2026 Car Loan During Bankruptcy Ontario | Yes, It's Real

Table of Contents

- Key Takeaways: Your Quick Guide to Bankruptcy Car Loans in Ontario

- Key Takeaways

- The First Hurdle: Why Your Bankruptcy Status Doesn't Mean an Automatic 'No'

- The Gatekeeper: A Deep Dive into Your Trustee's Role and Getting Their Approval

- The 'Need vs. Want' Test

- The Documentation You'll Need for Your Trustee

- Decoding the Numbers: What a Bankruptcy Car Loan *Actually* Costs in Ontario

- Interest Rate Tiers

- Beyond the Rate: Uncovering Other Costs

- The Power of a Down Payment

- Real-World Scenario

- Where to Apply: Dealerships vs. Specialized Lenders in the GTA and Beyond

- Why Your Big Bank is a Long Shot

- Dealership Financing vs. Specialized Lenders

- The Application Gauntlet: Your Step-by-Step Documentation Checklist

- Your 'Approval Kit' Checklist:

- What to Expect After You Apply

- Beyond the Keys: How This Loan Impacts Your Bankruptcy & Rebuilds Your Future

- The Mechanics of Credit Rebuilding

- Managing Your Loan and Surplus Income

- The Post-Discharge Payoff

- Your Next Steps to Approval: A 3-Step Action Plan

- Frequently Asked Questions About Ontario Bankruptcy Car Loans

Navigating an active bankruptcy in Ontario is one of the most stressful financial situations a person can face. The feeling of being completely cut off from the credit world is overwhelming. But what happens when life intervenes? What if your car breaks down, or you need a reliable vehicle to get to a new job—the very job that's key to your financial recovery? The common belief is that you're stuck, that no one will lend you a dime until you're discharged. We're here to tell you that for 2026, this is a myth. Securing a car loan during active bankruptcy Ontario is not only possible; it's a real, structured process that can put you back in the driver's seat and on the road to rebuilding your credit.

This isn't just another generic article. This is the definitive guide from the trenches. We'll move past the simple "yes, you can" and dive into the specific, complex questions you have right now. We'll cover the non-negotiable role of your trustee, what these loans *actually* cost, where to go, and what paperwork you need. Let's get started.

Key Takeaways: Your Quick Guide to Bankruptcy Car Loans in Ontario

Key Takeaways

- Yes, It's Possible: You can get a car loan while in active bankruptcy in Ontario, but it requires a specific process and approvals.

- Trustee is the Gatekeeper: Your Licensed Insolvency Trustee (LIT) must approve the loan. This is a non-negotiable first step. No lender who understands the law will proceed without this.

- Expect Higher Rates: Interest rates will be higher than prime rates due to the perceived risk. The goal is reliable transportation, not the lowest rate possible. Think of it as a utility, not a luxury purchase.

- It's a Credit Rebuilding Tool: A well-managed car loan during bankruptcy can be one of the first and most powerful steps to rebuilding your credit score post-discharge.

- Lender Type Matters: Specialized lenders and certain dealership finance departments are your best bet; traditional banks will almost certainly decline your application.

The First Hurdle: Why Your Bankruptcy Status Doesn't Mean an Automatic 'No'

The very idea of applying for new credit while in bankruptcy feels counterintuitive. You've just gone through a process to handle unmanageable debt, so why would anyone lend you more money? The key is to understand how specialized lenders view your situation.

Yes, you can get a car loan while in active bankruptcy in Ontario. From a lender's perspective, your bankruptcy creates a controlled financial environment. The process has effectively wiped out or managed your other unsecured debts (like credit cards and lines of credit), meaning you have fewer competing payments. A new, secured car loan, approved by a trustee, is seen as a much lower risk than the web of debts you had before filing.

This new loan is not part of your pre-bankruptcy history; it's the first entry in your new financial chapter. Lenders who specialize in this area understand this distinction. They aren't looking at your old, damaged credit score with the same lens as a traditional bank. Instead, they're focused on two things: your current, stable income and the formal approval from your trustee.

It's crucial to set realistic expectations. This isn't a standard loan. It's a specialized financial product designed for a specific situation. The terms will be different, the process more rigorous, but the outcome—a reliable vehicle—is absolutely achievable.

The Gatekeeper: A Deep Dive into Your Trustee's Role and Getting Their Approval

Before you even think about vehicle models or colours, your entire focus must be on one person: your Licensed Insolvency Trustee (LIT). In the context of a car loan during active bankruptcy Ontario, your trustee is the ultimate gatekeeper, and their approval is mandatory.

Under the federal Bankruptcy and Insolvency Act (BIA), your trustee has a duty to your creditors. Their job is to ensure that any new debt you take on doesn't compromise your ability to make your required surplus income payments or fulfill other duties of your bankruptcy. They are not there to prevent you from living your life, but to ensure the process remains fair and viable.

The 'Need vs. Want' Test

To get your trustee's approval, you must present a compelling case based on need, not want. They will scrutinize your request.

- A "want" is wanting to upgrade from a functioning 2012 Honda Civic to a 2022 model. This will be denied.

- A "need" is when your current vehicle is unreliable and constantly needs repairs, jeopardizing your ability to get to work. Or when you've secured a new job that is inaccessible by public transit.

The context of where you live in Ontario matters immensely. A resident of downtown Toronto with robust TTC access will have a harder time proving need than someone in Barrie or Ottawa, where workplaces are dispersed and public transit may not be a practical option for their commute.

The Documentation You'll Need for Your Trustee

Go to your trustee prepared. Don't just ask for permission; present a formal case. Your chances of approval increase dramatically when you show you've thought this through. Bring a folder with:

- A Letter of Employment: Confirming your job, salary, and hours.

- A Detailed Budget Proposal: This is the most important document. It should show your current income, your bankruptcy payments, all living expenses, and a new line item for the estimated car payment and insurance. It must prove you can afford the new payment without issue.

- Potential Loan Terms: If you've had a preliminary conversation with a specialized lender, bring a sample quote showing the estimated loan amount, interest rate, and monthly payment. This shows you've done your homework.

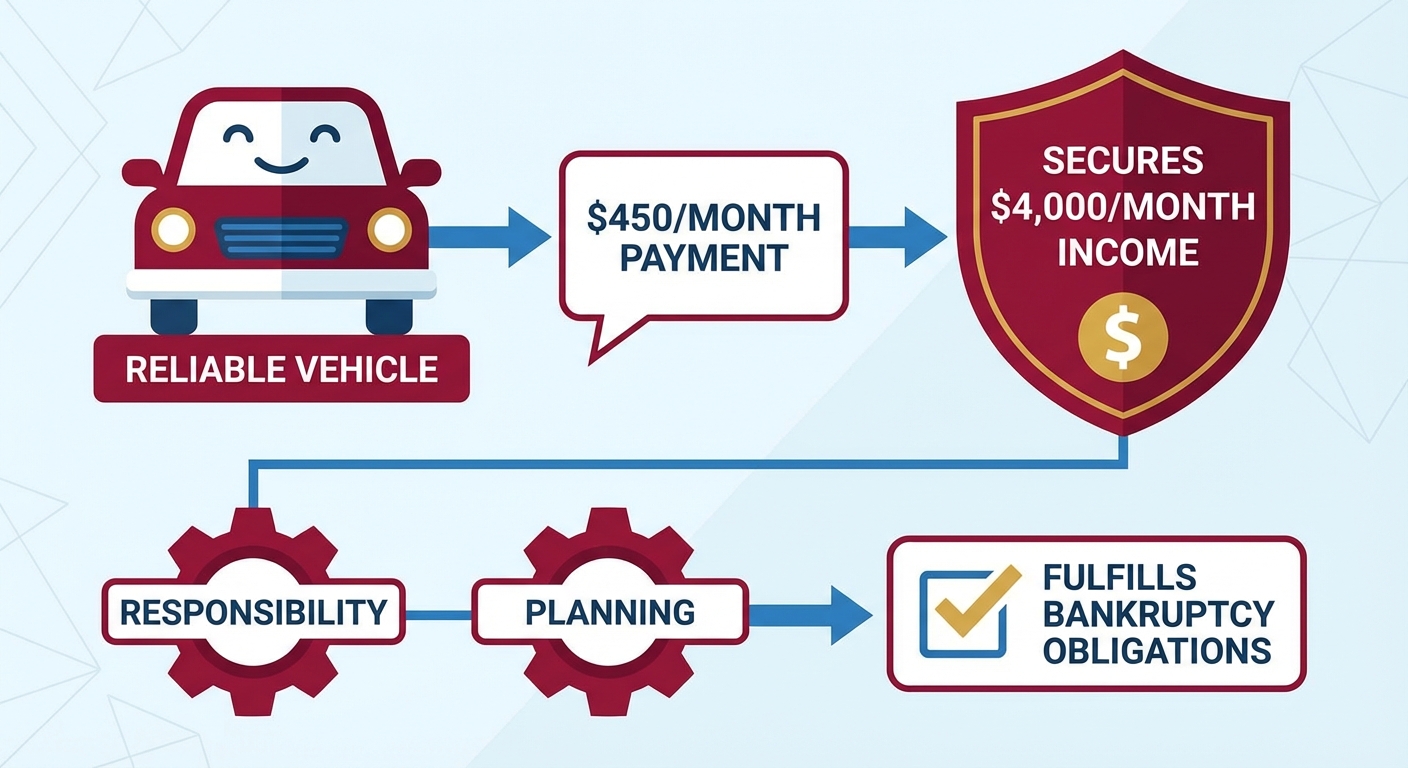

Pro Tip: Present your trustee with a detailed budget showing how the car payment fits without jeopardizing your surplus income payments. Frame the request as a tool for ensuring income stability. For example: "This reliable vehicle, with a payment of $450/month, secures my $4,000/month income, which is essential for fulfilling my bankruptcy obligations." This shows responsibility and planning.

- A clear, step-by-step flowchart graphic titled 'The Ontario Bankruptcy Car Loan Approval Path'. Steps: 1. Assess Need & Budget -> 2. Present Case to Trustee -> 3. Receive Trustee Approval Letter -> 4. Approach Lenders -> 5. Finalize Loan.

- A clear, step-by-step flowchart graphic titled 'The Ontario Bankruptcy Car Loan Approval Path'. Steps: 1. Assess Need & Budget -> 2. Present Case to Trustee -> 3. Receive Trustee Approval Letter -> 4. Approach Lenders -> 5. Finalize Loan.

Decoding the Numbers: What a Bankruptcy Car Loan *Actually* Costs in Ontario

Once you have the trustee's blessing, the focus shifts to the financial reality. It's essential to understand that you are in a high-risk lending category. The goal is to secure a fair, manageable loan for a reliable vehicle, not to find the 5.99% APR advertised on TV.

Interest Rate Tiers

In our experience, interest rates for active bankruptcy car loans in Ontario fall into specific tiers. A rate that seems high in a normal market can actually be very competitive in this space.

- Good/Excellent (10% - 18% APR): This is a strong rate in this context. It's typically offered to applicants with a stable, high income, a significant down payment, and a solid plan presented to the lender.

- Average (19% - 29% APR): This is the most common range. It reflects the lender's risk but is still manageable for many borrowers who need a vehicle. A loan in this range can still be a powerful credit-rebuilding tool.

- High-Risk (30%+ APR): While some lenders operate in this space, you should be extremely cautious. At these rates, the vast majority of your payment goes to interest, and it becomes very difficult to pay down the principal.

Beyond the Rate: Uncovering Other Costs

The APR isn't the only number to watch. Be aware of other potential costs that can be bundled into the loan:

- Administrative Fees: Some lenders charge fees for processing high-risk applications. Ask for these to be itemized.

- Mandatory Warranties: Lenders often require you to purchase an extended warranty. This protects their asset (the vehicle) from major mechanical failure, ensuring you can keep working and making payments. While an added cost, it can also provide you with peace of mind.

- Lien Registration Fees (PPSA): A standard fee in any province to register the lender's security interest in the vehicle.

The Power of a Down Payment

Even a small down payment can make a huge difference. Putting down $500, $1,000, or more shows the lender you have "skin in the game." It reduces their risk, which can lead to a slightly lower interest rate and, more importantly, a lower monthly payment. It's a powerful signal of your commitment to the new loan.

Real-World Scenario

Let's compare two hypothetical applicants in Ontario to see how their situations might affect their loan structures.

| Applicant Profile | Maria in Hamilton | David in Kenora |

|---|---|---|

| Vehicle Need | $15,000 used sedan for daily 40km commute to her nursing job. | $22,000 used 4x4 truck for construction work on rural sites. |

| Income | $55,000/year (stable) | $65,000/year (seasonal fluctuations) |

| Down Payment | $1,000 | $500 |

| Estimated APR | ~19.99% | ~24.99% (higher due to more expensive vehicle and fluctuating income) |

| Estimated Monthly Payment (60 mo) | ~$385 | ~$630 |

This illustrates how the specific vehicle needed for work and income stability directly impacts the loan's size and cost.

Where to Apply: Dealerships vs. Specialized Lenders in the GTA and Beyond

You have the trustee's letter and a realistic budget. Now, where do you go? Your choice of lender is the final critical piece of the puzzle.

Why Your Big Bank is a Long Shot

Let's get this out of the way: approaching RBC, Scotiabank, CIBC, or other major banks for a car loan during an active bankruptcy is almost always a waste of time. Their automated, credit-score-based risk models will flag the bankruptcy and issue an automatic decline. They are not set up to handle the manual review and documentation (like a trustee letter) required for these files. For those with no credit history, it's a different story, as we explain in our article No Credit? Great. We're Not Your Bank., but an active bankruptcy is a specific circumstance they typically avoid.

Dealership Financing vs. Specialized Lenders

Your viable options are dealership finance departments and standalone specialized lenders. Many large dealership groups, especially in the Greater Toronto Area (like Mississauga or Vaughan), have dedicated "special finance" or "subprime" teams that work exclusively with clients in complex situations, including bankruptcy.

- A simple comparison table: 'Who to Approach for Your Loan?' Columns: Lender Type (Dealership, Specialist Lender, Big Bank), Approval Odds, Typical Interest Rate Range, Best For...

- A simple comparison table: 'Who to Approach for Your Loan?' Columns: Lender Type (Dealership, Specialist Lender, Big Bank), Approval Odds, Typical Interest Rate Range, Best For...

| Lender Type | Approval Odds | Typical Rate Range | Best For... |

|---|---|---|---|

| Dealership Finance Dept. | High (if they specialize in it) | 15% - 29% | Convenience and a one-stop-shop experience. They have the vehicles and the financing partners. |

| Specialized/Private Lender | Very High | 10% - 30%+ | Expertise. These lenders *only* do this type of financing and understand the process inside and out. |

| Big Bank (RBC, TD, etc.) | Extremely Low | N/A | Not recommended for active bankruptcy files. |

Pro Tip: Never let a dealership run your credit with multiple lenders at once, a practice known as "shotgunning." This creates numerous hard inquiries on your credit report and can lower your score further. Work with one experienced finance manager you trust. They should know exactly which one or two lenders are best suited for your bankruptcy file and apply only to them.

The Application Gauntlet: Your Step-by-Step Documentation Checklist

Being prepared can make the difference between a quick approval and a frustrating series of delays. When you approach a lender or dealership, have your "Approval Kit" ready to go. This demonstrates that you are serious, organized, and a good candidate for a loan.

Your 'Approval Kit' Checklist:

- The Trustee's Approval Letter: This is your golden ticket. It's the first thing any legitimate lender will ask for.

- Proof of Income: Your two most recent pay stubs are standard. If you're self-employed, you may need business bank statements or Notices of Assessment.

- Proof of Address: A recent utility bill or bank statement with your name and current address.

- Valid Driver's Licence: Must be valid for the province of Ontario.

- Void Cheque or Pre-Authorized Debit Form: For setting up automatic loan payments.

- Bankruptcy Filing Number: Your unique estate number assigned when you filed.

- Down Payment (if applicable): Proof of funds, such as a bank statement.

Having this complete package makes the finance manager's job easier and signals that you are a responsible borrower.

What to Expect After You Apply

This process isn't instant. Once you submit your application and documents, the lender's underwriting team needs to manually review your file. They will verify your income, confirm the trustee's letter, and assess the deal's structure. This can take anywhere from 24 to 72 hours. Be patient. An experienced finance professional will keep you updated throughout the process.

Beyond the Keys: How This Loan Impacts Your Bankruptcy & Rebuilds Your Future

Getting the car is the immediate goal, but the long-term benefits are even more significant. A car loan is one of the most effective tools for rebuilding your credit rating, and starting that process *during* your bankruptcy gives you a powerful head start.

The Mechanics of Credit Rebuilding

This new car loan will be reported to Canada's credit bureaus, Equifax and TransUnion, as a new trade line. Every single on-time payment you make is a positive event recorded on your file. Over time, this consistent payment history builds a new foundation of creditworthiness. This is crucial because when you are discharged from bankruptcy, you won't be starting from zero; you'll already have a positive, active trade line showing lenders you can responsibly manage credit. This concept is so powerful, we've even explored how it can be more effective than traditional methods in our article, What If Your Car Loan *Was* Your Best Credit Card?.

Managing Your Loan and Surplus Income

It's vital to stick to the budget you created. Your surplus income payments to your trustee and your new car loan payment are your two most important financial obligations. Set up automatic payments for both to ensure you are never late. Success during this period proves to your trustee, your creditors, and future lenders that you are committed to your financial rehabilitation.

The Post-Discharge Payoff

After you receive your absolute discharge from bankruptcy, a new world of financial options opens up. After 6-12 months of continued on-time payments post-discharge, you may be in a position to refinance your car loan. With the bankruptcy now behind you and a proven track record of payments on the car, you could qualify for a much lower interest rate, potentially cutting your monthly payment significantly.

Your Next Steps to Approval: A 3-Step Action Plan

Feeling overwhelmed? Let's simplify it. If you're in an active bankruptcy in Ontario and need a vehicle, here is your clear, actionable plan.

- Step 1: The Budget Reality Check. Before speaking to anyone, sit down with your bank statements and pay stubs. Create a realistic budget that includes your surplus income payment and all living expenses. Determine, honestly, what extra amount you can afford for a car payment, insurance, and gas.

- Step 2: The Trustee Conversation. Schedule a meeting with your LIT. Do not email them a one-line question. Bring your budget, your letter of employment, and your clear "need-based" argument for the vehicle. Formally request their permission letter.

- Step 3: Smart Shopping. Once you have the trustee's letter in hand, contact a reputable dealership or lender that publicly states they work with bankruptcy files. Provide them with your documentation and let them find the right vehicle and financing solution for your approved budget.