![Bank Statements Only Car Refinance Canada [2026 Guide]](/images/2026-01-04_bank-statements-only-car-refinance-canada-2026-guide/cover.png)

Bank Statements Only Car Refinance Canada [2026 Guide]

Table of Contents

- Key Takeaways

- The 'Bank Statement Only' Refinance: A Lifeline for Non-Traditional Earners

- Who is This For? The Modern Earner's Dilemma

- Moving Beyond Pay Stubs and Tax Returns

- Deep Dive: Decoding Your Bank Statements Through a Lender's Eyes

- The Cash Flow Calculation: How Lenders Determine Your 'Real' Income

- Green Flags: What Underwriters Love to See

- Red Flags: What Triggers an Instant Rejection

- The Rate Reality: Unpacking the True Cost of Convenience

- Why Bank Statement Loan Rates Are Higher: The Risk Premium

- The Interest Rate Spectrum: What to Realistically Expect

- Your Application Playbook: From Document Prep to Approval

- Step 1: The Document Gauntlet (Getting Your Ducks in a Row)

- Step 2: Crafting the Narrative (Explaining Your Financial Story)

- Step 3: Finding the Right Lender (Specialists vs. Big Banks)

- Navigating the Minefield: Common Pitfalls and Lender Red Flags

- Hidden Fee #1: The 'Administration' or 'Processing' Fee

- The Prepayment Penalty Trap

- Red Flag: Pressure to Act Immediately

- Your Next Steps to a Better Car Loan

- The Decision Checklist: Is This Right for You?

- The Goal: From High-Interest Burden to Manageable Payment

- Frequently Asked Questions

You're a successful freelancer, a driven small business owner, or a hustling gig economy worker in Canada. Your monthly income is strong and consistent, yet when you tried to refinance your car loan, the bank showed you the door. Why? Because you couldn't produce the one thing their rigid system demands: a T4 slip or a traditional Notice of Assessment.

It's a frustrating, common story in today's economy. Your real-world financial health is excellent, but traditional lenders can't see past their outdated checklists. This guide is your solution. We're pulling back the curtain on how to refinance your car using the one document that tells your true financial story: your bank statements.

Key Takeaways

- Yes, It's Possible (But Different): You can absolutely refinance your car in Canada using only bank statements. This option is specifically designed for self-employed individuals, contractors, and freelancers who lack traditional income proof like pay stubs.

- Cash Flow is Your New Credit Score: In this type of financing, the consistency and volume of your bank deposits become the primary measure of your ability to pay. Lenders prioritize provable cash flow over a perfect credit history.

- Expect Higher Rates: Be prepared for the trade-off. The convenience and accessibility of a bank statement loan often mean interest rates are higher than a traditional T4-based loan due to the lender's perceived increase in risk.

- Documentation is Everything: While you don't need tax returns, the quality of your bank statements is paramount. Lenders need to see clear, consistent, and well-organized financial records for 12-24 months.

The 'Bank Statement Only' Refinance: A Lifeline for Non-Traditional Earners

Yes, you can refinance your car with bank statements only in Canada. This specialized financial product allows lenders to verify your income by analyzing the consistent deposits into your bank account over a 6 to 24-month period, bypassing the need for traditional tax documents or pay stubs. It's an essential tool for the modern self-employed professional.

Who is This For? The Modern Earner's Dilemma

Meet Alex, a successful freelance graphic designer from Calgary. His business is booming, and he consistently deposits over $10,000 a month into his business account. However, after legitimate business expenses and write-offs, his tax returns show a modest net income. When he applied to his bank to refinance his car for a lower payment, he was instantly rejected. Their system only saw the low number on his tax return, not the strong, steady cash flow his business generates.

This is the exact problem a bank statement refinance solves. It’s built for the Alexs of the world: consultants, tradespeople, e-commerce store owners, real estate agents, and anyone whose income doesn't fit neatly onto a bi-weekly paycheque.

Moving Beyond Pay Stubs and Tax Returns

Why do these loans even exist? Because there's a massive gap in the traditional lending market. The Canadian economy has changed dramatically, but big banks have been slow to adapt. They are built to serve T4 employees.

Alternative lenders and specialized finance companies like SkipCarDealer.com recognize that strong, unconventional income is still strong income. They have developed underwriting processes that focus on what truly matters for a self-employed person: actual cash flow. They understand that income from e-commerce profits, contractor payments, multiple client retainers, or gig work is just as valid as a salary—it just needs to be proven differently. For more on this, our guide Self-Employed? Your Bank Statement is Our 'Income Proof' dives even deeper into this concept.

Pro Tip: Consistency is King

Before you even think about applying, get your financial house in order. Use a single, primary business bank account for all your income deposits for at least 6 to 12 consecutive months. Avoid transferring money from personal savings to cover business expenses. This creates the cleanest, most impressive financial picture possible and makes an underwriter's job easy—which always works in your favour.

Deep Dive: Decoding Your Bank Statements Through a Lender's Eyes

To secure the best possible approval, you need to think like a lender. Your bank statements aren't just a record of transactions; they are a narrative of your financial stability and discipline. This is where expertise comes into play, and understanding the 'why' behind the process empowers you to present the strongest case.

The Cash Flow Calculation: How Lenders Determine Your 'Real' Income

Lenders don't just glance at your closing balance. They use a specific formula to calculate your qualifying income. Here’s a simplified look at the common method:

- Total Deposits: They will add up all business-related deposits over a set period, typically 12 or 24 months. Let's say your total deposits over 12 months were $120,000.

- Monthly Average: They divide the total by the number of months to get a monthly average. In this case, $120,000 / 12 = $10,000 per month.

- The Expense Factor: This is the crucial step. Since they don't have your tax returns to see your expenses, they apply a standardized 'expense factor' or 'haircut' to your gross deposits. This is an assumed percentage for business costs. It can range from 30% to 70% depending on your industry, but a 50% factor is common.

- Qualifying Income: They multiply your average monthly deposit by the inverse of the expense factor. With a 50% expense factor, your qualifying monthly income would be $10,000 * 0.50 = $5,000. This is the number they use to calculate your debt-to-income ratio.

Green Flags: What Underwriters Love to See

- Consistent Monthly Deposits: Similar deposit totals month after month show stability.

- Identifiable Sources: Deposits via e-transfer or direct deposit labelled with client or company names look professional and legitimate.

- Growing Average Balance: A trend of your average daily balance increasing over time signals a healthy, growing business.

- Minimal Large Withdrawals: Fewer large, unexplained cash withdrawals suggest good financial management.

- A Healthy Buffer: Maintaining a solid closing balance each month shows you aren't living "paycheque to paycheque."

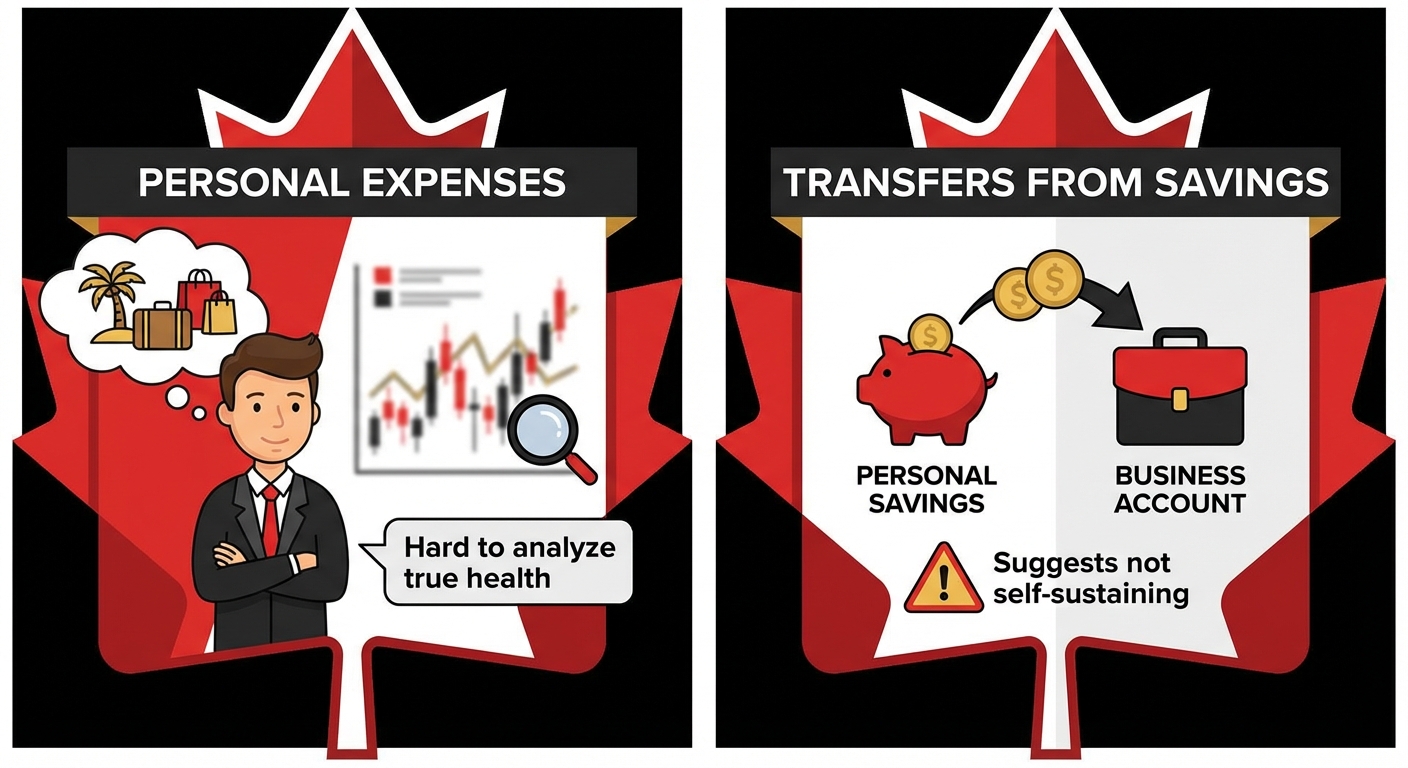

Red Flags: What Triggers an Instant Rejection

- Frequent NSF Fees: Non-Sufficient Funds (NSF) or bounced payments are a massive red flag. It tells a lender you are struggling with cash flow management.

- Numerous Overdrafts: Constantly living in your overdraft protection is another sign of financial distress.

- Erratic Cash Flow: Huge swings in income (e.g., $20,000 one month, $1,000 the next) make it difficult for lenders to predict your future ability to pay.

- Commingling Funds: Using your business account for numerous personal expenses (groceries, vacations, etc.) makes it hard for an underwriter to analyze your business's true health.

- Many Transfers from Savings: Regularly moving money from a personal savings account to cover business expenses suggests the business isn't self-sustaining.

An Annotated Bank Statement

An Annotated Bank Statement

Context: 'Visualizing the Lender's Underwriting Checklist.' This image would show a sample bank statement with green highlights on consistent deposits and a healthy ending balance, and red highlights on NSF fees and unexplained large withdrawals.

The Rate Reality: Unpacking the True Cost of Convenience

Let's address the most important question: what is this going to cost? It's crucial to be transparent here. A bank statement refinance is a powerful tool, but that power and convenience come at a price. Understanding the financial mechanics will help you set realistic expectations.

Why Bank Statement Loan Rates Are Higher: The Risk Premium

The core concept is risk-based pricing. When a lender uses a T4 slip and a Notice of Assessment, your income has been verified by a trusted third party: the Canada Revenue Agency (CRA). This is considered the gold standard of income proof.

With a bank statement loan, the lender is taking on the verification work themselves. They are trusting that your deposits accurately reflect your sustainable income. This added layer of analysis and perceived risk of income fluctuation is priced into your interest rate. This "risk premium" is the extra percentage you pay for the lender's flexibility.

The Interest Rate Spectrum: What to Realistically Expect

While rates fluctuate with the market, you can expect bank statement loan rates to be several percentage points higher than what a prime borrower with a perfect credit score and a T4 slip would receive. The better your financial picture, the smaller that premium becomes.

Here’s a realistic look at how different profiles might compare on a $30,000 car refinance over 60 months:

| Borrower Profile | Credit Score | Example Interest Rate | Estimated Monthly Payment | Total Interest Paid |

|---|---|---|---|---|

| Prime Borrower (T4 Slip) | 780+ | 7.99% | $608 | $6,480 |

| Bank Statement (Clean Statements) | 720 | 10.99% | $652 | $9,120 |

| Bank Statement (Messy Statements / Fair Credit) | 640 | 15.99% | $728 | $13,680 |

*Note: These are illustrative examples. Your actual rate will depend on your specific credit profile, vehicle details, and the lender.*

As the table shows, the difference in total interest paid can be significant. This is why cleaning up your bank statements and improving your credit score before applying can save you thousands of dollars.

Pro Tip: Your Credit Score Still Matters

While cash flow is the star of the show in a bank statement loan, your credit score is the powerful supporting actor. A strong credit score (700+) is your biggest bargaining chip. It demonstrates a history of responsible borrowing and can significantly reduce the 'risk premium' a lender adds to your interest rate. Even if your income is unconventional, a solid credit history tells lenders you're a reliable client. If you're struggling, know that Your 'Bad Credit' Isn't a Wall. It's a Speed Bump to Your New Car, Toronto.

Your Application Playbook: From Document Prep to Approval

Feeling ready to move forward? Don't just start filling out applications randomly. A strategic approach will dramatically increase your chances of success and help you secure the best terms. Think of this as your strategic plan.

Step 1: The Document Gauntlet (Getting Your Ducks in a Row)

Before you contact any lender, assemble your complete application package. Being prepared shows you're serious and organized. In our experience, clients who have all their documents ready get approved faster.

Your Checklist:

- 12-24 Months of Bank Statements: Download the complete PDF statements for every single month. Make sure every page is included, even the blank ones or marketing pages. Lenders need the full, unaltered documents.

- Void Cheque or Direct Deposit Form: For the account where you want your loan payments to be debited.

- Valid Driver's Licence: A clear photo of the front and back.

- Vehicle Ownership/Registration: Proof that the car is registered in your name.

- Current Loan Payout Statement: Contact your current lender and request a "payout statement" valid for at least 10 days. This document shows the exact amount needed to clear your existing loan.

For a detailed breakdown of paperwork, our guide on Approval Secrets: Exactly What Paperwork You Need for Alberta Car Financing can be a huge help, even if you're in another province.

The Ultimate Refinance Document Checklist

The Ultimate Refinance Document Checklist

Context: 'A simple, printable checklist to ensure you have all necessary paperwork before contacting a lender.' This graphic makes the information easy to digest and use.

Step 2: Crafting the Narrative (Explaining Your Financial Story)

Your bank statements tell most of the story, but not all of it. We highly recommend writing a brief, one-page letter of explanation to submit with your application. This is your chance to be proactive.

Explain what your business does, how you get paid, and the general nature of your income. Most importantly, use this letter to address any potential red flags. For example: "The large deposit of $15,000 in June 2025 was from a one-time project completion bonus. My typical monthly income is closer to the $8,000 average seen in other months." or "The two NSF fees in March were due to a client's delayed payment; a system is now in place to prevent this from recurring."

This professionalism can be the difference between a decline and an approval.

Step 3: Finding the Right Lender (Specialists vs. Big Banks)

Do not waste your time walking into the five major banks. They rarely, if ever, offer this type of product for auto loans. Your application will likely be rejected by an automated system before a human even sees it.

You need to work with lenders who specialize in the self-employed market. This includes:

- Alternative Lenders: Companies that focus specifically on non-traditional financing.

- Some Credit Unions: Local credit unions can sometimes be more flexible than national banks.

- Specialized Auto Finance Brokers: This is often your best bet. A brokerage like SkipCarDealer.com works with dozens of different lenders, including those who welcome bank statement programs. We know exactly which lenders are best suited for your specific profile and can shop for the best rate on your behalf.

Navigating the Minefield: Common Pitfalls and Lender Red Flags

The alternative lending space provides incredible opportunities, but it's also an area where you need to be vigilant. Building trustworthiness means protecting you, our reader, from predatory practices. Here are the most common traps to watch out for.

Hidden Fee #1: The 'Administration' or 'Processing' Fee

Some lenders charge large upfront fees, sometimes called "administration," "documentation," or "processing" fees. While a small fee can be normal, be wary of anything more than a few hundred dollars. Shady lenders may try to roll a fee of $1,000 or more into your loan, which means you're paying interest on that fee for the entire term.

The Prepayment Penalty Trap

Imagine your business has a fantastic year and you want to pay off your car loan early. A prepayment penalty is a fee the lender charges you for doing just that. It's a punishment for being financially responsible. Always ask, "Is this an open loan with no prepayment penalty?" The answer must be yes. This gives you the flexibility to pay it off faster or refinance again in the future if rates drop.

Red Flag: Pressure to Act Immediately

"This offer is only good for today!" or "You need to sign right now to lock in this rate!" This is a high-pressure sales tactic, not a sign of a good deal. A reputable lender or broker will provide you with a clear offer and give you a reasonable amount of time (at least 24-48 hours) to review the loan agreement in full before you sign. Never let anyone rush you.

Pro Tip: Request the Amortization Schedule

Before you sign any loan agreement, ask for the full amortization schedule. This is a table that breaks down every single payment you will make over the life of the loan. It clearly shows how much of each payment goes toward the principal (the actual loan amount) versus how much goes to interest (the lender's profit). This document reveals the true cost of the loan and leaves no room for hidden charges.

Your Next Steps to a Better Car Loan

You now have the insider knowledge to confidently navigate the world of bank statement car refinancing. It's a pathway designed for you, the modern Canadian entrepreneur. The goal isn't just to get a loan; it's to improve your financial position.

The Decision Checklist: Is This Right for You?

Ask yourself these final questions to be sure:

- Is your current interest rate significantly high? If you're paying 15% or more, refinancing could offer substantial savings, even with a bank statement loan.

- Is your cash flow strong and consistent? Have you reviewed your statements and confirmed they paint a positive picture?

- Have you prepared at least 12 months of clean bank statements? Do you have all the required documents from the checklist?

- Are you prepared for a rate that may be higher than traditional options? Do you understand the trade-off between convenience and cost?

The Goal: From High-Interest Burden to Manageable Payment

Refinancing your car loan isn't just about shuffling debt. It's about taking control. For a business owner or freelancer, monthly cash flow is everything. By lowering your car payment, you free up capital that can be reinvested into your business, used to pay down higher-interest debt, or simply provide a much-needed financial cushion. This is a strategic financial move to support your entrepreneurial journey.