Pay Stub? Nah. Your DoorDash Deposits Just Bought a Car, Ontario.

Table of Contents

- Key Takeaways

- The Gig Economy Revolution: Driving Your Dreams on Your Own Terms

- Navigating the New Normal: The Rise of Self-Employed Income

- Your Financial Footprint: How Bank Statements Tell Your Story

- Deconstructing the 'Bank Statements Only' Car Loan for DoorDash Drivers in Canada

- Pro Tip: Your Banking Habits are Your Best Reference – Consistency and Responsibility Matter Most.

- The Anatomy of a Gig Worker's Bank Statement

- Income Fluctuations: How Lenders Assess Variability

- Navigating the Lender Landscape: Who's Ready to Fund Your Ride in Canada?

- Pro Tip: Don't Settle for the First Offer – Comparison Shopping Across Different Lender Types is Crucial for Better Rates and Terms.

- Traditional Banks: The Conservative Approach

- Dealership Financing: Convenience and Specialization

- Online Lenders and Brokers: The Gig Economy's Best Bet?

- Beyond the Deposits: Strengthening Your Car Loan Application

- Credit Score Mastery for Gig Workers

- Optimizing Your Financial Picture

- Choosing the Right Ride for Your Business

- The Fine Print & Hidden Costs: What Every DoorDash Driver Must Know

- Pro Tip: Always Request a Full, Itemized Breakdown of All Costs, Fees, and the Total Amount Payable Before Signing Any Agreement.

- Demystifying Interest Rates

- Beyond the Monthly Payment: True Cost of Ownership

- Your Step-by-Step Blueprint to Car Loan Approval in Canada

- Phase 1: Preparation – Gathering Your Bank Statements, Identification, and Other Essential Documents

- Phase 2: Application – Filling Out the Forms Accurately, Being Honest, and Highlighting Your Financial Strengths

- Phase 3: Negotiation – Empowering Yourself to Secure the Best Possible Rates and Terms

- Phase 4: Finalizing the Deal – What to Double-Check Before You Sign on the Dotted Line

- Real-World Success Stories: DoorDash Drivers Who Drove Away Happy

- Case Study 1: 'Maria from Calgary: From Bike to Brand New Sedan – A Story of Consistent Deposits and Smart Saving.'

- Case Study 2: 'Jean-Pierre from Montreal: Building Credit and a Business with His Delivery Car, Even with Past Challenges.'

- Case Study 3: 'Sarah from Halifax: The Power of Proactive Communication and an Organized Application, Securing a Loan in the Maritimes.'

- Lessons from the Road: Common Threads in Successful Applications

- Maintaining Momentum: Post-Approval Financial Wisdom for DoorDashers

- Pro Tip: Automate Your Payments and Set Reminders to Avoid Missed Deadlines, Protecting Your Credit Score and Loan Terms.

- Smart Financial Habits for Car Owners

- The Path to Financial Growth

- Your Road Ahead: Solidifying Your Financial Future on Four Wheels

- Frequently Asked Questions (FAQ)

Key Takeaways

- Bank Statements are Your New Pay Stub: For DoorDash drivers and other gig workers in Canada, 6-12 months of bank statements are increasingly accepted as proof of stable income, replacing traditional pay stubs and T4s.

- Consistency is Key: Lenders prioritize consistent deposits, even if fluctuating, over sheer volume. Demonstrating responsible financial habits through your banking history is crucial.

- Diverse Lender Landscape: While traditional banks might be conservative, dealership financing and specialized online lenders are often more flexible and experienced in approving car loans for self-employed individuals across provinces like Ontario, British Columbia, and Quebec.

- Strengthen Your Application: Beyond income, factors like a healthy credit score, a manageable debt-to-income ratio, and a down payment significantly boost your approval odds and can lead to better interest rates.

- Understand the Full Cost: Always scrutinize interest rates, loan terms, fees, and insurance requirements (including commercial considerations for gig work) to understand the true cost of your car loan.

The Gig Economy Revolution: Driving Your Dreams on Your Own Terms

The traditional 9-to-5 job is no longer the sole path to financial stability, nor is it the only way to secure a car loan in Canada. Across Ontario, from the bustling streets of Toronto to the quiet towns of Northern Ontario, and stretching across the country to Vancouver, Calgary, and Montreal, a new workforce has emerged: the gig economy. Millions of Canadians are embracing the flexibility and autonomy of platforms like DoorDash, Uber Eats, SkipTheDishes, and various freelance ventures. While this shift offers incredible freedom, it also presents unique challenges, particularly when it comes to proving income for significant purchases like a vehicle.

For decades, a car loan application hinged on a steady pay stub and a T4 slip from a long-term employer. But what if your income comes in dozens of small deposits, fluctuates week-to-week, and doesn't generate a traditional pay stub? This is the new reality for DoorDash drivers and other independent contractors. Thankfully, the financial landscape is evolving. Lenders are increasingly recognizing the validity and stability of gig economy income, understanding that a consistent stream of DoorDash deposits can be just as reliable, if not more so, than a single, fixed salary.

The solution? Your bank statements. In the absence of traditional employment documents, your bank account becomes a transparent, verifiable record of your financial activity. It tells the story of your earnings, your spending habits, and your overall financial health. For gig workers in Canada, bank statements are fast becoming the new gold standard for proving income, opening doors to car ownership that were once firmly shut.

Navigating the New Normal: The Rise of Self-Employed Income

The Canadian economy has seen a significant shift towards independent contracting and self-employment. Many individuals, especially in provinces like British Columbia and Quebec, are opting for the flexibility of setting their own hours and being their own boss. This transition, while empowering, often puts gig workers at a disadvantage with conventional lenders. Traditional financial institutions are built around the predictability of salaried or hourly employment, where income is typically stable and easily documented with bi-weekly pay stubs or annual T4s.

For a DoorDash driver, income can vary based on demand, personal availability, and even the time of year. One week might be incredibly lucrative, while another might be slower. This variability, combined with the lack of a "employer" in the traditional sense, means that standard loan application processes often fail to accurately assess a gig worker's true financial capacity. Lenders accustomed to seeing consistent, branded pay stubs often don't know how to interpret a series of deposits from "DoorDash Canada" or "SkipTheDishes Inc." This is where the need for a new approach becomes critical.

Your Financial Footprint: How Bank Statements Tell Your Story

In this new financial paradigm, your bank statements are not just a record of transactions; they are a comprehensive narrative of your income and expenses. For lenders who understand the gig economy, these statements offer a powerful and verifiable record of your earnings. They provide a transparent view of how much money flows into your account, how often, and how it's managed. This is crucial for assessing your ability to make regular car loan payments.

What specific details do lenders look for in your transaction history? They're not just glancing at the final balance. They're meticulously examining:

- Consistent Deposits: Are there regular deposits from DoorDash or other gig platforms? Even if the amounts vary, a consistent pattern of incoming funds signals reliability.

- Average Deposit Amounts: What's the typical range of your earnings? This helps them project your average monthly income.

- Spending Habits: While income is key, lenders also assess your outgoing transactions. They look for responsible spending, a healthy balance between income and expenses, and a clear ability to manage your money.

- Account Activity: A frequently used, active account with a healthy average daily balance indicates financial engagement and stability.

- Lack of Overdrafts or NSF Fees: Frequent overdrafts or non-sufficient funds (NSF) charges can be red flags, suggesting poor financial management.

By providing a clear, detailed history, your bank statements allow lenders to piece together a realistic picture of your income and financial responsibility, even without a traditional pay stub.

Deconstructing the 'Bank Statements Only' Car Loan for DoorDash Drivers in Canada

The concept of a 'bank statements only' car loan might sound too good to be true for many DoorDash drivers in Canada. But it's a legitimate and increasingly common financing option. It's not about ignoring income verification; it's about shifting the focus from outdated documentation to a more relevant and accurate representation of your financial reality.

What lenders *really* look for has evolved. Instead of a uniform pay stub, they're seeking evidence of consistent cash flow. Your DoorDash deposits, whether daily, weekly, or bi-weekly, are proof of earning potential. The power of your deposits lies in their cumulative effect. While individual deposits might seem small, over several months, they paint a clear picture of reliable, ongoing income. Lenders understand that the nature of gig work means income might be irregular in its exact timing or amount, but a sustained pattern of deposits indicates a dependable income stream.

Dispelling myths is important here. A 'bank statements only' loan is *not* a 'no income verification' loan. You are still verifying your income; you're just doing so through a different, albeit equally robust, method. Lenders will still scrutinize your financial history, but they're doing it through the lens of your bank activity rather than a corporate payroll report.

Pro Tip: Your Banking Habits are Your Best Reference – Consistency and Responsibility Matter Most.

To maximize your chances of approval, aim for consistency in your banking. Try to deposit all your DoorDash earnings into one primary account. Avoid frequent overdrafts or bouncing cheques. A clean, well-managed bank account spanning several months is the strongest signal of financial responsibility to a lender, even more so than just the total income amount.

The Anatomy of a Gig Worker's Bank Statement

When you submit your bank statements, lenders will perform a detailed analysis. For a DoorDash driver, this involves clearly identifying all gig-related income. Look for recurring deposits from "DoorDash," "SkipTheDishes," "UberEats," or similar platform names. It's helpful if these deposits are clearly identifiable and regular, even if the amounts vary.

Beyond income, lenders also pay close attention to your expenses. They're not trying to judge your lifestyle, but rather to understand your debt-to-income ratio and your overall financial management. They'll look for:

- Regular Bills: Rent/mortgage, utility payments, phone bills, loan payments. These demonstrate your ability to meet ongoing financial obligations.

- Discretionary Spending: While less critical, excessive discretionary spending compared to income might be a yellow flag.

- The Importance of a Healthy Average Daily Balance: A bank account that consistently maintains a positive balance above zero, without frequent dips into overdraft, indicates financial stability and good money management. This shows you have a buffer and aren't living paycheque-to-paycheque, even if those "paycheques" are daily DoorDash deposits.

Income Fluctuations: How Lenders Assess Variability

One of the biggest concerns for gig workers is fluctuating income. Lenders understand that DoorDash earnings might spike during holidays or bad weather and dip during slower periods. The key is to demonstrate an overall trend of stability and sufficient income over time. Lenders aren't necessarily looking for identical deposits every week, but rather a consistent average income that can comfortably cover car loan payments.

Strategies for presenting fluctuating income positively include:

- Longer History: Providing 6 to 12 months of bank statements is usually far more effective than just 3 months. A longer history allows lenders to see the full cycle of your income, smoothing out weekly or seasonal variations and demonstrating a reliable annual earning potential.

- Highlighting Average Income: You might proactively calculate your average monthly income over the past 6-12 months and present it alongside your statements.

- Explanation: Be prepared to explain any significant dips or spikes. For example, "I took a two-week vacation in August, which explains the lower earnings that month."

Navigating the Lender Landscape: Who's Ready to Fund Your Ride in Canada?

When you're a DoorDash driver seeking a car loan in Canada, understanding the diverse landscape of lenders is crucial. Not all financial institutions are created equal, especially when it comes to non-traditional income. Your options can broadly be categorized into traditional banks, dealership financing, and online lenders/brokers.

Finding the right fit in Ontario is key. Major cities like Toronto, Ottawa, and Mississauga have a vibrant financial sector, but also a competitive market. Some lenders in these areas are more accustomed to dealing with varied income streams due to the high concentration of gig workers. However, it's worth noting that the flexibility you find might vary. Expanding horizons to other provinces is also valuable. Lenders in British Columbia, particularly in Vancouver, and Alberta, especially in Calgary, are also increasingly familiar with gig economy income, given the prevalence of ride-sharing and delivery services. Even in Quebec, where the financial landscape has its unique provincial nuances, specialized lenders are emerging to cater to this demographic.

Pro Tip: Don't Settle for the First Offer – Comparison Shopping Across Different Lender Types is Crucial for Better Rates and Terms.

Just like you'd compare prices for a new car, you should compare loan offers. Applying to a few different types of lenders (e.g., a bank you have a relationship with, a dealership, and an online broker) can provide leverage and help you secure the most competitive interest rates and favourable terms. This is especially true for gig workers, as rates can vary significantly depending on the lender's comfort level with your income type.

Traditional Banks: The Conservative Approach

Major Canadian banks like RBC, TD, Scotiabank, BMO, and CIBC tend to have more stringent lending criteria. They often prefer the predictability of traditional employment income, making it potentially challenging for DoorDash drivers to secure a loan solely with bank statements. They might require a longer history of consistent income, a higher credit score, or a larger down payment to mitigate perceived risk.

However, an existing banking relationship can sometimes open doors. If you've been a long-time customer with a good track record (e.g., no overdrafts, other loans paid on time), your bank might be more willing to consider your application. It's always worth exploring, but be prepared for potentially more hurdles or stricter requirements compared to other options.

Dealership Financing: Convenience and Specialization

Dealerships often have in-house finance departments or established relationships with a network of lenders, including those who specialize in non-traditional financing. This can be a significant advantage for DoorDash drivers. These finance managers are often more flexible and experienced in presenting unique income situations to lenders. They understand that their business thrives on getting people approved, and they are often more adept at working with gig economy income.

Dealerships in major centres like Calgary or Vancouver, where the gig economy is robust, are particularly likely to have experience with alternative financing solutions. They can often streamline the application process and sometimes even offer special programs or incentives. The convenience of handling the car purchase and financing under one roof is also a major plus.

Online Lenders and Brokers: The Gig Economy's Best Bet?

The rise of specialized online lenders and brokers has been a game-changer for the gig economy. These platforms are often built specifically to cater to individuals with non-traditional income, including DoorDash drivers. They have developed sophisticated algorithms and underwriting processes that can accurately assess risk based on bank statements and other alternative data points.

Online lenders typically offer speed and efficiency, with many providing pre-approvals within minutes or hours. They cast a wider net, connecting you with multiple lenders who might be more receptive to your income profile. This reach extends across Canada, from the urban centres of Ontario to the more rural areas of Manitoba and Saskatchewan, ensuring that gig workers everywhere have access to financing options. For more insights on how alternative income sources can secure you a vehicle, you might find our article Uber Driver Car Loan: Your Phone *Is* Your Pay Stub particularly helpful.

Beyond the Deposits: Strengthening Your Car Loan Application

While your DoorDash deposits and bank statements are fundamental, they are just one piece of the puzzle. Lenders assess your overall financial health, and there are several other critical factors that can significantly strengthen your car loan application, potentially leading to better approval odds and more favourable terms.

The unsung hero of any loan application is your credit score. This three-digit number, generated by credit bureaus like Equifax and TransUnion in Canada, is a summary of your financial reliability. A strong credit score signals to lenders that you are a low-risk borrower who pays bills on time. Even with consistent DoorDash income, a poor credit score can hinder your approval or result in higher interest rates. Polishing your credit score is an investment in your financial future.

Your debt-to-income (DTI) ratio is another crucial metric. This ratio compares your total monthly debt payments to your gross monthly income. Lenders use it to determine if you have enough disposable income to comfortably afford new loan payments. Even with a good income, if your DTI is too high, lenders might worry about your ability to manage additional debt. Presenting this favourably, by managing existing debt, is vital.

The down payment dilemma is a common one. While it might feel challenging to save up, a down payment is a powerful tool. Even a modest investment upfront can unlock big savings over the life of the loan by reducing the principal amount and therefore the interest paid. Furthermore, a down payment signals commitment and reduces the risk for the lender, significantly boosting your approval odds.

Co-signers can be a strategic ally, especially if you have a lower credit score or limited credit history. A co-signer with strong credit essentially guarantees the loan, making it less risky for the lender. However, it's important to understand the risks and rewards: if you default, the co-signer is equally responsible for the debt. Finally, your vehicle choice impacts your approval odds and affordability. While you might dream of a luxury SUV, choosing a practical, fuel-efficient vehicle that aligns with your DoorDash work can make your application more appealing and demonstrate responsible planning.

Credit Score Mastery for Gig Workers

Understanding your credit score in Canada means knowing about Equifax and TransUnion, the two primary credit bureaus. Your score is influenced by several factors:

- Payment History (35%): Making all payments on time is paramount.

- Credit Utilization (30%): How much credit you use compared to your available credit. Keep this low (ideally below 30%).

- Length of Credit History (15%): Longer histories generally lead to better scores.

- New Credit (10%): Too many recent credit applications can temporarily lower your score.

- Credit Mix (10%): A healthy mix of credit (e.g., credit card, line of credit, small loan) can be beneficial.

Strategies for improving your credit include consistently paying all bills on time, reducing your credit card debt, and regularly checking your credit report for errors to dispute them. Even with a lower credit score, options exist. For example, if you're in Toronto and facing challenges, our article 450 Credit? Good. Your Keys Are Ready, Toronto provides insights into securing a loan with less-than-perfect credit.

Optimizing Your Financial Picture

Managing existing debt is critical for improving your debt-to-income ratio. Focus on paying down high-interest debts first. This not only reduces your DTI but also frees up more income for car loan payments. The power of a modest down payment cannot be overstated. Even 10-20% of the vehicle's price can significantly reduce the loan amount, lower your monthly payments, and signal to lenders that you are a serious and committed borrower, reducing their perceived risk.

Choosing the Right Ride for Your Business

For a DoorDash driver, your car isn't just personal transport; it's a business tool. Balancing personal preference with practical considerations is vital. Prioritize fuel efficiency, reliability, and low maintenance costs. A reasonable car choice not only makes your application more attractive to lenders but also ensures that your vehicle remains a profitable asset for your DoorDash work. A lender will look more favourably on an application for a sensible, affordable sedan than a high-end luxury vehicle when assessing a gig worker's income.

The Fine Print & Hidden Costs: What Every DoorDash Driver Must Know

Securing a car loan as a DoorDash driver, especially with bank statements as your primary income proof, means diving deep into the fine print. It's not just about getting approved; it's about understanding the true cost of your loan to ensure it aligns with your financial goals and business profitability.

Interest rates for non-traditional income can sometimes be higher than for salaried employees due to the perceived increased risk by some lenders. It's important to have realistic expectations, but also to know how to negotiate. Don't assume the first rate offered is the only one available. Understanding loan terms is also paramount: shorter terms mean higher monthly payments but less interest paid overall, while longer terms reduce monthly payments but increase the total cost of the loan over time. For a gig worker, balancing these can be critical for cash flow.

Beyond interest, be vigilant about fees and charges. Unmasking the 'extra' costs is essential. These can include administration fees, documentation fees, late payment penalties, and even early repayment penalties. Always ask for a full breakdown. Finally, insurance imperatives cannot be overlooked. Protecting your investment and income source is critical. As a DoorDash driver, you're using your vehicle for commercial purposes, which may require different insurance coverage than a standard personal policy. Commercial insurance can be more expensive but is often a necessity to ensure you're fully covered in case of an accident while on a delivery.

Pro Tip: Always Request a Full, Itemized Breakdown of All Costs, Fees, and the Total Amount Payable Before Signing Any Agreement.

Never sign a loan agreement without a clear, itemized list of every single cost. This includes the vehicle price, interest charged over the loan term, all administrative fees, and any optional add-ons. This transparency will prevent unwelcome surprises and help you compare offers accurately. This is particularly important for gig workers who need to carefully manage their cash flow in provinces like Nova Scotia and New Brunswick.

Demystifying Interest Rates

Factors influencing interest rates for gig workers typically include your credit score, the loan amount, the loan term, the vehicle's age and value, and the lender's risk assessment of your income stability. While rates might start slightly higher, strategies for securing the most competitive rates available include:

- Improving your credit score prior to application.

- Making a substantial down payment.

- Shopping around with multiple lenders, including specialized online platforms.

- Choosing a more affordable, reliable vehicle.

Rates can vary significantly by province, too, so research local market dynamics in your area, whether you're in Halifax or Vancouver.

Beyond the Monthly Payment: True Cost of Ownership

While the monthly car loan payment is a significant expense, it's only part of the true cost of ownership. For DoorDash drivers, it's crucial to budget for:

- Fuel: Your biggest ongoing expense. Factor in your average weekly mileage for deliveries.

- Insurance: As discussed, commercial insurance will likely be required.

- Maintenance: Regular oil changes, tire rotations, and unexpected repairs. High mileage from deliveries accelerates wear and tear.

- Depreciation: The car's value will decrease over time, especially with high mileage.

Calculating the total cost of the loan over its lifetime, including all interest and fees, combined with these operating costs, will give you a clearer picture of your financial commitment and ensure your DoorDash venture remains profitable.

Your Step-by-Step Blueprint to Car Loan Approval in Canada

Getting a car loan as a DoorDash driver in Canada doesn't have to be daunting. With the right preparation and approach, you can navigate the process successfully. Here's a four-phase blueprint to guide you:

Phase 1: Preparation – Gathering Your Bank Statements, Identification, and Other Essential Documents

This is arguably the most crucial phase. Lenders want a clear, comprehensive picture of your financial health. Start by gathering:

- Bank Statements: Typically 6 to 12 months of your primary checking account statements. Ensure they clearly show your DoorDash deposits and regular expenses.

- Identification: Valid Canadian government-issued ID (e.g., driver's license, passport).

- Proof of Address: Utility bill or lease agreement.

- Social Insurance Number (SIN): For credit checks.

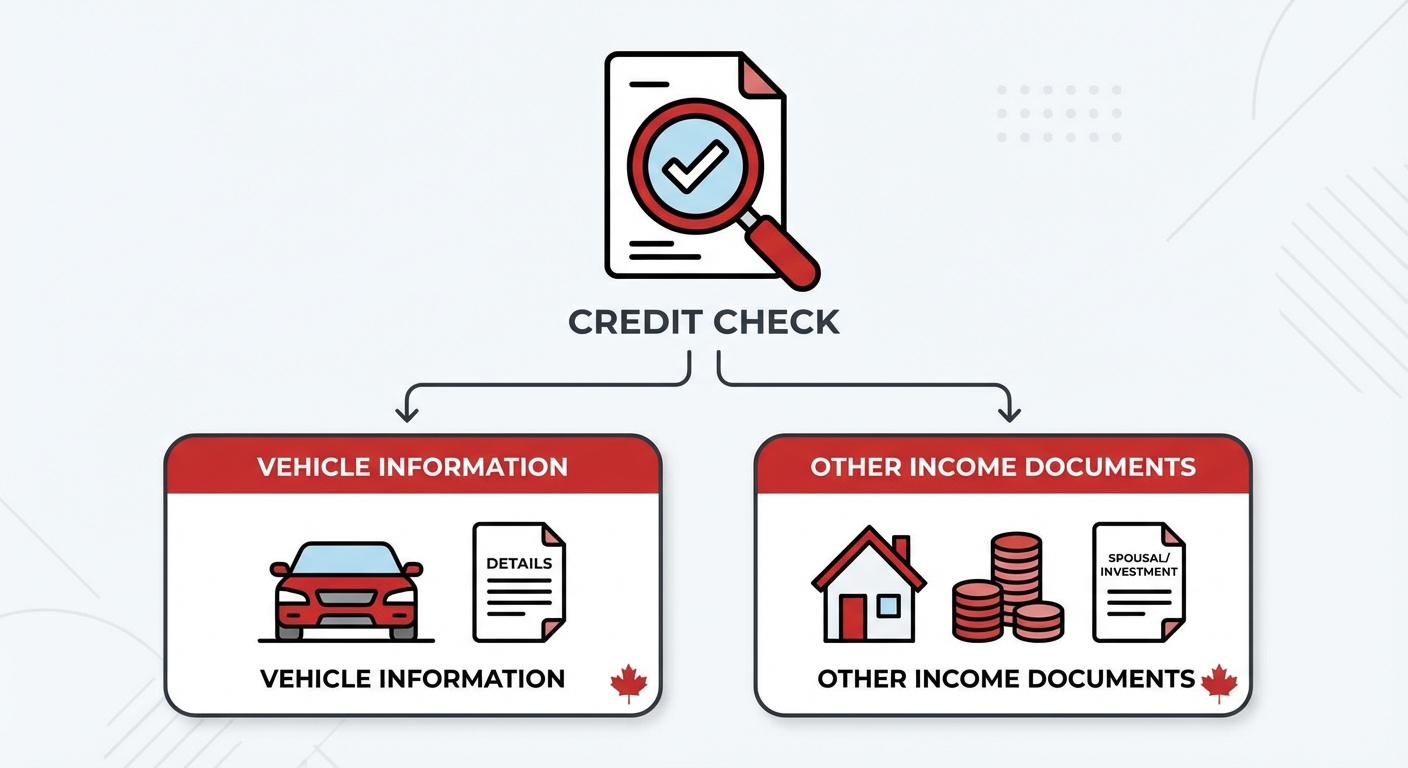

- Vehicle Information (if applicable): If you have a specific car in mind, have its details ready.

- Other Income Documents: If you have any other verifiable income (e.g., spousal income, investments), include documentation.

Context: A DoorDash driver (or an aspiring one) sitting at a kitchen table, intently reviewing recent bank statements and comparing car options on a tablet or laptop. This visually represents the crucial planning and preparation phase before applying for the loan.

Context: A DoorDash driver (or an aspiring one) sitting at a kitchen table, intently reviewing recent bank statements and comparing car options on a tablet or laptop. This visually represents the crucial planning and preparation phase before applying for the loan.

Phase 2: Application – Filling Out the Forms Accurately, Being Honest, and Highlighting Your Financial Strengths

Once your documents are ready, it's time to apply. Whether you're at a dealership in Calgary, an online broker in Toronto, or a bank in Montreal, accuracy is key. Be honest about your income and financial situation. Don't inflate earnings or hide debts, as lenders will verify this information. Clearly highlight your financial strengths, such as consistent DoorDash deposits, a low debt-to-income ratio, or a solid down payment.

When communicating with lenders, be prepared to explain the nature of your gig work. Clearly articulate how your DoorDash earnings contribute to a stable income, even if it's not a traditional salary. Emphasize your commitment to responsible financial management. For more specific advice on applying with non-traditional income, our article Cash Income Only? That's Not a Problem, It's Your Car Loan, Vancouver offers valuable strategies.

Phase 3: Negotiation – Empowering Yourself to Secure the Best Possible Rates and Terms

Don't be afraid to negotiate! With your preparation complete, you're in a stronger position. Compare offers from different lenders. If one lender offers a higher interest rate, politely inquire if they can match a competitor's offer or provide a better deal, especially if you have a strong application. Discuss loan terms (length of the loan) and any associated fees. Remember, every percentage point and every fee reduction adds up to significant savings over the life of the loan.

Phase 4: Finalizing the Deal – What to Double-Check Before You Sign on the Dotted Line

Before you sign, review everything with a fine-tooth comb. Double-check:

- The exact interest rate and APR (Annual Percentage Rate).

- The total loan amount, including all fees.

- The monthly payment amount and the total number of payments.

- Any pre-payment penalties or other hidden clauses.

- The vehicle's make, model, VIN, and purchase price.

- Your insurance coverage, ensuring it meets requirements for commercial use if applicable.

Ask any lingering questions. A reputable lender will be happy to clarify everything. Once you're fully satisfied and understand all aspects of the agreement, then, and only then, sign the dotted line. Congratulations, you're officially a car owner powered by your DoorDash hustle!

Real-World Success Stories: DoorDash Drivers Who Drove Away Happy

It's one thing to understand the theory; it's another to see it in action. Across Canada, DoorDash drivers are successfully securing car loans, proving that the gig economy is a viable path to vehicle ownership. Here are a few real-world examples:

Case Study 1: 'Maria from Calgary: From Bike to Brand New Sedan – A Story of Consistent Deposits and Smart Saving.'

Maria, a 28-year-old DoorDash driver in Calgary, Alberta, started delivering on her bike. She meticulously saved her earnings, depositing every DoorDash payout into a dedicated bank account. After 10 months, she had a consistent history of income, averaging $3,000 per month, and a modest down payment of $2,500. Despite having a limited credit history, her organized bank statements, showing no overdrafts and a healthy average balance, impressed a local dealership that specialized in alternative financing. She was approved for a loan on a fuel-efficient compact sedan, allowing her to expand her delivery area and significantly increase her earnings.

Case Study 2: 'Jean-Pierre from Montreal: Building Credit and a Business with His Delivery Car, Even with Past Challenges.'

Jean-Pierre, 35, from Montreal, Quebec, had faced some credit challenges in the past, including a consumer proposal that had recently been completed. He found it difficult to get approved through traditional banks. However, he had been consistently driving for DoorDash for over a year, diligently making deposits into his bank account. With 12 months of detailed bank statements and a clear explanation of his past credit issues, an online lender specializing in second-chance auto financing saw his commitment. They approved him for a loan on a used minivan, which not only served his DoorDash business but also provided reliable family transport, helping him rebuild his credit history in the process.

Case Study 3: 'Sarah from Halifax: The Power of Proactive Communication and an Organized Application, Securing a Loan in the Maritimes.'

Sarah, a university student in Halifax, Nova Scotia, supplemented her studies by driving for DoorDash. Her income fluctuated based on her class schedule. When applying for a car loan, she anticipated lenders' concerns about her variable income. She proactively organized her bank statements, highlighting her average monthly earnings over the past 8 months. She also wrote a brief letter explaining her income patterns, demonstrating her understanding of peak and off-peak delivery times, and outlining her commitment to making payments. Her proactive communication and extremely organized application, combined with a relatively clean credit file, helped her secure an affordable loan from a regional credit union that valued her transparency and effort.

Lessons from the Road: Common Threads in Successful Applications

These stories highlight several common themes: the importance of financial discipline, clear record-keeping, and the willingness to seek out lenders who understand the gig economy. Persistence and a well-prepared application truly make a difference, proving that your DoorDash deposits can indeed buy you a car in Canada.

Maintaining Momentum: Post-Approval Financial Wisdom for DoorDashers

Congratulations, you've secured your car loan and are now driving for DoorDash with your new (or new-to-you) vehicle! But the journey doesn't end there. Maintaining good financial habits post-approval is just as crucial as the application process. Your car loan can be a powerful tool for building your credit and enhancing your financial future, but only if managed wisely.

Making payments on time is the absolute foundation of future financial freedom and credit building. Every on-time payment reinforces your credit score, proving to credit bureaus and future lenders that you are a reliable borrower. This positive payment history will be invaluable if you ever need another loan, whether it's for a mortgage, a business venture, or even another vehicle. Missed payments, however, can quickly damage the credit you're trying to build, leading to higher interest rates and difficulty securing future credit.

Keep an eye on refinancing opportunities. As your credit score improves with consistent on-time payments, and if market interest rates drop, you might be able to refinance your car loan for lower rates or better terms. This could significantly reduce your total interest paid and your monthly payments, freeing up more cash flow for your DoorDash business or personal savings. Finally, think about leveraging your car for more income. While DoorDash is great, having a reliable vehicle opens doors to exploring other gig platforms or opportunities, further diversifying and strengthening your income streams.

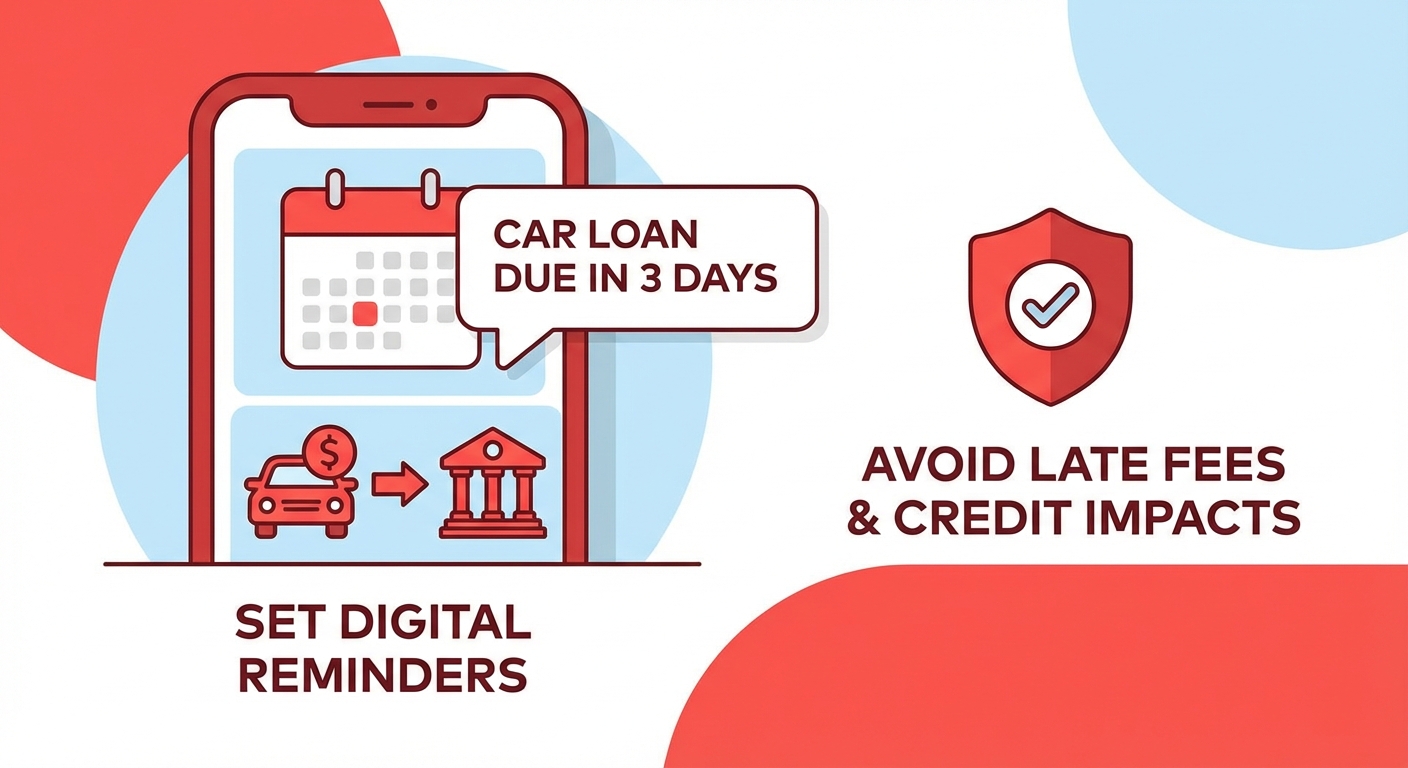

Pro Tip: Automate Your Payments and Set Reminders to Avoid Missed Deadlines, Protecting Your Credit Score and Loan Terms.

Life as a DoorDash driver can be busy and unpredictable. To ensure you never miss a payment, set up automatic debits from your bank account for your car loan payments. Additionally, set digital reminders a few days before each payment is due to ensure you have sufficient funds in your account. This simple step can save you from late fees, negative credit impacts, and unnecessary stress.

Context: A gleaming car, possibly with a subtle DoorDash branding sticker, parked in front of a Canadian landmark (e.g., Toronto skyline, Vancouver mountains). A happy DoorDash driver is getting out of the car, holding a delivery bag, symbolizing successful business and financial independence achieved through the car loan.

Context: A gleaming car, possibly with a subtle DoorDash branding sticker, parked in front of a Canadian landmark (e.g., Toronto skyline, Vancouver mountains). A happy DoorDash driver is getting out of the car, holding a delivery bag, symbolizing successful business and financial independence achieved through the car loan.

Smart Financial Habits for Car Owners

Beyond the loan payment itself, budgeting for ongoing car expenses is essential. This includes fuel, insurance (remembering potential commercial requirements), and maintenance. Given the high mileage often associated with DoorDash work, your maintenance costs might be higher than average. Setting aside a portion of your earnings for these costs, along with building an emergency fund for unexpected car repairs, will ensure your vehicle remains a dependable asset rather than a financial burden.

The Path to Financial Growth

A successfully managed car loan is more than just a means to get around; it's a stepping stone to greater financial growth. It demonstrates your ability to handle significant debt responsibly, which can open doors to other financial products like mortgages or business loans. As your income and credit profile strengthen, explore opportunities to expand your gig work, diversify your income streams, or even transition into other entrepreneurial ventures, all supported by the reliable transportation you've secured.

Your Road Ahead: Solidifying Your Financial Future on Four Wheels

The landscape of car financing in Canada is undeniably changing, and for DoorDash drivers and other gig economy workers, this shift is a welcome one. The days when a traditional pay stub was the sole gatekeeper to car ownership are fading. Your consistent DoorDash deposits, meticulously documented through your bank statements, are now a powerful testament to your earning potential and financial responsibility.

The core principles for gig worker car loans with bank statements only boil down to transparency, consistency, and proactive financial management. By understanding what lenders look for, preparing your documents thoroughly, and choosing the right financing partner, you can overcome the unique challenges of non-traditional income. This isn't just about getting a car; it's about empowering your entrepreneurial journey. A reliable vehicle is often the catalyst for growth in the gig economy, enabling you to take on more deliveries, expand your service area, and ultimately increase your income.

The future of financing for the gig economy is bright. As more Canadians embrace flexible work, financial institutions will continue to adapt, offering more tailored solutions for DoorDashers and beyond. By staying informed and financially astute, you're not just buying a car; you're investing in your independence, your business, and your future on the open road.