Toronto's Active R9? Your Car Loan Didn't Get the Memo.

Table of Contents

- Toronto's Active R9? Your Car Loan Didn't Get the Memo.

- Key Takeaways

- The Unignorable Truth: Securing a Car Loan with an Active R9 in Ontario

- The Elephant in the Room: What an 'Active R9' Actually Signifies for Your Credit in Ontario

- Setting the Stage for Success: Pre-Loan Preparation for R9 Borrowers in Ontario

- Your Financial Mirror: Unpacking Your Current Financial Situation

- The Down Payment Advantage: Why More Cash Upfront is Your Best Friend

- The Power of Co-Signers: A Strategic Ally for R9 Borrowers

- Navigating the Ontario Lender Labyrinth: Finding Your Path to Approval

- Traditional Banks vs. Subprime Specialists: Where to Focus Your Search

- Dealership Finance Departments: A Direct Route to Approval

- Online Auto Loan Platforms: Convenience and Connection for Ontario Drivers

- The Application Deep Dive: What Ontario Lenders *Really* Look For Beyond the R9

- Beyond the R9: The Other Factors That Matter to Ontario Lenders

- The Paperwork Playbook: Documents You'll Need to Assemble

- Understanding Interest Rates and Loan Terms for R9 Borrowers in Ontario

- The Vehicle Choice Conundrum: Smart Decisions for R9 Borrowers

- Beyond Approval: Managing Your Loan and Rebuilding Your Credit with an R9

- Making Every Payment Count: The Foundation of Credit Rehabilitation

- The Credit Score Comeback: How a Car Loan Can Transform Your R9

- Strategic Refinancing: A Future Opportunity for Lower Rates

- Real-World Scenarios and Ontario City Spotlights for R9 Car Loans

- Toronto's Urban Challenge: Navigating higher costs of living and specific lender options in the Greater Toronto Area.

- Ottawa's Public Sector Advantage: How stable government employment can be a significant positive factor for R9 borrowers.

- Mississauga & Hamilton's Diverse Markets: Exploring local dealership and lender nuances in rapidly growing regions.

- Rural Ontario Considerations: Different vehicle needs and accessibility to specialized lenders outside major urban centres.

- Your Next Steps to Approval: A Clear Path Forward for Ontario Drivers with an R9

- A Concise Action Plan

- Empowerment Message: You *Can* Get a Car Loan, But It Requires Strategy and Discipline.

- Your Burning Questions Answered: FAQ for R9 Car Loans in Ontario

- Common Inquiries from Ontario Drivers with an R9

Toronto's Active R9? Your Car Loan Didn't Get the Memo.

In the vibrant, fast-paced landscape of Ontario, from the bustling streets of Toronto to the serene shores of Lake Superior, a car isn't just a convenience – it's often a necessity. It gets you to work, connects you with family, and opens up opportunities. But what happens when your credit report flashes an "R9"? This ominous rating, indicating a debt written off or sent to collections, can feel like a roadblock to your automotive dreams. Many assume an R9 means an automatic "no" from lenders. However, at SkipCarDealer.com, we understand that life happens, and a past financial misstep shouldn't permanently sideline your future. Getting a car loan with an active R9 in Ontario isn't easy, but it's far from impossible. It requires strategy, preparation, and knowing where to look. Let's navigate this journey together.

Key Takeaways

- An active R9 rating doesn't mean 'no' to a car loan, but it means 'strategize and prepare diligently.'

- Your best allies are specialized subprime lenders and dealership finance departments, not traditional banks.

- A significant down payment and a reliable co-signer dramatically improve your approval odds.

- Be prepared for higher interest rates, but focus on the total cost and the opportunity to rebuild credit.

- Consistent, on-time payments on your new car loan are your most powerful tool for credit rehabilitation in Ontario.

The Unignorable Truth: Securing a Car Loan with an Active R9 in Ontario

The Elephant in the Room: What an 'Active R9' Actually Signifies for Your Credit in Ontario

Let's be blunt: an R9 credit rating is a serious red flag for lenders across Canada. It means that an account – whether it was a credit card, a line of credit, or a personal loan – was so severely delinquent that the lender either wrote it off as uncollectible or sent it to a collections agency. This isn't just a missed payment; it signifies a significant breakdown in your financial commitment to a creditor.

Beyond the Basics: A Deep Dive into the R9 Credit Rating and Its Impact on Lending in Ontario. When a lender sees an R9, they don't just see a number; they see a history of non-payment, which translates directly into high risk. This risk assessment is central to the Canadian financial system. Lenders are in the business of lending money they expect to get back, with interest. An R9 tells them there's a higher probability that you might not repay, or at least, not on time.

The Domino Effect: How an R9 on one account can affect your entire credit profile and future borrowing capacity. One R9 can indeed cast a long shadow. It significantly lowers your credit score, making it difficult to qualify for new credit cards, mortgages, and, yes, car loans. It also signals to other potential lenders that you might be a high-risk borrower, leading to stricter terms, higher interest rates, or outright denials.

For those who have navigated severe financial challenges like a Consumer Proposal, it's worth noting that even these situations don't necessarily close the door on future financing. For more on this, check out our guide on Your Consumer Proposal? We Don't Judge Your Drive.

Pro Tip: Understanding your credit report beyond just the R9 is crucial. Order full reports from Equifax Canada and TransUnion Canada before applying anywhere. Dispute any inaccuracies immediately. Knowing precisely what's on your report allows you to address it directly and present a clearer picture to potential lenders.

Setting the Stage for Success: Pre-Loan Preparation for R9 Borrowers in Ontario

Your Financial Mirror: Unpacking Your Current Financial Situation

Before you even think about stepping onto a dealership lot or filling out an online application, you need to take a brutally honest look at your finances. This isn't just about what you *want* to pay; it's about what you can *realistically* afford.

- Budgeting Bootcamp: Identifying Realistic Disposable Income for Car Payments in Ontario – examples from Toronto, Ottawa, and smaller cities. Start by listing all your income sources and every single expense – rent, groceries, utilities, existing loan payments, entertainment, even that daily coffee. In Toronto, where the cost of living is notoriously high, a realistic budget might mean cutting back on discretionary spending more aggressively than in, say, Kingston or Thunder Bay. For someone in Ottawa with stable government employment, their disposable income might be more predictable, allowing for a higher payment threshold. Your goal is to identify a clear, consistent amount you can commit to a car payment each month without straining your finances.

- Addressing Outstanding Debts: Prioritizing Your Financial Health Before Applying – strategies for managing current collections or overdue accounts. If you have active collection accounts, addressing them – even by setting up payment plans – can show lenders you're taking responsibility. While an R9 remains, demonstrating proactive debt management can make a difference.

- Understanding Your Debt-to-Income Ratio: Why it matters even more with an R9. Your Debt-to-Income (DTI) ratio is the percentage of your gross monthly income that goes towards debt payments. Lenders use this to assess your ability to take on more debt. With an R9, a high DTI is a major deterrent. Aim for a DTI below 40%, ideally even lower, especially if your credit is already compromised.

Pro Tip: Create a detailed monthly budget, accounting for all income and expenses. Be ruthlessly honest about what you can truly afford, factoring in insurance, fuel, and maintenance. Use a spreadsheet or a budgeting app to track every dollar for at least two months to get an accurate picture.

The Down Payment Advantage: Why More Cash Upfront is Your Best Friend

For R9 borrowers in Ontario, a significant down payment isn't just helpful; it's often critical.

- Reducing Lender Risk: How a Significant Down Payment Improves Your Odds of Approval and potentially lowers your interest rate. When you put down a substantial amount of your own money, you immediately reduce the lender's risk. They're financing less of the vehicle's value, meaning they have less to lose if you default. This reduced risk can translate directly into a higher likelihood of approval and, in some cases, a slightly lower interest rate, which can save you thousands over the life of the loan.

- Calculating a Realistic Down Payment Goal for Ontario Car Buyers: Strategies for saving or sourcing funds. Aim for at least 10-20% of the vehicle's purchase price. For a $15,000 used car, that's $1,500 to $3,000. Strategies include saving diligently, selling unused items, or utilizing a tax refund (which we'll discuss later).

- The Psychological Impact: Demonstrating Commitment to Lenders. Beyond the financial reduction of risk, a down payment shows a lender that you are personally invested in the purchase and committed to the loan. It signals responsibility and a serious intent to repay.

While a significant down payment is highly recommended for R9 borrowers, some lenders and programs do exist that cater to different financial situations. If you're exploring options where a down payment might be less critical, you might find our article on Your Ink Is Dry. Your New Car Needs No Down Payment, Ontario insightful, though it's important to remember an R9 changes the landscape.

The Power of Co-Signers: A Strategic Ally for R9 Borrowers

If a strong down payment isn't enough, or if you want to further bolster your application, a co-signer can be a game-changer.

- Who Makes a Good Co-Signer? Understanding the Responsibilities and Risks for both parties in Ontario. A good co-signer is someone with excellent credit, stable income, and a willingness to take on the legal responsibility for your loan. In Ontario, a co-signer is equally liable for the debt. If you miss payments, their credit will suffer, and they will be pursued for repayment. This is a serious commitment, not to be taken lightly by either party.

- Navigating the Co-Signer Conversation: Tips for Approaching Friends or Family with a Clear Plan. Be transparent and honest about your R9 rating and your commitment to rebuilding credit. Present your detailed budget and explain your plan for consistent, on-time payments. Emphasize that you view this as an opportunity to prove your financial responsibility.

- Legal Implications: What a Co-Signer Agreement Entails in Ontario. Ensure your co-signer fully understands the legal contract. They are not just vouching for you; they are signing a legally binding agreement to repay the loan if you cannot.

Navigating the Ontario Lender Labyrinth: Finding Your Path to Approval

Traditional Banks vs. Subprime Specialists: Where to Focus Your Search

This is where R9 borrowers need to manage expectations and direct their efforts wisely.

- The Reality of Major Banks (RBC, TD, CIBC, Scotiabank, BMO) for R9 Borrowers: Managing Expectations and understanding their stricter lending criteria. Let's be frank: securing a car loan from a major Canadian bank with an active R9 rating is highly unlikely. These institutions typically have very strict lending criteria and prefer borrowers with good to excellent credit scores. While it's not impossible, their risk models are generally not designed to accommodate severe credit challenges like an R9. You might find a warmer reception if you have a long-standing, positive relationship with your bank, but even then, it's an uphill battle.

- Specialized Bad Credit Lenders in Ontario: Understanding Their Business Model and How They Can Help those with an R9 credit rating. This is your primary target. Specialized subprime lenders (also known as bad credit lenders) are in the business of lending to individuals with less-than-perfect credit, including those with R9 ratings, bankruptcies, or consumer proposals. They understand that people make mistakes and deserve a second chance. Their business model accounts for higher risk by charging higher interest rates, but they are far more willing to approve loans based on your current ability to pay, employment stability, and other mitigating factors rather than solely your credit score.

- Credit Unions in Ontario: A Potential, Though Less Likely, Avenue – exploring local options in places like Hamilton or Kingston. Credit unions, being member-owned, sometimes offer more flexible lending criteria than major banks. If you have a long-standing relationship with a local credit union in Ontario, like Meridian Credit Union or Alterna Savings, it might be worth exploring. They might be more willing to consider your personal story and current financial situation, even with an R9, especially if you have other accounts in good standing with them. However, their rates for high-risk loans might still be competitive with specialized subprime lenders.

Pro Tip: Research lenders specifically advertising 'bad credit car loans' or 'R9 auto financing' in Ontario. These are designed to handle higher-risk profiles and are your most likely avenue for approval. Don't waste time applying to traditional banks if you have an R9, as multiple rejections can further negatively impact your credit score.

Dealership Finance Departments: A Direct Route to Approval

Many dealerships, particularly larger ones, have robust finance departments that act as intermediaries, connecting you with a network of lenders.

- The 'Buy Here, Pay Here' Model: Pros, Cons, and What to Watch Out For in Ontario, particularly in urban centres like Mississauga. Some dealerships operate on a "buy here, pay here" model, meaning they finance the loan themselves, often targeting customers with poor credit. The main pro is easier approval. However, cons often include very high interest rates, limited vehicle selection (often older, higher-mileage cars), and potentially less favourable terms. In urban centres like Mississauga, you might find more of these options, but exercise extreme caution, scrutinize contracts, and understand all fees before committing.

- Leveraging Dealership Networks: How they connect you with a multitude of subprime lenders who specialize in challenging credit situations. Most reputable dealerships don't just work with one or two banks. They have relationships with a wide array of lenders, including those specialized in subprime auto loans. Their finance managers are experts at matching borrowers with the right lender and structuring deals that get approved, even with an R9. They can often "shop" your application to several lenders at once, increasing your chances of finding an approval.

- The Value of a Dedicated Finance Manager: Their role in advocating for your loan. A good finance manager understands the nuances of bad credit financing. They know what information to highlight, how to present your application, and which lenders are most likely to approve someone with an R9 based on your specific circumstances.

Pro Tip: Don't limit yourself to one dealership. Shop around and compare offers, even with an R9. Different dealerships work with different lenders and may have varying success rates for challenging credit situations.

Online Auto Loan Platforms: Convenience and Connection for Ontario Drivers

The digital age has brought new avenues for securing financing, even for those with credit challenges.

- How Online Services Streamline the Application Process for High-Risk Borrowers across Ontario. Online auto loan platforms – like SkipCarDealer.com – offer a streamlined application process that can be completed from the comfort of your home, whether you're in Timmins or Windsor. These platforms often specialize in connecting applicants with a network of lenders, including subprime specialists, who are more willing to approve those with an R9. They can quickly pre-approve you, giving you an idea of what you qualify for before you even step foot in a dealership.

- Vetting Online Lenders: Ensuring Legitimacy and Avoiding Scams in the digital age. While convenient, the online space also requires vigilance. Always ensure any online platform or lender you engage with is legitimate and reputable. Look for clear privacy policies, secure websites (HTTPS), and positive customer reviews. Avoid any lender that guarantees approval without checking your information or asks for upfront fees.

- The Speed Advantage: Getting pre-approved quickly to understand your options. One of the biggest benefits of online platforms is speed. You can often get pre-approved within minutes or hours, allowing you to understand your budget and terms before you start car shopping. This pre-approval gives you leverage at the dealership and helps you avoid looking at vehicles outside your financial reach.

The Application Deep Dive: What Ontario Lenders *Really* Look For Beyond the R9

Beyond the R9: The Other Factors That Matter to Ontario Lenders

While an R9 is a significant hurdle, it's not the only factor lenders consider. They look at your overall financial picture.

- Income Stability: Demonstrating Your Ability to Pay – the importance of consistent employment or verifiable income sources. This is paramount. Lenders want to see that you have a steady, reliable source of income that can cover your monthly car payments. This could be consistent employment, verifiable self-employment income, or even certain government benefits.

- Employment History: Consistency as a Key Indicator of Reliability – how long you've been at your current job. Lenders prefer to see a stable employment history, ideally at least 1-2 years with your current employer. Frequent job changes can be seen as instability, adding another layer of risk.

- Residency and Identity Verification: Standard Requirements for all Ontario Loans. You'll need to prove you're an Ontario resident and provide valid identification. This is standard procedure for any loan application.

- The 'Human Factor': Some lenders may consider your personal story and circumstances, especially if you can explain past financial difficulties. While less common with automated systems, some specialized lenders or finance managers will listen to your story. If you can clearly explain the circumstances that led to the R9 (e.g., job loss, medical emergency) and demonstrate how your situation has improved, it can sometimes sway a decision in your favour.

The Paperwork Playbook: Documents You'll Need to Assemble

Being prepared with the right documents can significantly speed up the approval process.

- Proof of Income: Recent Pay Stubs, Employment Letters, or Tax Returns (Notice of Assessment). Typically, 2-3 recent pay stubs are required. If self-employed, your Notice of Assessment from the Canada Revenue Agency (CRA) for the last 1-2 years will be crucial.

- Proof of Residency: Utility Bills, Lease Agreements, or Mortgage Statements. Documents showing your current address and that you've been at that address for a reasonable period (e.g., 6-12 months) are often requested.

- Banking Information: Recent Bank Statements and Direct Deposit Details. Lenders want to see consistent income deposits and responsible management of your bank account.

- Personal Identification: Valid Ontario Driver's License or other government-issued ID. This is a non-negotiable requirement.

Understanding Interest Rates and Loan Terms for R9 Borrowers in Ontario

This is where the reality of an R9 credit rating becomes most apparent: higher costs.

- The Reality of Higher Rates: Why R9 Loans Come with Increased Costs due to perceived risk. With an R9, you are considered a high-risk borrower. Lenders compensate for this risk by charging significantly higher interest rates than they would for someone with good credit. While it might feel punitive, it's how subprime lending works.

- Calculating Total Cost: Beyond the Monthly Payment – Understanding Amortization, Fees, and the true expense over the loan term. Don't just look at the monthly payment. A lower monthly payment often means a longer loan term, which drastically increases the total interest paid. Factor in any administrative fees, processing charges, or other add-ons that can inflate the total cost.

- Negotiating Terms: What little leverage you might have, and when to walk away. With an R9, your negotiation leverage is limited. Your best bet is to compare offers from multiple lenders. If a deal feels predatory (e.g., excessively long terms, rates well above the typical subprime range, or hidden fees), be prepared to walk away and continue your search.

Pro Tip: Focus on the total cost of the loan over its lifetime, not just the monthly payment. Shorter terms, if affordable, can save you thousands in interest, even with a high rate. Use an online loan calculator to compare different term lengths and their impact on total interest paid.

Here's a general idea of interest rates for different credit profiles in Ontario:

| Credit Profile | Typical Interest Rate Range (Ontario) | Considerations for R9 Borrowers |

|---|---|---|

| Excellent (760+) | 4.99% - 8.99% | Not applicable for R9; rates are significantly lower. |

| Good (660-759) | 9.99% - 14.99% | Not applicable for R9; rates are considerably higher. |

| Fair (560-659) | 15.99% - 19.99% | Closer to this range for some bad credit, but R9 typically higher. |

| Poor/Bad (300-559 with R9) | 19.99% - 29.99% (or higher) | This is the realistic range for R9 borrowers. Focus on total cost. |

The Vehicle Choice Conundrum: Smart Decisions for R9 Borrowers

Your choice of vehicle plays a crucial role in securing approval and managing your finances.

- Used vs. New: Why a Reliable Used Car is Often the Wiser Choice, offering lower price points and less depreciation. With an R9, a new car loan is a significant challenge. Lenders are more comfortable financing reliable used vehicles, which have lower price tags and depreciate less rapidly. This reduces the loan amount, making it easier to qualify and keep payments manageable.

- Affordable Models: Prioritizing Functionality Over Flash – focusing on vehicles that meet your needs without overextending your budget. Forget the luxury SUV for now. Focus on dependable, fuel-efficient models that will get you from point A to point B. Think Honda Civic, Toyota Corolla, or a similar compact SUV – vehicles known for their longevity and lower maintenance costs.

- Avoiding Predatory Practices: Spotting Red Flags in Toronto, Hamilton, and other Ontario cities – watch out for extremely long loan terms or excessive add-ons. Be wary of dealerships pushing you into a vehicle far beyond your means, or extending loan terms to 8 or 9 years to lower monthly payments. While the monthly payment looks appealing, you'll pay exorbitant amounts in interest and likely be underwater on the loan for years. Also, scrutinize any extended warranties, rustproofing, or other add-ons; they can significantly inflate your loan.

Beyond Approval: Managing Your Loan and Rebuilding Your Credit with an R9

Making Every Payment Count: The Foundation of Credit Rehabilitation

Once you've secured that loan, the real work – and opportunity – begins.

- Setting Up Automatic Payments: Eliminating the Risk of Missed Deadlines and ensuring punctuality. This is your single most important step. Automating your payments directly from your bank account ensures you never miss a due date. This builds a perfect payment history, which is the most impactful factor in improving your credit score.

- Understanding Your Loan Agreement: Key Clauses, Penalties for Missed Payments, and Your Responsibilities as a Borrower. Read your loan agreement carefully. Know your payment schedule, any late fees, and what constitutes a default. Understanding your obligations helps you avoid costly mistakes.

- The Power of Early Payments: How even small extra payments can reduce interest and shorten your loan term. If you can afford it, even an extra $20-$50 on your principal each month can make a significant difference over the loan term, reducing the total interest paid and shortening the duration of the loan.

Pro Tip: Treat your car loan as a primary tool for credit rebuilding. Consistent, on-time payments are paramount and will be reported to credit bureaus, positively impacting your score. This isn't just about owning a car; it's about proving your financial reliability for future opportunities.

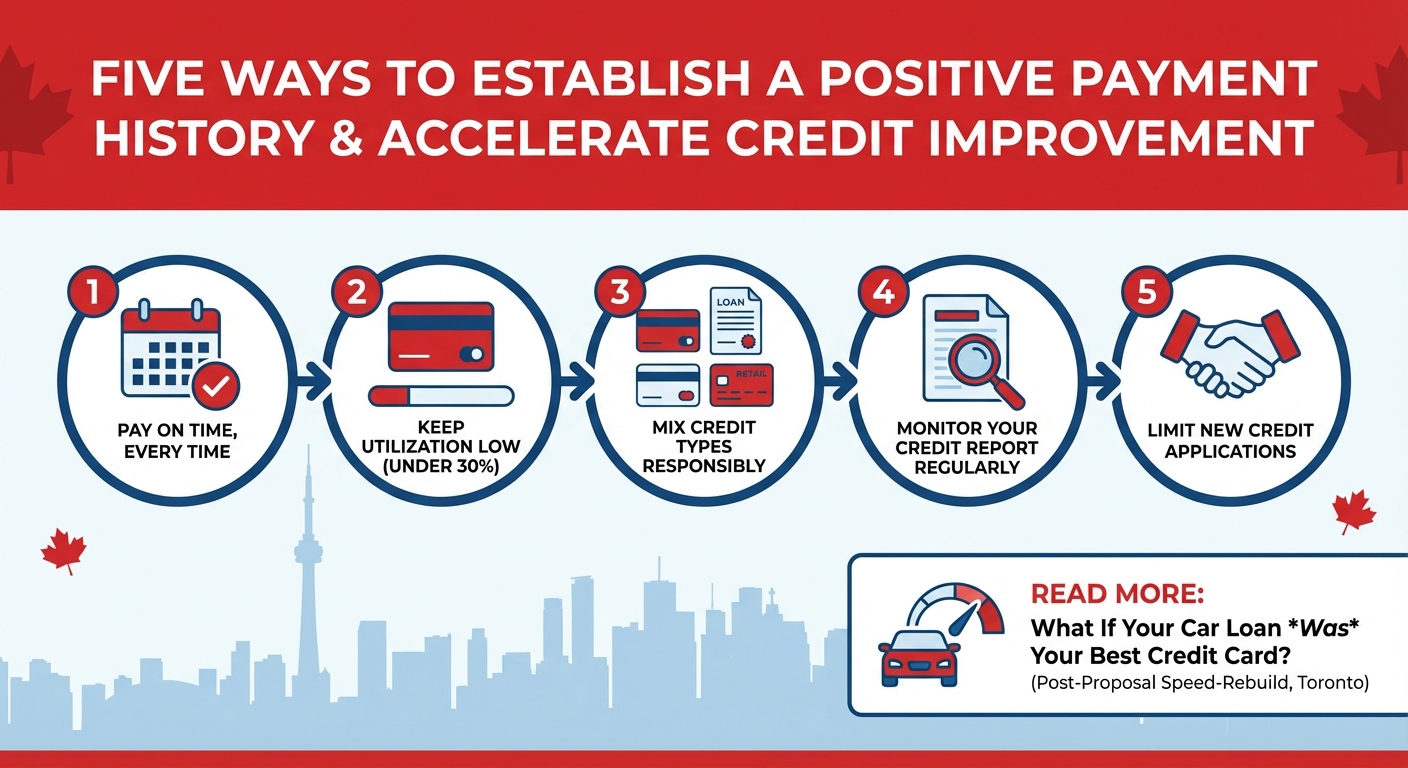

The Credit Score Comeback: How a Car Loan Can Transform Your R9

This is the silver lining of getting a car loan with an R9 – it's a direct path to credit rehabilitation.

- The Mechanics of Credit Improvement: Payment History, Credit Utilization, and Credit Mix – how your new loan contributes. Each on-time payment you make is a positive entry on your credit report. Over time, this consistent positive payment history will overshadow the negative R9. A new installment loan also diversifies your credit mix, which can further boost your score. Your credit utilization for this specific loan will also be managed as you pay it down.

- Monitoring Your Progress: Regularly Checking Your Credit Report and Score to see the positive changes. Continue to monitor your credit reports from Equifax Canada and TransUnion Canada every few months. You'll start to see your score gradually increase and the positive payment history build.

- What to Expect: A realistic timeline for seeing significant improvements in your credit rating. Credit rebuilding is a marathon, not a sprint. While you'll see small improvements relatively quickly (within 6-12 months), significant improvements that move you out of the "poor credit" category typically take 18-36 months of consistent, on-time payments.

Think of your new car loan as a powerful tool in your credit rebuilding arsenal. In fact, for many, a car loan can be one of the most effective ways to establish a positive payment history and accelerate credit improvement. For more on how a car loan can act as a catalyst for credit recovery, read What If Your Car Loan *Was* Your Best Credit Card? (Post-Proposal Speed-Rebuild, Toronto).

Strategic Refinancing: A Future Opportunity for Lower Rates

Once your credit improves, you won't be stuck with that high R9 interest rate forever.

- When to Consider Refinancing: After 12-24 Months of Perfect Payments and a demonstrated improvement in your credit score. Once you've established a solid track record of 1-2 years of on-time payments and seen your credit score improve significantly, it's time to consider refinancing.

- The Benefits of Refinancing for R9 Borrowers Who've Improved Their Credit: Lower interest rates, reduced monthly payments, and more favourable terms. Refinancing allows you to replace your existing high-interest loan with a new one at a much lower interest rate. This can drastically reduce your monthly payments, save you thousands in interest over the remaining term, and free up disposable income.

- The Refinancing Process: How it works and what documents you'll need. The process is similar to your initial loan application, but this time you'll have a stronger credit profile. You'll need proof of income, ID, and your current loan details.

Real-World Scenarios and Ontario City Spotlights for R9 Car Loans

Toronto's Urban Challenge: Navigating higher costs of living and specific lender options in the Greater Toronto Area.

- Public transit considerations vs. car necessity. In Toronto, while the TTC (Toronto Transit Commission) is extensive, many residents still require a car for work commutes (especially if outside the core), family obligations, or simply to escape the city on weekends. The necessity often outweighs the high cost of car ownership, including insurance and parking.

- Specific dealerships known for bad credit financing in the GTA. The Greater Toronto Area is vast and competitive. Many large dealership groups have dedicated subprime finance departments – look for those advertising "bad credit auto loans" or "second chance financing" in areas like North York, Scarborough, or Brampton.

Ottawa's Public Sector Advantage: How stable government employment can be a significant positive factor for R9 borrowers.

- Lenders' perception of federal/provincial employee stability. In Ottawa, the high concentration of federal and provincial government employees offers a unique advantage. Lenders often view government employment as highly stable, with consistent income and strong benefits. This stability can significantly offset the risk associated with an R9, making approval more likely and potentially leading to slightly better terms than for someone with less stable employment.

- Local resources for credit counselling. Ottawa also has several non-profit credit counselling services that can help residents manage debt and improve financial literacy, which can indirectly aid in securing a car loan.

Mississauga & Hamilton's Diverse Markets: Exploring local dealership and lender nuances in rapidly growing regions.

- Access to a wider range of vehicle types and price points. As rapidly growing cities, Mississauga and Hamilton boast diverse populations and economies. This translates into a wide array of dealerships offering vehicles at various price points, from budget-friendly used cars to newer models. This diversity can be beneficial for R9 borrowers, providing more options to fit their specific budget and needs.

- Community-specific financial advice centres. Both cities also have local financial literacy and debt counselling services that can provide tailored advice and support.

Rural Ontario Considerations: Different vehicle needs and accessibility to specialized lenders outside major urban centres.

- The necessity of a vehicle for daily life and work. In rural Ontario – from the agricultural communities of Southwestern Ontario to the resource-rich regions of Northern Ontario – a vehicle is almost always a non-negotiable necessity. Public transit is often non-existent, making a car essential for commuting, groceries, and medical appointments.

- Challenges and opportunities for securing financing in less populated areas. While there might be fewer physical dealerships and lenders in smaller towns, online platforms and larger regional dealerships (often located in the nearest city like London, Sudbury, or North Bay) can still serve rural residents effectively. The key is to be prepared to travel slightly further for the right deal or leverage online tools.

Your Next Steps to Approval: A Clear Path Forward for Ontario Drivers with an R9

A Concise Action Plan

- Assess & Budget: Get your credit reports from Equifax Canada and TransUnion Canada, create a detailed budget, and determine an affordable monthly payment that includes insurance, fuel, and maintenance.

- Save & Secure: Work towards a significant down payment (aim for 10-20%) and consider approaching a reliable co-signer with excellent credit.

- Target & Apply: Focus your efforts on specialized bad credit lenders and dealership finance departments in Ontario. Avoid traditional banks. Leverage online platforms like SkipCarDealer.com to streamline your search.

- Review & Compare: Scrutinize all loan terms, focusing on the total cost of the loan over its lifetime, not just the monthly payments. Don't be afraid to walk away from predatory offers.

- Commit & Rebuild: Once approved, set up automatic payments and make every single payment on time to transform your R9 rating and rebuild your financial future.

Empowerment Message: You *Can* Get a Car Loan, But It Requires Strategy and Discipline.

An R9 is a challenge, not an insurmountable barrier. It's a snapshot of your past, not a definitive statement about your future. With the right approach, diligent preparation, and a commitment to financial discipline, you can secure the vehicle you need in Ontario and embark on a journey to improved financial health. At SkipCarDealer.com, we believe everyone deserves a second chance to drive forward.