Uber Driver, No Credit? Your Car Loan Just Solved Your First Problem. Toronto.

Table of Contents

- Uber Driver, No Credit? Your Car Loan Just Solved Your First Problem. Toronto.

- Key Takeaways: Your Fast Track to an Uber-Ready Car in Canada

- The Urgent Imperative: Why Your Uber Career in Toronto Demands a Car Now, Not Later

- Demystifying 'No Credit': How New Uber Drivers in Canada Can Still Secure Financing

- Beyond the Score: What Lenders Really Evaluate When You Have No Credit History

- The 'New to Canada' Advantage: Navigating Car Loans as a Recent Immigrant

- Your Loan Lifelines: Specialized Dealerships vs. Traditional Banks for Urgent Uber Car Loans

- The Dealership Advantage: In-House Financing & Speed for No-Credit Applicants in Toronto

- Why Banks Might Not Be Your First Stop (and When They Are the Right Choice)

- The Application Blueprint: Your Step-by-Step Guide to Urgent Car Loan Approval in Canada

- Gathering Your Arsenal: Essential Documents You'll Absolutely Need

- Crafting Your Story: Presenting Your Case for Loan Approval Effectively

- The Co-Signer Advantage: When a Helping Hand Speeds Up Approval and Improves Terms

- Beyond the Loan: Smart Car Choices for Maximum Uber Profitability in Toronto and Beyond

- Uber's Vehicle Requirements: What You *Must* Verify Before You Buy

- Top Picks for Toronto Uber Drivers: Where Fuel Efficiency Meets Unbeatable Reliability

- The True Cost of Ownership: Fuel, Insurance, and Maintenance in Canadian Cities

- Navigating the Fine Print: Understanding Your Urgent Car Loan Terms in Canada

- Interest Rates for No-Credit Loans: Realistic Expectations and Improvement Strategies

- Hidden Fees & Charges: What to Scrutinize in Your Loan Agreement

- Payment Schedules & Flexibility: Aligning Your Loan with Your Uber Income Cycle

- Building Your Financial Future: From Urgent Loan to Excellent Credit in Canada

- The Power of On-Time Payments: How Your Uber Car Loan Builds Your Credit Score

- When to Refinance: Proactively Lowering Your Payments and Interest Rates

- Your Next Steps to Approval: Driving Your Uber Career Forward in Toronto and Across Canada

- Ready to Drive? Your Personalized Action Plan for Immediate Success

- Frequently Asked Questions (FAQ): Urgent Car Loans for New Uber Drivers in Canada

Uber Driver, No Credit? Your Car Loan Just Solved Your First Problem. Toronto.

You've got the drive, the ambition, and a burning desire to start earning on your own terms. Becoming an Uber driver in a bustling metropolis like Toronto offers incredible flexibility and income potential. But there's a catch, isn't there? That crucial first step: getting a reliable vehicle. And if you're like many aspiring drivers, perhaps new to Canada or simply haven't had the chance to build a credit history, the thought of securing a car loan can feel like hitting a roadblock before you've even started.

Let's be clear: this isn't just about owning a car; it's about launching your career. A dependable vehicle is your business's foundation. Without it, you can't pick up riders, you can't earn, and your entrepreneurial dreams remain just that – dreams. This article isn't just a guide; it's your definitive roadmap to overcoming the "no credit" hurdle and getting behind the wheel of an Uber-ready car, quickly and effectively, right here in Toronto and across Canada.

Key Takeaways: Your Fast Track to an Uber-Ready Car in Canada

- Specialized Financing is Your Best Bet: Traditional banks often aren't equipped for no-credit scenarios. Seek out dealerships and lenders who specialize in alternative financing.

- 'No Credit' Isn't a Dead End: Lenders look beyond a score. Your employment stability, residency, and projected Uber earnings can be powerful indicators of your ability to repay.

- Prioritize Affordability and Reliability: For your first Uber car, focus on a fuel-efficient, low-maintenance vehicle that meets Uber's requirements, not luxury. Your goal is to start earning.

- Understand the Full Cost: Beyond monthly payments, factor in fuel, specialized rideshare insurance, and maintenance. These are critical for profitability.

- Speed and Reliability are Paramount: Every day without a car is a day without income. Target lenders and dealerships known for expedited approvals and quick vehicle delivery.

The Urgent Imperative: Why Your Uber Career in Toronto Demands a Car Now, Not Later

Imagine the vibrant streets of Toronto, Calgary, or Montreal, alive with opportunity. Every minute you're not driving for Uber is a missed fare, a lost tip, and a delay in reaching your financial goals. For many, an Uber career isn't just a side hustle; it's a vital income stream, often addressing immediate financial needs. The link between having a dependable car and starting to earn income is direct and undeniable. Delays in securing a vehicle translate directly into an opportunity cost that can be financially burdensome.

Whether you're looking to supplement your income, transition to full-time gig work, or simply need a flexible way to earn money in one of Canada's most expensive cities, a car is non-negotiable. The sooner you're approved for a loan and driving, the sooner you can capitalize on the demand for rideshare services. Waiting for traditional loan approvals, especially when you have no credit history, can set you back weeks, even months. That's weeks or months of potential earnings you're leaving on the table.

Demystifying 'No Credit': How New Uber Drivers in Canada Can Still Secure Financing

When lenders talk about 'no credit,' they're referring to a lack of a documented financial history within Canada's credit reporting system. This isn't necessarily a bad thing, nor does it mean you're a high-risk borrower. It simply means there's no existing data for them to evaluate. This scenario is incredibly common, especially for new immigrants to Canada settling in cities like Toronto, Vancouver, or Montreal, young adults just starting their financial journeys, or individuals who've simply preferred to operate on a cash basis and haven't engaged with credit systems like credit cards or previous loans.

Traditional banks often rely heavily on a credit score to assess risk, which can create a frustrating Catch-22: you need credit to get credit. However, specialized lenders and dealerships understand this unique demographic. They've developed alternative methods to assess your risk, looking beyond a simple three-digit score to understand your true financial picture and repayment capacity.

Beyond the Score: What Lenders Really Evaluate When You Have No Credit History

So, if a credit score isn't the primary factor, what is? Specialized lenders focus on a holistic view of your financial stability. They want to see evidence that you're a responsible individual capable of making consistent payments. Key indicators they'll consider include:

- Consistent Employment: If you have a current job, even if it's not full-time, steady pay stubs are a strong signal. Lenders look for stability in your income source.

- Proof of Residency: Utility bills (hydro, gas, internet) in your name, a lease agreement, or property tax statements in cities like Toronto, Ottawa, or Vancouver demonstrate stability and a fixed address.

- Existing Bank Accounts: Having a chequing or savings account in good standing, with a history of regular deposits and no overdrafts, shows financial management.

- Projected Uber Earnings: This is crucial for aspiring Uber drivers. Prepare a realistic projection of your potential income. Lenders can factor this into your repayment capacity, especially if you can back it with research on average Uber driver earnings in your area. For more insights on how alternative income sources can secure your loan, you might find our article on Self-Employed? Your Bank Account *Is* Your Proof. Get Approved. particularly helpful.

- Down Payment: Even a modest down payment can significantly boost your application by reducing the loan amount and showing your commitment.

The 'New to Canada' Advantage: Navigating Car Loans as a Recent Immigrant

Canada welcomes newcomers, and the financial system is increasingly adapting to support them. If you're a recent immigrant to major Canadian cities like Toronto, Vancouver, or Montreal, you likely have no Canadian credit history. However, this doesn't mean you're without options. Many specialized lenders understand that you might have a stable job offer, foreign assets, or even a strong financial background from your home country. While foreign credit history isn't directly transferable, demonstrating financial stability through other means is key.

Some programs and lenders specifically cater to this demographic, often requiring proof of a stable job, permanent residency status, and a reasonable down payment. They understand that building Canadian credit takes time, and a car loan can be the perfect first step. For a deeper dive into how newcomers can secure vehicle financing, check out our guide on Approval Secrets: How International Students Get Car Loans in Ontario.

Your Loan Lifelines: Specialized Dealerships vs. Traditional Banks for Urgent Uber Car Loans

When seeking a car loan, especially with no credit history and an urgent need, you essentially have two main avenues: traditional banks and specialized dealerships. Understanding the distinct advantages and disadvantages of each is paramount to making the right choice for your Uber career.

The Dealership Advantage: In-House Financing & Speed for No-Credit Applicants in Toronto

For aspiring Uber drivers with no established credit, specialized dealerships often emerge as the superior choice. Why? Because they operate differently. Dealerships that focus on alternative or subprime financing understand the nuances of non-traditional applications. They don't just rely on a single credit score; they look at your entire financial picture, including your income stability, residency, and the specific vehicle you're interested in.

Here's how they provide an advantage:

- Faster Approvals: Dealerships, particularly those with in-house financing departments or strong relationships with multiple niche lenders, can often provide approval decisions much faster than traditional banks – sometimes within hours. This speed is crucial when your income depends on getting a vehicle quickly.

- Flexible Terms: They are more willing to work with applicants who have no credit, offering terms that might be considered unconventional by a bank but are perfectly suitable for your situation.

- Leveraging Multiple Lenders: A good specialized dealership acts as a broker, submitting your application to several lenders in their network who are accustomed to approving no-credit applicants. This increases your chances of approval.

- Bundled Services: Many dealerships can offer a comprehensive package, including the vehicle, the loan, and sometimes even assistance with finding appropriate rideshare insurance, streamlining the entire process.

Why Banks Might Not Be Your First Stop (and When They Are the Right Choice)

Traditional banks and credit unions, while offering potentially lower interest rates for those with excellent credit, typically have much stricter lending criteria. Their systems are heavily reliant on established credit scores and extensive credit histories. For someone with no credit, their requirements can be a significant barrier.

- Stricter Requirements: Banks are less likely to approve loans for individuals with no credit history, as they lack the data points their algorithms demand.

- Slower Process: Their approval processes can be more bureaucratic and time-consuming, which is a luxury an aspiring Uber driver often doesn't have.

- Limited Flexibility: They generally offer less flexibility in terms and conditions for applicants outside their prime lending criteria.

However, there are specific scenarios where a bank might be a viable option:

- Strong Co-Signer: If you have a family member or friend with excellent credit who is willing to co-sign the loan, a bank might consider your application.

- Existing Banking Relationship: If you have a long-standing, positive relationship with your bank (e.g., a history of significant savings, investments, or other products), they *might* be more inclined to work with you.

But for urgent, no-credit situations, especially for an Uber career, managing your expectations with traditional banks is essential. Your best bet for immediate action will almost always be with specialized dealerships.

| Feature | Specialized Dealerships | Traditional Banks/Credit Unions |

|---|---|---|

| Approval Speed | Fast (often within hours/days) | Slower (days to weeks) |

| No-Credit Applicant Acceptance | High (their specialty) | Low (rarely, unless strong co-signer) |

| Flexibility in Terms | High (tailored solutions) | Low (standardized products) |

| Lender Network | Access to multiple niche lenders | Primarily their own products |

| Interest Rates (No Credit) | Higher (reflects increased risk) | Potentially lower (if approved, but rare for no-credit) |

| Application Process | Streamlined, often online with dealer support | More rigorous, extensive documentation |

The Application Blueprint: Your Step-by-Step Guide to Urgent Car Loan Approval in Canada

Securing an urgent car loan with no credit requires preparation and a strategic approach. Don't just walk into a dealership or submit an online application without gathering your "arsenal" first. Being prepared can significantly speed up the approval process and improve your chances of success.

Gathering Your Arsenal: Essential Documents You'll Absolutely Need

Think of this as assembling your financial identity. The more organized and complete your documentation, the smoother your application process will be. Here's what you'll typically need:

- Valid Canadian Driver's License: For Ontario, this means a G-class license. Ensure it's current and in good standing.

- Proof of Residency: This is critical for confirming your address. Bring recent utility bills (hydro, gas, internet), a current lease agreement, or property tax statements. These should clearly show your name and address in cities like Toronto, Edmonton, or Halifax.

- Proof of Income: This is arguably the most vital document when you have no credit.

- Employment: Recent pay stubs (typically 2-3 months), a letter of employment, or bank statements showing consistent direct deposits.

- Projected Uber Earnings: If you're new to Uber, prepare a realistic projection. This could include market research on average Uber driver incomes in your area, and a written statement outlining your commitment and plan.

- Other Income: If you receive other forms of verifiable income (e.g., benefits, pensions), have official statements ready. For insights into using various income streams, consider our article EI Income? Your Car Loan Just Said 'Welcome Aboard!'.

- Government-Issued Identification: A valid passport, Canadian permanent resident card, or provincial identification card.

- Bank Account Information: Details of your chequing or savings account for setting up payments.

Crafting Your Story: Presenting Your Case for Loan Approval Effectively

Beyond the documents, how you present your situation to the lender or dealership matters. Be transparent, confident, and articulate:

- Be Honest About Your Financial Situation: Don't try to hide the fact you have no credit. Instead, explain *why* (e.g., new to Canada, young adult).

- Clearly Articulate Your Commitment to Uber Driving: Explain your business plan. Why Uber? What are your projected hours? How does this car directly enable your income? This helps lenders see the immediate revenue potential.

- Demonstrate Repayment Capacity and Intent: Show that you've thought about how you'll make payments. Highlight any savings, other income streams, or a budget you've created.

- The Strategic Role of a Down Payment: Even a modest down payment (5-10% of the vehicle's price) can significantly strengthen your application. It reduces the amount you need to borrow, lowers the risk for the lender, and demonstrates your commitment.

The Co-Signer Advantage: When a Helping Hand Speeds Up Approval and Improves Terms

If you have a trusted family member or friend with good credit who is willing to co-sign your loan, this can be a game-changer. A co-signer essentially guarantees the loan, promising to make payments if you default. This significantly reduces the risk for the lender, often leading to:

- Enhanced Approval Odds: Even with no credit history, a strong co-signer can make your application highly attractive.

- More Favourable Interest Rates: With reduced risk, lenders are often willing to offer lower interest rates, saving you money over the life of the loan.

However, it's crucial to understand the responsibilities involved for both parties. The co-signer is equally responsible for the debt, and any missed payments will negatively impact *their* credit score as well as yours. Ensure open communication and a clear understanding before pursuing this option.

Beyond the Loan: Smart Car Choices for Maximum Uber Profitability in Toronto and Beyond

Securing the loan is a major hurdle cleared, but choosing the right vehicle is equally critical for your success as an Uber driver. Your car is your primary business asset, and selecting wisely can make a significant difference to your profitability in the dynamic markets of Toronto, Vancouver, Calgary, and Montreal.

Uber's Vehicle Requirements: What You *Must* Verify Before You Buy

Before you fall in love with a car, ensure it meets Uber's specific requirements for drivers in Ontario. These can vary slightly by region but generally include:

- Vehicle Age: Typically, vehicles must be 10 model years old or newer (e.g., if it's 2024, a 2014 model or newer).

- Condition: The vehicle must be in excellent working condition, with no cosmetic damage, missing parts, or commercial branding.

- Seating Capacity: Must have 4 doors and seat a minimum of 4 passengers (excluding the driver).

- Registration & Insurance: Must have valid Ontario registration and, crucially, appropriate rideshare insurance. This is a common pitfall – personal car insurance is insufficient for rideshare.

- Safety Standards: Must pass an annual vehicle inspection (Safety Standards Certificate in Ontario).

Always check the most up-to-date requirements on Uber's official website for your specific city before finalizing any purchase to avoid costly rejections.

Top Picks for Toronto Uber Drivers: Where Fuel Efficiency Meets Unbeatable Reliability

For an Uber driver, reliability and fuel efficiency are paramount. Downtime for repairs means lost income, and high fuel costs eat into your profits. Consider these popular and proven choices for used cars in Canadian cities:

- Toyota Corolla/Camry: Legendary for their bulletproof reliability, low maintenance costs, and excellent fuel economy. Parts are readily available and affordable.

- Honda Civic/CR-V: Another strong contender, offering similar reliability and efficiency. The CR-V offers more space if you anticipate larger groups or luggage.

- Hyundai Elantra/Kona: Modern Hyundai models offer great value, good fuel economy, and increasingly strong reliability, often with better tech features for the price.

- Hybrid Options (e.g., Toyota Prius, Hyundai Ioniq): While potentially a higher upfront cost, hybrids offer significant long-term fuel savings, especially with the stop-and-go driving typical of urban centres like Toronto. The savings on gas can quickly offset the initial premium.

Focus on a vehicle with a clean service history and relatively low kilometres for its age.

The True Cost of Ownership: Fuel, Insurance, and Maintenance in Canadian Cities

The car loan payment is just one piece of the puzzle. To truly maximize your Uber profitability, you must account for the full cost of ownership. These costs can vary significantly across Canada:

- Fuel Costs: Gas prices fluctuate but tend to be higher in provinces like British Columbia and Quebec, while generally more affordable in Alberta. Ontario sits in the middle. Your fuel-efficient vehicle choice will directly impact this daily expense.

- Insurance Considerations: This is a critical point for rideshare drivers in Ontario. Personal auto insurance does NOT cover commercial ridesharing. You will need specialized rideshare insurance, which is often significantly higher than standard personal policies. Obtain multiple quotes before committing to a vehicle.

- Routine Maintenance: Budget for regular oil changes, tire rotations, brake inspections, and occasional repairs. Reliable cars keep these costs lower, but they are inevitable. Costs for labour can vary between major cities like Toronto, Calgary, and Montreal.

| Cost Factor | Impact on Uber Profitability | Regional Considerations (Examples) |

|---|---|---|

| Fuel Efficiency | Directly reduces operating expenses, higher net income per ride. | Higher gas prices in British Columbia and Quebec make efficiency critical. |

| Rideshare Insurance | Mandatory, often significantly higher than personal insurance. Crucial for legal operation. | Ontario has strict rideshare insurance requirements; costs can vary significantly by driver and vehicle. |

| Maintenance & Repairs | Unplanned downtime means lost income; reliable cars minimize this. | Labour rates for mechanics can be higher in larger cities like Toronto and Vancouver. |

| Vehicle Depreciation | Long-term cost, impacts resale value. | Popular, reliable models tend to hold value better in Canada. |

Navigating the Fine Print: Understanding Your Urgent Car Loan Terms in Canada

You're almost there! Before you sign on the dotted line, it's absolutely crucial to understand the terms and conditions of your car loan. This is where financial literacy empowers you, allowing you to ask the right questions and avoid potential pitfalls, especially when dealing with no-credit financing.

Interest Rates for No-Credit Loans: Realistic Expectations and Improvement Strategies

Let's be realistic: when you have no credit history, the interest rates offered on your initial car loan will likely be higher than those for someone with an excellent credit score. This reflects the increased risk lenders perceive. However, don't view this as a permanent state; view it as a necessary stepping stone.

- Realistic Expectations: Prepare for rates that might be in the higher single digits or even double digits. Focus on the total monthly payment and ensure it's manageable within your projected Uber income.

- Improvement Strategies: Your goal with this first loan is to establish a positive payment history. Consistently making on-time payments will systematically build your credit score. Once your score improves (typically after 12-18 months of diligent payments), you can explore refinancing options to secure a lower interest rate, potentially saving you thousands of dollars over the remaining loan term.

Hidden Fees & Charges: What to Scrutinize in Your Loan Agreement

The sticker price and advertised interest rate aren't the only figures to consider. Loan agreements can contain various fees and charges that inflate the total cost. Always read the entire contract thoroughly and ask for clarification on anything you don't understand:

- Administration Fees: Common for processing the loan, but ensure they are reasonable and clearly disclosed.

- PPSA Registration Fees: Personal Property Security Act (PPSA) registration fees are standard in Canada, registering the lender's interest in the vehicle.

- Extended Warranty Pitches: While sometimes beneficial, these are often high-profit items for dealerships. Understand what's covered, the cost, and if it's truly necessary for your Uber vehicle. You can often purchase these separately later if desired.

- Mandatory Add-ons: Be wary of "mandatory" protection packages (e.g., rust proofing, paint protection) that significantly inflate the loan amount without clear value.

Never feel pressured to sign until every line item is understood and you're comfortable with the total cost.

Payment Schedules & Flexibility: Aligning Your Loan with Your Uber Income Cycle

Your loan payment schedule should align seamlessly with your income. Uber drivers often receive payments weekly or bi-weekly, so choosing a payment schedule that mirrors this can prevent cash flow issues.

- Payment Frequency: Most lenders offer monthly, bi-weekly, or even weekly payment options. Bi-weekly often works well for Uber drivers as it aligns with typical payout schedules and results in paying off the loan slightly faster (26 bi-weekly payments vs. 12 monthly).

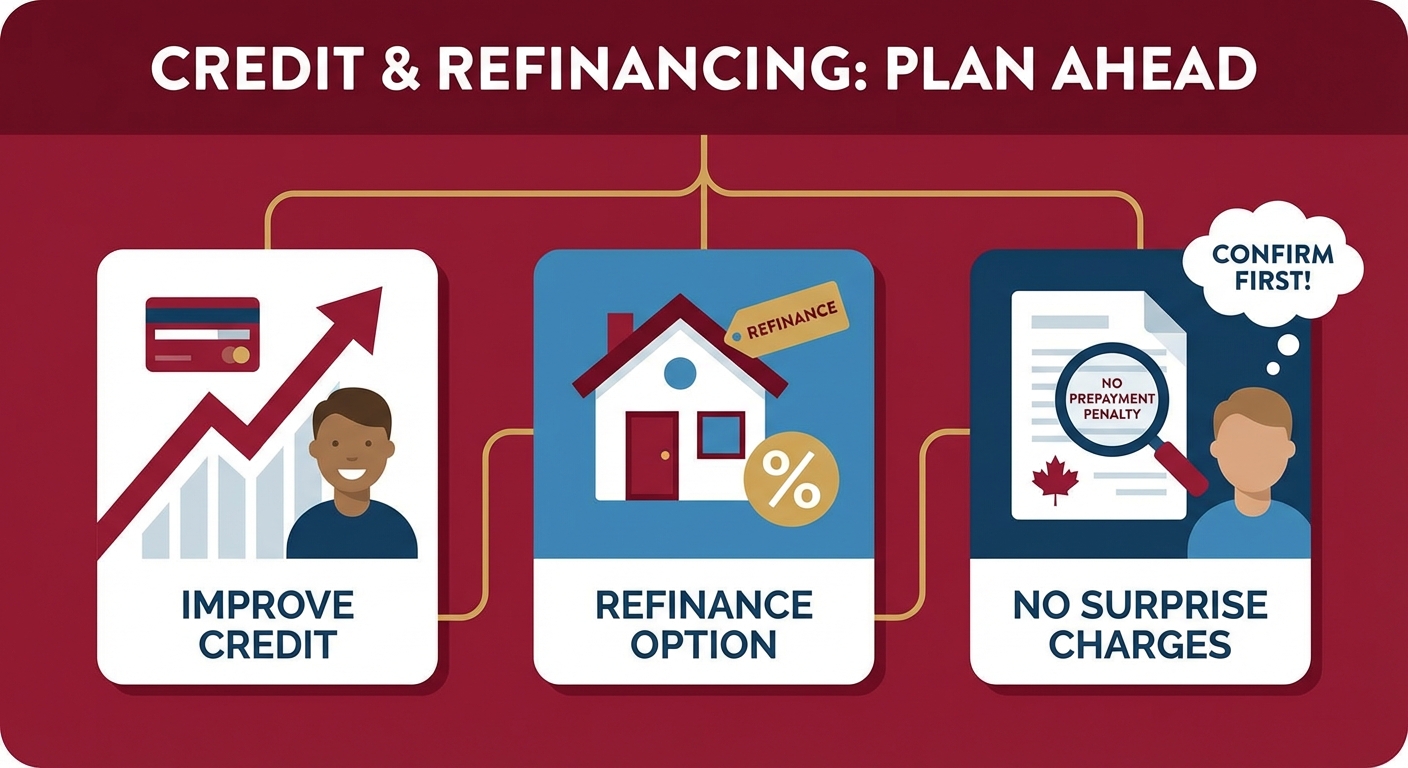

- Prepayment Penalties: Understand if your loan agreement includes any penalties for paying off the loan early. While you might not plan to do so immediately, improving your credit could lead to refinancing, and you don't want to be surprised by extra charges. Many subprime loans in Canada do not have prepayment penalties, but it's essential to confirm.

Building Your Financial Future: From Urgent Loan to Excellent Credit in Canada

This urgent car loan isn't just about getting an Uber-ready vehicle; it's a foundational step in building a robust financial future. By securing and responsibly managing this loan, you're not just making car payments; you're making an investment in your creditworthiness, systematically opening doors to better financial products and opportunities down the road.

The Power of On-Time Payments: How Your Uber Car Loan Builds Your Credit Score

Every single on-time payment you make on your car loan is reported to Canada's major credit bureaus, Equifax and TransUnion. These positive reports are the building blocks of your credit score. Here's how it works:

- Payment History: This is the most significant factor in your credit score (accounting for roughly 35%). Consistent, on-time payments demonstrate reliability and responsibility.

- Credit Mix: A car loan diversifies your credit profile, showing you can manage different types of credit (installment loans vs. revolving credit like credit cards).

- Length of Credit History: The longer your account is open and in good standing, the more positive impact it has. This initial loan starts that timeline.

Think of this car loan as a strategic tool. It's your opportunity to prove your financial reliability, transforming your "no credit" status into a solid credit foundation that will serve you well for years to come.

When to Refinance: Proactively Lowering Your Payments and Interest Rates

Once you've consistently made payments on your car loan for 12 to 18 months, and your credit score has demonstrably improved, it's time to consider refinancing. This is a proactive strategy that can save you a significant amount of money.

Refinancing involves taking out a new loan, typically with a lower interest rate, to pay off your existing car loan. With your improved credit score, you'll be a more attractive borrower to a wider range of lenders, including traditional banks. The benefits can include:

- Lower Interest Rate: Directly translates to lower overall cost of the loan.

- Reduced Monthly Payments: Frees up more cash flow for your business or personal needs.

- Shorter Loan Term: Potentially pay off your car faster, reducing the total interest paid.

Regularly monitoring your credit score and being aware of current interest rates will help you identify the opportune moment to refinance.

Your Next Steps to Approval: Driving Your Uber Career Forward in Toronto and Across Canada

The path from "no credit" to "Uber driver with a reliable car" is not just a dream; it's a wholly achievable reality. With the right information, preparation, and approach, you can overcome the initial hurdles and launch your flexible, income-generating career. Securing that urgent car loan is more than just buying a vehicle; it's an investment in your immediate financial stability and your long-term credit health.

Don't let the lack of a credit history deter you. Specialized lenders and dealerships across Canada, particularly in vibrant markets like Toronto, are ready and willing to work with aspiring Uber drivers. Your ambition, your commitment to earning, and a strategic approach to financing are your most powerful assets.

Ready to Drive? Your Personalized Action Plan for Immediate Success

Here’s your concise roadmap to getting behind the wheel:

- Gather Your Documents: Collect all necessary proof of ID, residency, and income (including projected Uber earnings).

- Identify Reputable Specialized Lenders/Dealerships: Look for those in your area (especially Toronto) known for alternative financing and working with no-credit applicants.

- Confidently Submit Your Application: Be transparent about your credit situation and clearly articulate your Uber career plan.

- Intelligently Select Your Vehicle: Choose a fuel-efficient, reliable, Uber-compliant car that maximizes your profitability.

- Understand and Agree to Your Loan Terms: Review all details, including interest rates and fees, before signing.

The road to financial independence as an Uber driver in Canada starts now. Take that first crucial step, and you'll be on your way to earning on your terms.