and vehicle choice become even more critical. You need a reliable vehicle that won't drain your EI benefits with unexpected costs.

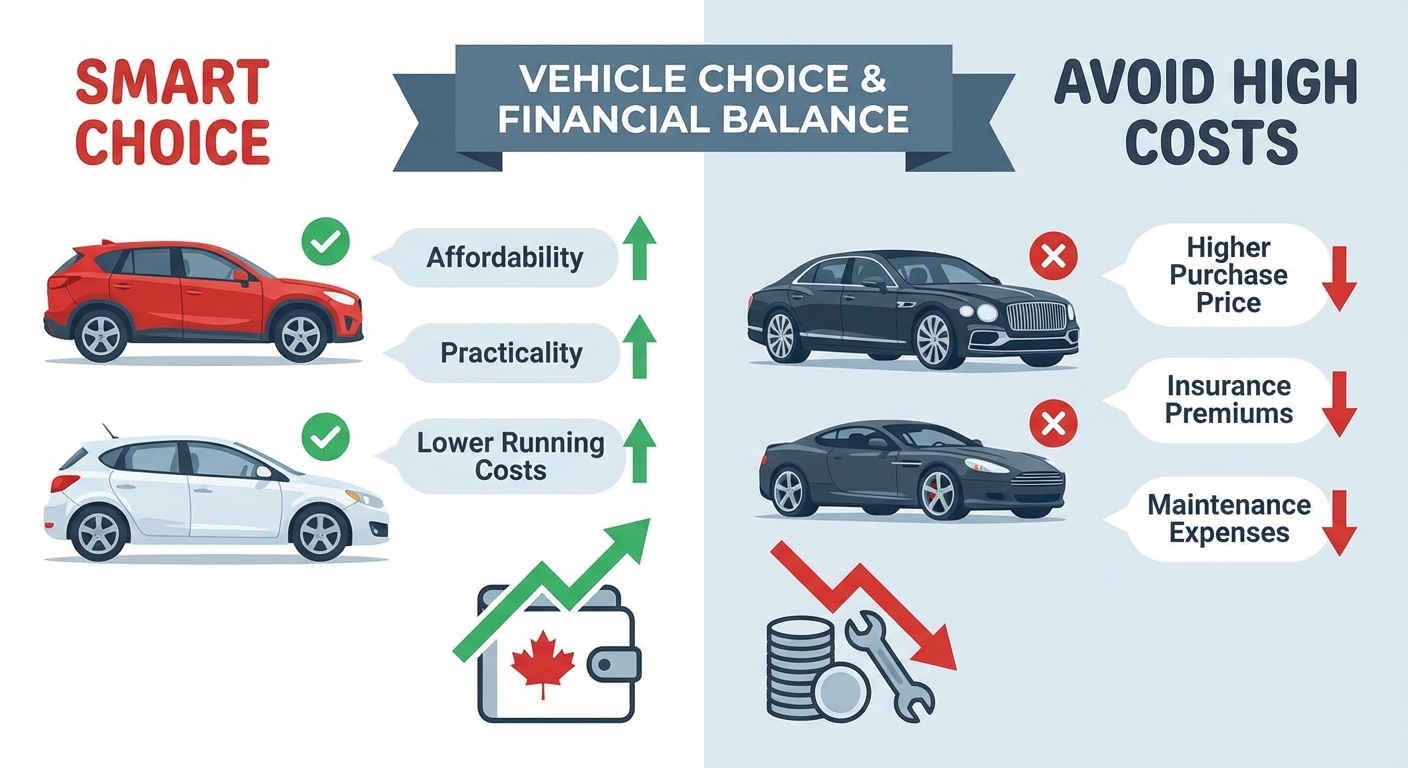

New vs. Used: The EI-Friendly Choice for Your Wallet

For most Canadians on EI, a reliable used car is the unequivocally smarter financial choice. Here's why:

| Factor | New Car | Used Car | EI Recipient Recommendation |

|---|---|---|---|

| Depreciation | Rapid, especially in the first few years. | Slower; significant depreciation already occurred. | Used: Less financial loss if you need to sell. |

| Purchase Price | Higher. | Lower. | Used: Reduces loan amount, making approval easier and payments more manageable. |

| Insurance Costs | Generally higher due to higher value. | Generally lower. | Used: Keeps monthly expenses down. |

| Loan Terms | Can be longer to offset high price. | Often shorter, reducing total interest paid. | Used: Align with temporary EI income more effectively. |

Focus on a vehicle that meets your needs without overextending your budget.

Beyond the Sticker Price: Factoring in Insurance, Maintenance, and Fuel

The monthly car payment is just one piece of the puzzle. When on EI, every dollar counts, so you must budget for the total cost of ownership:

- Car Insurance: Get quotes before you buy. Insurance can be a significant monthly expense, varying widely based on the vehicle, your driving history, and your location.

- Fuel Costs: Consider your daily commute and the vehicle's fuel efficiency.

- Maintenance & Repairs: Even reliable used cars need routine maintenance. Factor in oil changes, tire rotations, and an emergency fund for unexpected repairs.

- Registration & Licensing: Annual fees that need to be budgeted for.

The 'Sweet Spot' Car: Identifying Affordable, Reliable Models

Look for vehicles known for their reliability, fuel efficiency, and lower insurance costs. Brands like Honda, Toyota, Mazda, and certain Ford and Hyundai models often fit this description. Compact sedans, smaller SUVs, or even hatchbacks typically offer a good balance of affordability, practicality, and lower running costs. Avoid luxury vehicles or high-performance models, which come with higher purchase prices, insurance premiums, and maintenance expenses.

The Application Journey: From Paperwork to Keys

With your strategy in place and a clear understanding of what lenders look for, it's time to prepare your application. Thorough preparation is key to a smooth and successful approval process.

Assembling Your Approval Arsenal: Documents You Can't Afford to Forget

Being prepared with all necessary documents streamlines the process and demonstrates your seriousness. Gather these essentials:

- Proof of EI Income: Your 'My Service Canada Account' statements, showing benefit amounts and payment schedule.

- Proof of Identity: Government-issued photo ID (e.g., driver's license, passport).

- Proof of Residency: Utility bills, lease agreement, or other documents showing your current address.

- Bank Statements: Recent statements (3-6 months) to show financial activity and stability.

- Credit Report: Obtain a copy of your credit report (Equifax or TransUnion) so you know what lenders will see.

- Additional Income Proof: Pay stubs for part-time work, invoices for side gigs, or proof of spousal income.

- References: Some lenders may ask for personal or professional references.

The Interview: What to Say (and Not Say) to Your Loan Officer

When speaking with a loan officer, honesty and preparedness are your best tools. Be transparent about your EI status and your plans for future employment. Clearly articulate your budget and why the chosen vehicle is a practical necessity. Avoid exaggerating your future income prospects or making promises you can't keep. Focus on demonstrating your responsibility, your proactive job search, and your commitment to making payments. Remember, they're looking for reasons to say 'yes,' so give them the information they need to feel confident in your ability to repay the loan.

Pro Tip 4: The 'Future Income' Factor: Proving Your Path Beyond EI

Lenders want to know what happens when your EI runs out. Proactively provide evidence of your efforts to secure future employment. This could include: copies of job applications, interview schedules, letters from prospective employers, enrollment in vocational training programs, or a confirmed return-to-work date if you were temporarily laid off. This forward-looking information is incredibly valuable in reassuring lenders about your long-term repayment capacity.

Life After Loan Approval: Sustainable Car Ownership on EI

Getting approved is a huge step, but the journey doesn't end there. Managing your car loan and associated costs responsibly, especially while on EI, is crucial for long-term financial stability.

Budgeting for the Road Ahead: Beyond Just Your Car Payment

Create a comprehensive budget that accounts for all car-related expenses, not just the monthly loan payment. This includes:

- Fuel: Estimate your weekly or monthly fuel costs based on your driving habits.

- Insurance: Factor in your monthly or annual premiums.

- Maintenance & Repairs: Set aside a small amount each month for routine maintenance and an emergency fund for unexpected repairs.

- Emergency Fund: This is particularly vital when on a temporary income. Aim to have at least 1-3 months of essential living expenses saved.

Stick to your budget rigorously to avoid financial strain.

Insurance Insights: Protecting Your Investment Without Breaking the Bank

Car insurance is a mandatory expense in Canada, and it can vary significantly. To find affordable coverage:

- Shop Around: Get quotes from multiple insurance providers.

- Bundle Policies: If you have home or tenant insurance, bundling it with your car insurance can often lead to discounts.

- Consider Your Coverage: While full coverage is often required for financed vehicles, discuss options with your insurer to find the most cost-effective solution without compromising essential protection.

- Ask About Discounts: Many insurers offer discounts for good driving records, alarm systems, winter tires, or being a member of certain associations.

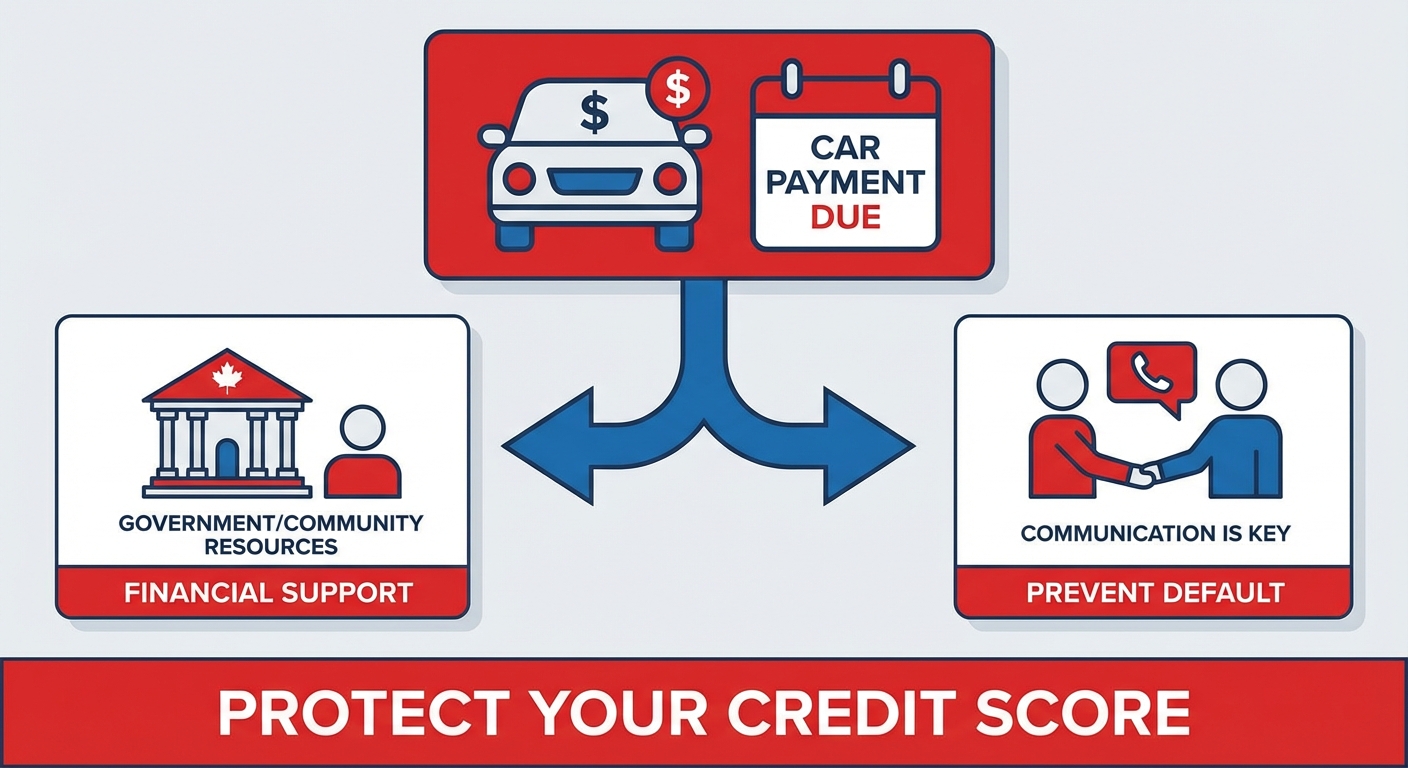

What If EI Runs Out? Proactive Steps to Safeguard Your Payments

The most important thing is to be proactive. If your EI benefits are nearing their end and you haven't secured new employment:

- Contact Your Lender IMMEDIATELY: Don't wait until you miss a payment. Explain your situation and explore options like payment deferrals or temporary adjustments.

- Seek Temporary Work: Even part-time or gig work can help bridge the gap.

- Re-evaluate Your Budget: Cut non-essential expenses to prioritize your car payment.

- Explore Government/Community Resources: Local non-profits or government agencies might offer support for individuals facing temporary financial hardship.

Communication is key to preventing default and protecting your credit score.

Your Next Steps to Driving Away with Confidence

Securing a car loan while on Employment Insurance, especially with no down payment, is a goal within reach. It requires preparation, a clear strategy, and a willingness to explore different lending avenues. By understanding how lenders view your EI income and by presenting a strong overall financial profile, you can overcome common hurdles.

Reaffirming Possibility: Your EI is a Stepping Stone, Not a Stumbling Block

Remember, your EI benefits are a legitimate form of income designed to support you during a transition. They demonstrate your ability to receive and manage funds. With the right approach, this temporary support can indeed be the stepping stone to securing the reliable transportation you need.

Building Your Personal 'Approval Checklist'

Here's a concise action plan to get you started:

- Check Your Credit Score: Understand where you stand and take steps to improve it if necessary.

- Gather All Documents: Have your EI statements, bank statements, ID, and proof of residency ready.

- Define Your Budget: Determine what you can truly afford, factoring in all costs of ownership.

- Explore Lenders: Focus on dealership finance departments and specialty lenders.

- Craft Your Stability Story: Be ready to explain your job search efforts and future income plan.

The Power of Persistence: Don't Give Up on Your Mobility Needs

If one lender says no, don't be discouraged. The lending landscape is vast, and different lenders have different criteria. Keep exploring your options, refine your application, and leverage all available resources. Your need for mobility is valid, and with persistence and the right strategy, you can drive away with confidence.