Foreign Pension Denied? Your Lender Just Missed a Paycheque. (British Columbia)

Table of Contents

- Key Takeaways

- I. The Unrecognized Asset: Why Your Foreign Pension Should Open Car Doors in British Columbia

- A. Key Takeaways: Your Fast Track to Car Financing with Foreign Pension

- B. The Frustration of Being Overlooked: Why Lenders Miss Your Foreign Pension's Value

- II. Decoding Your Foreign Pension: What Lenders *Need* to See for Approval

- A. Beyond the Statement: Proving Stability and Reliability of Your Income

- Pro Tip 1: Pre-emptively translate and notarize *all* relevant pension documents into English or French by a certified professional. This proactive step builds trust and streamlines the assessment process.

- B. The Document Arsenal: What to Prepare (and Why Each Piece Matters)

- III. The Lender Landscape in British Columbia: Who Truly Understands Foreign Pension Income?

- A. Big Banks vs. Local Credit Unions: A Tale of Two Approaches for Newcomers

- Pro Tip 2: Prioritize credit unions or smaller regional financial institutions in British Columbia known for their robust newcomer programs. They often have more tailored approaches and dedicated advisors familiar with diverse income sources.

- B. Dealership Financing: Convenience vs. Cost for Permanent Residents

- C. Online Lenders and Specialty Finance Companies: Exploring Niche Options in British Columbia

- Pro Tip 3: Secure a pre-approval from a bank or credit union *before* stepping into a dealership. This significantly strengthens your negotiating position on both the car price and the financing terms.

- IV. Crafting Your Application: Strategic Moves for Maximizing Approval Odds

- A. The Power of a Down Payment: Why More is Always Better with Foreign Income

- B. Building a Canadian Financial Footprint (Even a Small One) Before Applying

- C. The Co-Signer Advantage: When and How to Leverage Support Effectively

- D. Targeting the Right Vehicle: Balancing Needs, Affordability, and Lender Comfort

- Pro Tip 4: For your first Canadian car, consider starting with a slightly less expensive, reliable used vehicle. This allows you to build credit history more quickly and upgrade to your dream car later.

- V. Beyond the Approval: Navigating Loan Terms and Uncovering Hidden Costs

- A. Deconstructing Your Loan Agreement: Interest Rates, APR, and Amortization Schedules

- Pro Tip 5: Never solely focus on the monthly payment. Always calculate the total amount you'll pay over the entire life of the loan, including interest, to understand the true cost.

- B. The Fine Print: Fees, Penalties, and Mandatory Insurance Requirements

- C.

- VI. British Columbia Specifics: Driving Forward in the Golden Province

- A. ICBC and Insurance Requirements: What You Need to Know as a Newcomer in British Columbia

- B. Vehicle Registration and Licensing for Permanent Residents in British Columbia

- C. City-Specific Considerations for Car Ownership and Financing in British Columbia

- D. Navigating Public Transportation vs. Car Ownership Costs in British Columbia's Major Hubs

- VII. Your Roadmap to Driving Off the Lot in British Columbia: Final Steps and Future Credit Building

- A. From Loan Approval to Keys in Hand: The Final Checklist for New Car Owners

- B. Leveraging Your Car Loan for Future Financial Success in Canada

- C. A Word of Encouragement: Your Foreign Pension is a Strength, Not a Weakness

- VIII. Frequently Asked Questions (FAQ)

Arriving in British Columbia as a permanent resident is an exciting new chapter, filled with promise and opportunity. For many, a crucial part of settling in and embracing the Canadian lifestyle is securing a reliable vehicle. But what happens when your stable, consistent foreign pension, a lifeline in your home country, seems to be a hurdle rather than a help when applying for a car loan?

You’ve worked hard, contributed to society, and now receive a well-deserved pension. This income is dependable, verifiable, and often substantial. Yet, when you approach a lender for a car loan in Vancouver, Surrey, or any other vibrant British Columbia community, you might encounter blank stares or outright rejections. It feels like your proven financial stability is being completely overlooked. Why? Because many lenders, particularly those unfamiliar with international financial nuances, are simply missing a paycheque – your foreign pension.

At SkipCarDealer.com, we understand this frustration. We know that your foreign pension isn't just a monthly deposit; it's a testament to your financial history and a solid indicator of your ability to meet financial obligations. This comprehensive guide is designed to empower permanent residents in British Columbia to confidently leverage their foreign pension income to secure the car loan you deserve, transforming a perceived weakness into a powerful asset.

Key Takeaways

- Foreign pension isn't just income; it's a stable, verifiable asset for lenders when presented correctly.

- Preparation is paramount: meticulous documentation, professional translation, and clear communication are non-negotiable.

- Not all lenders are equal; understanding the landscape and knowing where to look makes all the difference for newcomers.

- Securing a car loan with foreign pension isn't just about getting a car; it's a strategic step towards establishing a robust Canadian credit history and financial footprint.

I. The Unrecognized Asset: Why Your Foreign Pension Should Open Car Doors in British Columbia

Imagine this: you've planned your move to British Columbia meticulously, chosen your new neighbourhood, and are eager to explore the province’s stunning landscapes. A car isn't just a convenience; it's often a necessity for navigating sprawling cities like Surrey, commuting to work in Richmond, or simply enjoying the freedom of the open road from Victoria to Kelowna. Your foreign pension is your key to unlocking this mobility, but only if lenders recognize its true value.

A. Key Takeaways: Your Fast Track to Car Financing with Foreign Pension

For many permanent residents, the concept of a foreign pension as a car loan asset is revolutionary. It shifts the perspective from "I don't have Canadian credit" to "I have a stable income that supports a loan." This isn't just about proving you have money; it's about demonstrating financial consistency and responsibility, which are universal lending principles. When you approach a lender armed with the right knowledge and documentation, your foreign pension becomes an undeniable force in your favour.

The journey to car financing begins with meticulous preparation. Think of it as building your financial case. Every document, every translation, and every conversation contributes to a lender's confidence in your ability to repay. This proactive approach not only increases your chances of approval but also often leads to more favourable terms. Moreover, understanding that the Canadian lending landscape isn't monolithic is crucial. There are institutions and strategies specifically geared towards newcomers, and knowing where to focus your efforts can save you significant time and frustration. Ultimately, successfully leveraging your foreign pension for a car loan is more than just buying a car; it's a foundational step in building a strong financial presence in Canada.

B. The Frustration of Being Overlooked: Why Lenders Miss Your Foreign Pension's Value

The primary barrier for many newcomers, including those with substantial foreign pensions, is the 'Canadian Credit History' wall. Lenders in Canada heavily rely on a credit score and history built within the Canadian financial system to assess risk. Without this history, even impeccable financial records from another country can be difficult for automated systems and less experienced loan officers to process.

Navigating unfamiliar income sources presents another significant challenge. Traditional financial institutions often struggle with assessing non-Canadian income streams due to a lack of standardized procedures for verification, concerns about currency fluctuations, and unfamiliarity with foreign tax laws or pension systems. This isn't necessarily a reflection of your financial standing, but rather an institutional blind spot.

The specific case of permanent residents in British Columbia can involve unique regional considerations. While British Columbia is a diverse province welcoming immigrants from around the globe, lender perceptions can still vary. Some lenders, especially smaller, local institutions, might have more experience or a greater willingness to work with diverse income streams, understanding the unique needs of Vancouver's or Richmond's multicultural populations. However, others may default to conservative national policies that don't easily accommodate international income. This means your approach needs to be strategic, targeting lenders who are more attuned to the newcomer experience. For more on navigating the initial hurdles, you might find our article New to Canada? Your Permanent Resident Auto Loan Starts Before Your Credit Does, Vancouver particularly helpful.

II. Decoding Your Foreign Pension: What Lenders *Need* to See for Approval

To turn your foreign pension into a recognized asset, you must translate its stability and reliability into terms that Canadian lenders understand and trust. This involves more than just showing a bank statement; it requires a comprehensive presentation of your financial narrative.

A. Beyond the Statement: Proving Stability and Reliability of Your Income

Foreign pensions come in various forms: government pensions (e.g., state social security, civil service pensions), corporate pensions (from former employers), and private pensions (annuities, personal retirement accounts). Canadian lenders generally view government and established corporate pensions as highly stable and reliable, often comparable to Canadian government benefits. Private pensions might require more detailed documentation to prove their consistent payout structure.

Addressing currency conversion and stability is crucial. Lenders will naturally be concerned about exchange rate fluctuations impacting your real income in Canadian dollars. Strategies to mitigate these concerns include:

- Demonstrating a history of consistent direct deposits into a Canadian bank account, showing that you've been managing currency conversions successfully.

- Highlighting any hedges or financial instruments you use to protect against significant currency swings (though this is less common for car loans).

- Focusing on the long-term stability of the pension source rather than short-term currency volatility.

Remember, the goal is to paint a picture of predictable, dependable income, regardless of its origin. For insights into how other non-traditional incomes are viewed, you might be interested in Your Government Cheque Just Rewrote Your Car Loan. Seriously, Vancouver.

Pro Tip 1: Pre-emptively translate and notarize *all* relevant pension documents into English or French by a certified professional. This proactive step builds trust and streamlines the assessment process.

Waiting for a lender to request translations can cause significant delays. Having them ready demonstrates preparedness and professionalism, making your application much more appealing.

B. The Document Arsenal: What to Prepare (and Why Each Piece Matters)

Your documentation is your undeniable proof. Gather these items with care:

- Official pension statements: Originals and their certified translations are essential. These documents should clearly detail the payment amounts, frequency (monthly, quarterly), and the issuing authority. This proves the existence and value of your pension.

- Proof of consistent payment: Provide bank statements (Canadian preferred, showing direct deposits over several months; or foreign with clear transaction history and certified translations) to demonstrate that the pension is indeed being paid regularly and deposited into your accounts. This verifies the income stream in practice.

- Proof of permanent residency status in Canada: Your Permanent Resident (PR) card and other immigration documents (e.g., Confirmation of Permanent Residence) establish your legal right to reside in Canada and your long-term commitment to the country, which reassures lenders about your stability.

- Income tax returns: If applicable, tax filings from your home country (with certified translations) and any Canadian tax filings (even if you've only filed for a short period) help demonstrate your overall financial picture and compliance with tax regulations. This provides a comprehensive view of your financial health.

III. The Lender Landscape in British Columbia: Who Truly Understands Foreign Pension Income?

Not all lenders are created equal, especially when it comes to assessing non-traditional income sources like foreign pensions. Understanding the different types of financial institutions in British Columbia can significantly impact your success.

A. Big Banks vs. Local Credit Unions: A Tale of Two Approaches for Newcomers

Canada's major banks, such as the Royal Bank of Canada (RBC), TD Canada Trust, Scotiabank, BMO, and CIBC, often have "newcomer" programs designed to help permanent residents establish banking relationships. However, their general auto loan policies can still be quite rigid when it comes to specific, detailed foreign income assessment, especially without an established Canadian credit history. While they might be excellent for opening bank accounts or getting secured credit cards, securing a car loan directly from a big bank with only foreign pension income can be challenging due to their automated underwriting systems.

Credit unions in British Columbia, on the other hand, are often more flexible, community-focused, and potentially more receptive to individualized income assessments. Institutions like Vancity, Coast Capital Savings, and Prospera Credit Union operate with a more local focus and may have dedicated advisors familiar with diverse income sources, including foreign pensions. They often pride themselves on serving their community members, which can include newcomers with unique financial situations.

| Feature | Big Banks (e.g., RBC, TD) | Credit Unions (e.g., Vancity, Coast Capital) |

|---|---|---|

| Approach to Foreign Pension | Often rigid, relies on standardized Canadian credit history. May struggle with non-standard verification. | More flexible, willing to assess individual circumstances. Stronger emphasis on relationship banking. |

| Newcomer Programs | Exist, but often focus on basic banking and credit building tools (secured credit cards). | Often include more tailored advice and willingness to consider broader income documentation. |

| Speed of Approval | Can be faster if you fit standard criteria, but slower if manual review for foreign income is needed. | May involve more personalized review, potentially longer initial assessment but higher approval rate. |

| Geographic Focus | National/International presence, standardized policies across all branches. | Local/Regional focus, policies can be more adaptable to local community needs in British Columbia. |

Pro Tip 2: Prioritize credit unions or smaller regional financial institutions in British Columbia known for their robust newcomer programs. They often have more tailored approaches and dedicated advisors familiar with diverse income sources.

Don't be afraid to visit a few branches, explain your situation, and ask about their policies for permanent residents with foreign pension income. A personal conversation can make all the difference.

B. Dealership Financing: Convenience vs. Cost for Permanent Residents

The 'one-stop shop' appeal of car dealerships is undeniable. Many dealerships in British Columbia, from large chains in Vancouver to independent lots in Kelowna, facilitate loans directly through their finance departments. They often work with a network of lenders, including subprime lenders, which can make them a viable option even for challenging cases like those with foreign income and no Canadian credit history. However, this convenience often comes at a price.

Understanding potential dealer markups and financing rates specifically for foreign income scenarios is crucial. Dealerships might be able to get you approved, but the interest rates could be significantly higher to offset the perceived risk. Always be wary of rates that seem excessive. While they offer a path to ownership, it's vital to compare their offerings with other options to ensure you're getting a fair deal.

C. Online Lenders and Specialty Finance Companies: Exploring Niche Options in British Columbia

When traditional routes fall short, online lenders and specialty finance companies can offer solutions. Many of these lenders specialize in non-traditional income sources, bad credit, or newcomer financing. They often have more flexible underwriting criteria and a greater understanding of diverse financial backgrounds. SkipCarDealer.com, for instance, connects you with a network of lenders who are specifically equipped to handle unique financial situations, including foreign pension income.

However, due diligence is required. The online lending landscape can include both reputable platforms and predatory lenders. Always research a company's reputation, read reviews, and ensure they are licensed to operate in British Columbia. Check for transparent terms and conditions and avoid any lender that pressures you into quick decisions or demands upfront fees without a clear loan offer.

Pro Tip 3: Secure a pre-approval from a bank or credit union *before* stepping into a dealership. This significantly strengthens your negotiating position on both the car price and the financing terms.

Having a pre-approval in hand shows the dealership you're a serious buyer with financing already secured, giving you leverage to negotiate a better deal on the vehicle itself.

IV. Crafting Your Application: Strategic Moves for Maximizing Approval Odds

Your foreign pension is a strong foundation, but a well-crafted application goes further. Strategic moves can significantly improve your chances of approval and secure more favourable loan terms.

A. The Power of a Down Payment: Why More is Always Better with Foreign Income

A substantial down payment is one of the most effective ways to reduce perceived risk for lenders, especially when income sources are non-traditional or new to the Canadian system. It demonstrates your financial commitment and reduces the amount you need to borrow, which in turn lowers the lender's exposure. The direct impact of a substantial down payment on interest rates and overall approval likelihood is significant. Lenders see you as a safer bet, often translating to lower interest rates and a higher chance of approval.

B. Building a Canadian Financial Footprint (Even a Small One) Before Applying

Even if you've just arrived in British Columbia, you can start building a Canadian financial footprint. Secured credit cards and small, manageable loans are essential stepping stones. A secured credit card requires a deposit, which acts as your credit limit, allowing you to demonstrate responsible credit usage without a prior credit history. Paying bills on time, even small ones, helps establish a positive credit score. The critical importance of a Canadian bank account for direct pension deposits cannot be overstated. It demonstrates financial stability within Canada and provides a clear, verifiable record of your income in Canadian dollars.

Timely payments on any credit product, no matter how small, contribute to your credit score. For example, if you get a small loan or secured credit card, ensure you always make payments on time. This proactive approach shows lenders that you are capable of managing Canadian credit responsibly. For more on building credit, consider our article Your Credit Score is NOT Your Rate. Get a Fair Loan, Toronto, which emphasizes that even with a developing credit profile, fair rates are attainable.

C. The Co-Signer Advantage: When and How to Leverage Support Effectively

If you have a trusted friend or family member who is a Canadian resident with a strong credit history, a co-signer can significantly boost your approval odds. A co-signer takes on full legal responsibility for the loan if you default, substantially reducing the lender's risk. However, it's crucial to understand the full responsibility and implications of a co-signer on a car loan, both for you and for them. This is a serious commitment that can impact their credit score if payments are missed. Choose a co-signer who understands these terms and is willing to support your financial journey.

D. Targeting the Right Vehicle: Balancing Needs, Affordability, and Lender Comfort

The type of vehicle you choose can also impact your loan approval. For newcomers with foreign pension income, starting with a more affordable and reliable vehicle can be a strategic move. New vs. Used: While a new car might seem appealing, a reliable used vehicle often presents lower entry costs and depreciation, making it a less risky proposition for lenders. Car brands often associated with easier financing or lower entry costs (e.g., Toyota, Honda, Hyundai, Mazda) are good choices due to their reputation for reliability, fuel efficiency, and strong resale value in British Columbia.

Pro Tip 4: For your first Canadian car, consider starting with a slightly less expensive, reliable used vehicle. This allows you to build credit history more quickly and upgrade to your dream car later.

A lower loan amount reduces risk for lenders and makes approvals easier. It also helps you focus on building that crucial Canadian credit score without undue financial stress.

V. Beyond the Approval: Navigating Loan Terms and Uncovering Hidden Costs

Getting approved is a victory, but understanding the terms of your loan is equally important. Many newcomers, eager to drive off the lot, overlook the fine print, potentially leading to higher long-term costs.

A. Deconstructing Your Loan Agreement: Interest Rates, APR, and Amortization Schedules

Your loan agreement is a legally binding document that outlines all the financial details. Pay close attention to:

- Interest Rates: This is the percentage charged on the principal amount of your loan.

- APR (Annual Percentage Rate): The APR includes the interest rate plus any additional fees, giving you a more accurate picture of the total annual cost of borrowing. It's the most comprehensive measure of your loan's cost.

- Variable vs. Fixed Rates: Fixed rates offer predictable monthly payments for the life of the loan, which can be highly suitable for those relying on a stable foreign pension. Variable rates can fluctuate with market conditions, potentially leading to unpredictable payments, which might be less ideal for managing a fixed income.

- Amortization Schedules: This details how your payments are applied to the principal and interest over the loan's term. Understanding the true total cost of borrowing over extended terms (e.g., up to 96 months, as seen with some competitor offerings like RBC) is paramount. Longer terms mean lower monthly payments but significantly more interest paid over the life of the loan.

Pro Tip 5: Never solely focus on the monthly payment. Always calculate the total amount you'll pay over the entire life of the loan, including interest, to understand the true cost.

A lower monthly payment spread over a longer term can hide a much higher overall cost. Use online loan calculators or ask your lender for a full amortization schedule.

B. The Fine Print: Fees, Penalties, and Mandatory Insurance Requirements

Loan agreements often contain various fees and penalties:

- Administrative Fees: Charges for processing your loan.

- Loan Origination Fees: Sometimes a percentage of the loan amount, charged for setting up the loan.

- Early Repayment Penalties: Some loans penalize you for paying off the loan sooner than scheduled. Ensure you understand if this applies, especially if you anticipate having extra funds later.

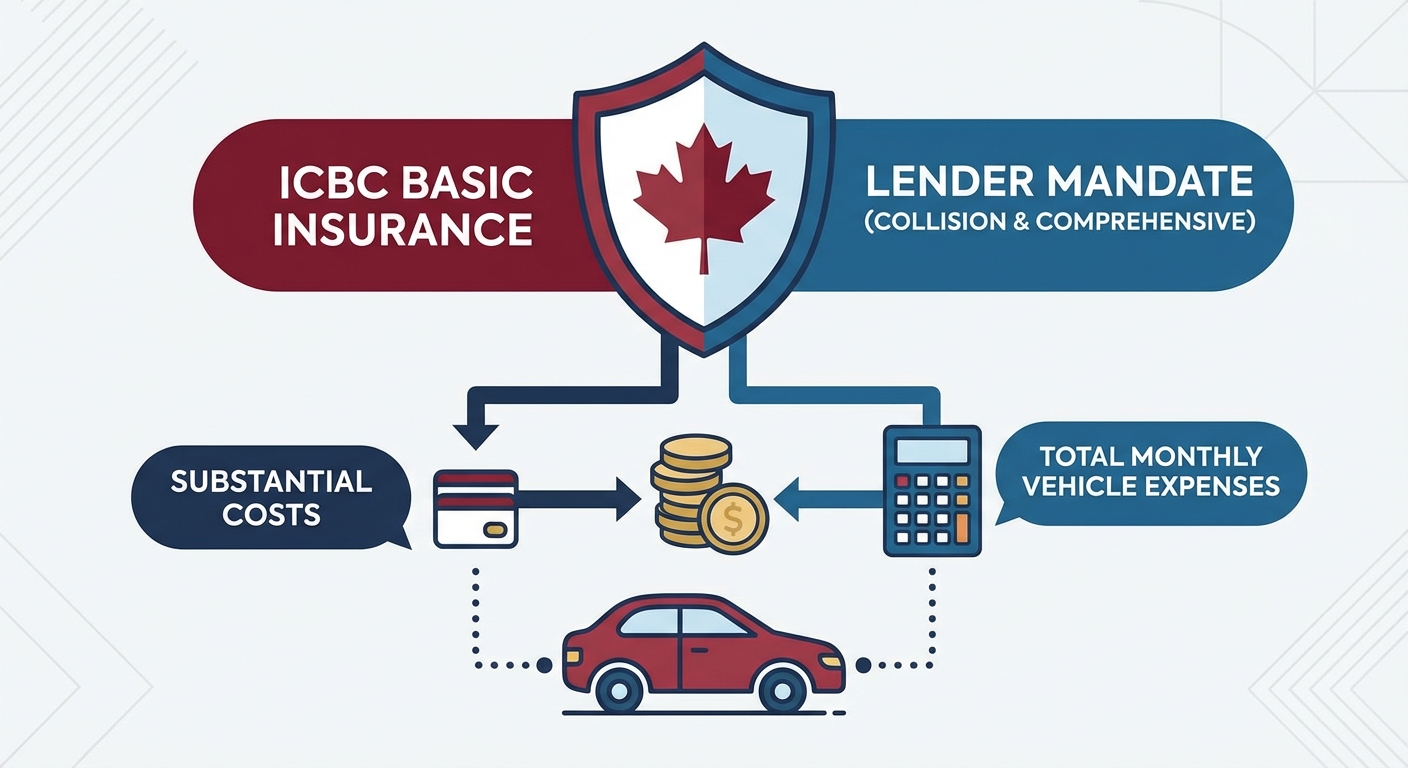

In British Columbia, mandatory insurance (collision, comprehensive) is a significant part of your overall vehicle budget. Unlike other provinces, British Columbia operates under a public auto insurance system managed by the Insurance Corporation of British Columbia (ICBC). You are legally required to purchase basic insurance from ICBC, and most lenders will also mandate additional collision and comprehensive coverage to protect their asset (the car). These costs can be substantial and must be factored into your total monthly vehicle expenses.

C.

VI. British Columbia Specifics: Driving Forward in the Golden Province

Beyond the loan itself, understanding the unique automotive landscape of British Columbia is crucial for any new car owner.

A. ICBC and Insurance Requirements: What You Need to Know as a Newcomer in British Columbia

As mentioned, British Columbia has a unique public auto insurance system. All basic vehicle insurance must be purchased through ICBC. As a newcomer, you'll need to understand how to register your vehicle and obtain appropriate insurance. Leveraging foreign driving history and claims records can potentially reduce premiums. ICBC often offers discounts for drivers with a proven record of safe driving from other countries, but you'll need official documentation (e.g., driving abstracts, claims history letters) from your previous insurer(s) and licensing authority, translated and certified if necessary.

B. Vehicle Registration and Licensing for Permanent Residents in British Columbia

Once you purchase a vehicle, you'll need to register it with ICBC and obtain British Columbia licence plates. If you have a driver's license from your home country, you may be able to use it for a limited time, but you will eventually need to obtain a British Columbia driver's license. This process typically involves knowledge and road tests, although some countries have reciprocal agreements that may simplify the process. Importing a vehicle vs. buying locally: While tempting to bring your car from abroad, importing a vehicle has significant regulations, inspections, and cost implications (duties, taxes, modifications for Canadian standards) that often make buying locally the more practical and economical choice.

C. City-Specific Considerations for Car Ownership and Financing in British Columbia

- Vancouver: Known for its high cost of living, car ownership in Vancouver presents challenges like expensive parking, significant traffic congestion, and a robust public transit system (TransLink) that might make car ownership less essential for some. However, having a car opens up the stunning natural beauty surrounding the city.

- Surrey/Richmond: These rapidly growing communities often have longer commutes and less comprehensive public transit coverage than central Vancouver, making personal vehicles a greater necessity. The presence of diverse financial institutions and dealerships caters to a wide range of needs.

- Victoria/Kelowna: In these regional centres, car ownership is often essential for daily life and exploring the beautiful surrounding areas. Local banks and credit unions might have a stronger presence and more personalized service, offering different commuting needs and lifestyle implications for car ownership.

D. Navigating Public Transportation vs. Car Ownership Costs in British Columbia's Major Hubs

Before committing to a car loan, especially in metropolitan areas like Vancouver, it's wise to conduct a cost-benefit analysis. Consider the monthly loan payment, insurance, fuel, maintenance, parking, and potential depreciation against the cost of TransLink passes or other regional transit systems. While public transit is efficient in some areas, a car provides unparalleled freedom and access to all that British Columbia has to offer, from the Okanagan Valley to the Rocky Mountains.

VII. Your Roadmap to Driving Off the Lot in British Columbia: Final Steps and Future Credit Building

The journey from foreign pension to Canadian car owner is a significant accomplishment. Here’s how to finalize your purchase and leverage it for future financial success.

A. From Loan Approval to Keys in Hand: The Final Checklist for New Car Owners

Once your loan is approved, there are a few critical final steps before you take possession of your new vehicle:

- Verifying all paperwork: Carefully review the bill of sale, loan agreement, and any extended warranty documents. Ensure all figures match what you agreed upon.

- Insurance: Confirm your ICBC insurance is active and covers the vehicle as required by law and your lender.

- Registration: Ensure the vehicle is properly registered in your name with ICBC.

- Understanding warranty and maintenance schedules: Know your vehicle’s warranty coverage and recommended maintenance plan to ensure its longevity and protect your investment.

B. Leveraging Your Car Loan for Future Financial Success in Canada

Timely and consistent payments on your car loan are a powerful tool for building a robust Canadian credit score. This is arguably one of the most significant long-term benefits of securing your first car loan in Canada. A strong credit history opens doors for larger financial goals down the line, such as mortgages for a home in Burnaby, business loans for an entrepreneurial venture in Richmond, or other significant credit opportunities. Your car loan, when managed responsibly, becomes a stepping stone to full financial integration and empowerment in Canada.

C. A Word of Encouragement: Your Foreign Pension is a Strength, Not a Weakness

It's easy to feel discouraged when your financial stability is initially misunderstood. But remember, your stable foreign income is a strength. It represents a lifetime of work, responsibility, and financial planning. By following the strategies outlined in this guide – meticulous preparation, targeting the right lenders, and understanding the nuances of the Canadian system – you can confidently navigate the process. At SkipCarDealer.com, we believe every permanent resident deserves the opportunity to thrive in British Columbia, and that includes the freedom and mobility a car provides. Embrace your financial story, present it well, and drive forward with confidence.