ODSP in Ontario? Your Car Loan Just Found Its Favourite Client.

Table of Contents

- ODSP in Ontario? Your Car Loan Just Found Its Favourite Client.

- Key Takeaways

- Chapter 1: The 'Impossible' Dream Debunked – Why ODSP Car Loans Are Not Only Possible, But Common in Ontario

- Breaking the Myth: ODSP as a Stable Income Source

- The Lender's Lens: Beyond Just the Dollar Amount

- Why a Car is More Than a Luxury for ODSP Recipients in Ontario

- Chapter 2: Decoding the Approval Matrix – What Lenders *Really* Want to See From ODSP Applicants

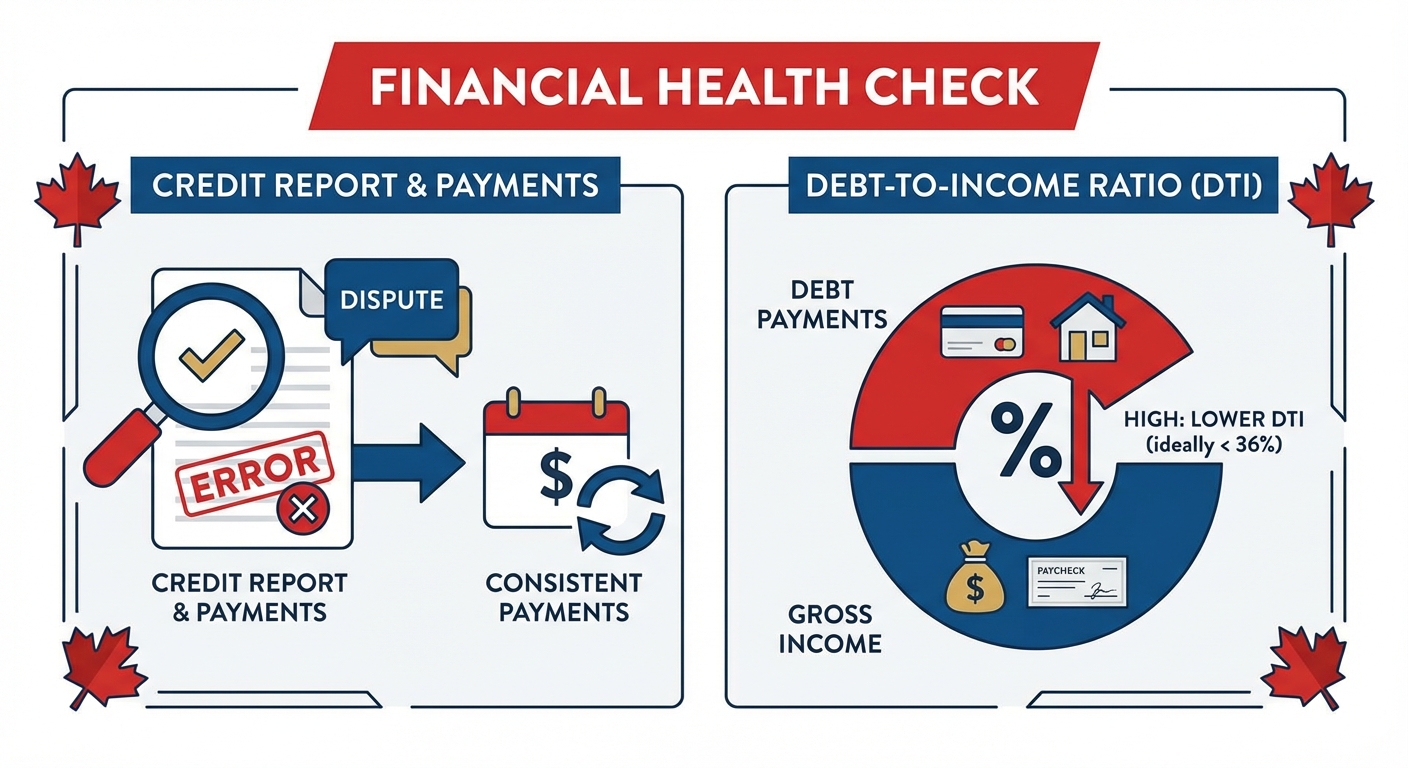

- The Power of Your Credit Score: Understanding the Numbers Game

- Income Stability & Supplementary Sources: Building a Stronger Financial Profile

- Debt-to-Income Ratio: Your Invisible Approval Hurdle

- The Down Payment Advantage: Boosting Your Odds and Lowering Costs

- The Co-Signer Conundrum: A Double-Edged Sword for ODSP Borrowers

- Chapter 3: Your Strategic Playbook – Crafting an Irresistible Application in Ontario

- Pre-Approval: Your Secret Weapon for Confidence and Negotiation

- Gathering Your Financial Arsenal: Documents You'll Need

- Budgeting for Reality: Beyond the Monthly Payment

- Chapter 4: Navigating Ontario's Lending Landscape – Where to Find ODSP-Friendly Car Loans

- Dealership Financing: The Convenience Factor and Its Caveats

- Banks vs. Credit Unions: Traditional Lenders and Community Support

- Specialized Lenders: Your Best Bet for Non-Traditional Income

- Online Car Loan Platforms: Speed, Variety, and Cautionary Tales

- Finding 'ODSP-Friendly' Dealerships & Brokers in Major Ontario Cities

- Chapter 5: Beyond the Sticker Price – Unmasking the True Costs of Car Ownership in Ontario

- Understanding Interest Rates: What to Expect and How to Improve Them

- The Hidden Costs: Fees, Warranties, and Extras to Watch Out For

- Ontario Car Insurance: A Major Budgetary Consideration

- New vs. Used: The ODSP Perspective on Vehicle Choice

- Chapter 6: Driving Forward – Managing Your Loan and Building a Brighter Financial Future

- Mastering Your Monthly Payments: The Cornerstone of Credit Building

- Refinancing Your ODSP Car Loan: When and Why it Makes Sense

- Protecting Your Investment: Maintenance, Warranties, and Emergency Funds

- Your Next Steps to Approval: Charting Your Course in Ontario

- Frequently Asked Questions (FAQ): ODSP Car Loans in Ontario

ODSP in Ontario? Your Car Loan Just Found Its Favourite Client.

A bold promise, but one we're here to unpack. For too long, the narrative around securing a car loan while on the Ontario Disability Support Program (ODSP) has been shrouded in myth and misconception. Many believe that receiving ODSP automatically disqualifies them from vehicle ownership, or at best, relegates them to predatory lending options. We at SkipCarDealer.com are here to tell you that this simply isn't true. This deep-dive article will dismantle those barriers, offering a comprehensive, empowering guide for every ODSP recipient in Ontario aspiring to vehicle ownership.

Imagine the freedom: reliable transportation to medical appointments, easier access to employment opportunities, connecting with family and friends across Ontario's vast landscapes, or simply running errands without the stress and limitations of public transit. This isn't just a pipe dream. We're not just offering hope; we're providing a roadmap to approval, better rates, and sustainable car ownership. Ready to take the wheel?

Key Takeaways

- ODSP is Recognizable Income: Lenders do consider ODSP a stable, verifiable income source, dispelling the myth of automatic disqualification. It's often viewed as more consistent than fluctuating employment income.

- Credit Score Matters, But Isn't Everything: While a strong credit history certainly helps, specific strategies can overcome past challenges or limited credit. Focus on demonstrating financial responsibility in other areas.

- Strategic Preparation is Power: Understanding lender perspectives, building a strong application, and exploring all financing avenues significantly boost your approval odds. Knowledge is your greatest asset.

- Ontario-Specific Resources are Your Ally: From specialized lenders to provincial programs and local credit unions, knowing your options within Ontario is crucial for success.

- Beyond Approval: Focus on Sustainable Ownership: The true win is securing a manageable loan and understanding the full cost of vehicle ownership in the long term, including insurance, fuel, and maintenance.

Chapter 1: The 'Impossible' Dream Debunked – Why ODSP Car Loans Are Not Only Possible, But Common in Ontario

Breaking the Myth: ODSP as a Stable Income Source

The misconception that ODSP disqualifies individuals from securing a car loan is perhaps the biggest hurdle to overcome. Many applicants, and even some uninformed lenders, operate under this false premise. However, the reality is quite different. Lenders, particularly those experienced in non-traditional financing, often view government benefits like ODSP as a highly stable and predictable income source. Think about it: unlike hourly wages that can fluctuate based on shifts, layoffs, or economic downturns, ODSP payments are consistent, guaranteed, and reliable. This inherent stability can be a significant advantage, often perceived as more secure than some forms of employment income.

The challenge isn't the income itself, but how it's presented and understood by the lender. A well-prepared applicant can effectively communicate the reliable nature of their ODSP income, emphasizing its consistent monthly deposit. This understanding is key to unlocking approval, especially in a province like Ontario where many individuals rely on such programs.

The Lender's Lens: Beyond Just the Dollar Amount

While the stability of your ODSP income is a strong foundation, lenders don't just look at the dollar amount you receive. They delve into your overall financial picture, seeking a holistic understanding of your ability to manage debt. What does this entail? They'll scrutinize your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. They'll also consider your living expenses – rent, utilities, groceries, and other necessities – to assess how much disposable income you genuinely have available for a car payment.

The perceived stability of your financial situation goes beyond just income. It includes your payment history on other bills (rent, utilities, phone), your savings habits, and your general financial discipline. This section will empower you to see your finances from a lender's perspective, helping you identify areas to strengthen before you even apply. Understanding these nuances is crucial for crafting an application that truly shines.

Why a Car is More Than a Luxury for ODSP Recipients in Ontario

For many ODSP recipients across Ontario, a reliable vehicle isn't a luxury item; it's a fundamental necessity that unlocks greater independence and quality of life. Consider the vastness of Ontario, from the sprawling urban centres like the Greater Toronto Area (GTA) and Ottawa to the more rural and remote communities. Public transit, while extensive in some cities, can be challenging, unreliable, or simply non-existent for those with disabilities.

A car provides direct access to crucial medical appointments, specialized treatments, and therapy sessions that might be geographically dispersed. It can open doors to part-time employment or volunteer opportunities, fostering social inclusion and contributing to personal growth. For some, it's about maintaining family connections, visiting loved ones, or accessing essential services like grocery stores and pharmacies that are not easily reached by foot or public transport. In many cases, a vehicle directly addresses barriers to full participation in community life, making it an essential tool for navigating daily challenges and enhancing overall well-being.

Chapter 2: Decoding the Approval Matrix – What Lenders *Really* Want to See From ODSP Applicants

The Power of Your Credit Score: Understanding the Numbers Game

Your credit score is a three-digit number that summarizes your creditworthiness, and it plays a significant role in car loan approvals. It's calculated based on factors like payment history, amounts owed, length of credit history, new credit, and credit mix. For ODSP recipients, realistic credit score expectations might range. While an excellent score (750+) will always yield the best rates, many successful ODSP applicants secure loans with fair (650-699) or even poor (below 600) credit scores.

The key is to understand your score and proactively address any issues. Even a 'bad' score isn't a dead end. Lenders specializing in non-traditional financing often look beyond the score to your current income stability and willingness to pay. Knowing your score allows you to identify potential red flags and prepare explanations for any past missteps. It's your financial report card, but it's one you can improve.

Income Stability & Supplementary Sources: Building a Stronger Financial Profile

As we've established, ODSP provides a stable income. However, combining it with other legitimate income sources can significantly strengthen your application, improving your perceived ability to repay the loan. This might include:

- Canada Child Benefit (CCB): If you have dependent children, CCB payments are a consistent, non-taxable income source that lenders will recognize.

- Part-time Employment: Even a few hours a week can demonstrate an ability to earn additional income and manage work alongside your disability.

- Self-Employment Income: If you engage in any small business activities, properly documented income can be added. For more on how self-employment income can help secure a car loan, see our guide on Approval Secrets: Navigating the Best Used Car Finance Options for Ontario’s Self-Employed.

- Spousal Income: If you have a spouse or common-law partner, their income can be included on a joint application, significantly boosting your combined financial profile.

- Other Benefits: Any other government benefits or pensions, such as CPPD (Canada Pension Plan Disability), also contribute to your total verifiable income.

Proper documentation for all income sources is crucial. Lenders will want to see bank statements, pay stubs, or benefit statements that clearly show consistent deposits. The more comprehensive your financial picture, the better your chances.

Debt-to-Income Ratio: Your Invisible Approval Hurdle

Your Debt-to-Income (DTI) ratio is a critical metric that lenders use to assess your capacity to take on new debt. It's calculated by dividing your total monthly debt payments (including rent/mortgage, credit card minimums, existing loan payments) by your gross monthly income. For example, if your total monthly debt payments are $1,000 and your gross monthly income (ODSP + any supplementary income) is $2,500, your DTI is 40% ($1,000 / $2,500 = 0.40). Lenders typically prefer a DTI below 40-45%, though some specialized lenders may go higher depending on other factors.

Strategies to improve your DTI include: paying down existing high-interest debts, consolidating smaller debts into one manageable payment, or even closing unused credit accounts (though be cautious, as this can sometimes temporarily lower your score). Demonstrating a proactive approach to managing your current debts shows financial responsibility and improves your appeal to lenders.

The Down Payment Advantage: Boosting Your Odds and Lowering Costs

A down payment is a powerful tool in your car loan application. It represents the portion of the car's price you pay upfront, reducing the amount you need to borrow. From a lender's perspective, a down payment signals commitment and significantly reduces their risk. The less they have to lend, the lower their exposure. Even a small down payment, say 5% or 10% of the vehicle's price, can make a significant difference in approval odds and, crucially, can lead to lower interest rates over the life of the loan.

Strategies for saving a down payment include setting aside a small amount from each ODSP payment, selling unused items, or utilizing tax refunds. While zero-down loans are available, they often come with higher interest rates and longer loan terms, meaning you pay more over time. Prioritizing even a modest down payment can be a smart long-term financial move.

The Co-Signer Conundrum: A Double-Edged Sword for ODSP Borrowers

A co-signer can be a valuable asset for ODSP borrowers, particularly if you have a limited or challenged credit history. A co-signer, typically a trusted family member or friend with good credit, essentially guarantees the loan, promising to make payments if you default. This reduces the lender's risk and can help you secure approval or better interest rates.

However, it's a double-edged sword. The co-signer assumes full legal responsibility for the debt. If you miss payments, their credit score will be negatively impacted, and they will be pursued for repayment. This can strain relationships if not handled with extreme care and transparent communication. Approach this option strategically: ensure both parties fully understand the responsibilities, have a clear plan for repayment, and only consider it if you are confident in your ability to meet the monthly obligations. It's a serious commitment for everyone involved.

To further clarify the factors lenders weigh, here's a table summarizing key elements of your application:

| Factor | Description | Impact on Approval | Tips for ODSP Applicants |

|---|---|---|---|

| Income Stability | Consistent, verifiable income from ODSP and supplementary sources. | High: Predictable income is crucial for repayment confidence. | Highlight ODSP's guaranteed nature. Document all other income (CCB, part-time). |

| Credit Score | A numerical representation of your creditworthiness. | Medium to High: Better scores mean better rates, but specialized lenders can work with lower scores. | Check your report, dispute errors. Focus on consistent payments on existing debts. |

| Debt-to-Income Ratio (DTI) | Percentage of gross income used for debt payments. | High: Lower DTI (ideally <40%) shows capacity for new debt. | Pay down existing debts. Avoid taking on new credit before applying. |

| Down Payment | Upfront cash payment towards the vehicle purchase. | Medium: Reduces loan amount and lender risk. Can improve rates. | Even 5-10% can make a difference. Save consistently. |

| Co-Signer | Another person guaranteeing the loan. | High (if needed): Can unlock approval or better rates with challenged credit. | Choose carefully. Ensure full understanding of responsibilities for both parties. |

| Employment History | Record of stable employment (if applicable). | Medium (if applicable): Shows ability to earn, but ODSP is strong on its own. | If employed part-time, emphasize consistency. If not, focus solely on ODSP stability. |

Chapter 3: Your Strategic Playbook – Crafting an Irresistible Application in Ontario

Pre-Approval: Your Secret Weapon for Confidence and Negotiation

One of the smartest moves you can make is getting pre-approved for a car loan before you even step foot on a dealership lot. Why? Pre-approval is essentially a conditional offer from a lender, telling you how much they're willing to lend you and at what interest rate, based on a preliminary review of your finances. This empowers you in several significant ways.

Firstly, it clarifies your budget. You'll know exactly what you can afford, preventing you from falling in love with a car outside your financial reach. Secondly, and perhaps most importantly, it transforms you into a powerful negotiator. With pre-approved financing in hand, you approach the dealership like a cash buyer. Their focus shifts from selling you a loan to selling you a car, often leading to better vehicle prices and less pressure in the finance office. Many lenders offer pre-approval with only a "soft inquiry" on your credit, which doesn't impact your score. It's a low-risk, high-reward strategy for any car buyer in Ontario.

Gathering Your Financial Arsenal: Documents You'll Need

Being prepared with all necessary documentation is a hallmark of a responsible borrower and significantly speeds up the application process. Lenders appreciate efficiency and thoroughness. Here's a comprehensive checklist of what you'll likely need:

- Government-Issued ID: Valid Canadian driver's license (essential for driving, of course!) or other photo ID.

- ODSP Statements: Recent statements (typically 3 months) showing consistent payments.

- Bank Statements: Recent statements (3-6 months) from your primary bank account, demonstrating income deposits and spending habits. For more on how important these are, check out our guide on Bank Statements: The Only Resume Your Car Loan Needs. Drive, Alberta!.

- Proof of Residency: Utility bills (hydro, gas, internet) from the last 30-60 days with your current address (e.g., from Toronto, Ottawa, or any Ontario city).

- Proof of Income (Supplementary): If you have other income sources, gather pay stubs, employment letters, or tax returns.

- Credit Report: While lenders will pull their own, having reviewed yours beforehand helps you understand and explain any discrepancies.

- References: Some lenders, especially those for challenged credit, may ask for a few personal references.

Having these documents organized and ready shows a high level of responsibility and commitment, making your application much smoother.

Budgeting for Reality: Beyond the Monthly Payment

Securing the loan is just the first step; sustainable car ownership is the true goal. Too often, buyers focus solely on the monthly car loan payment, overlooking the myriad of other costs associated with owning a vehicle in Ontario. A robust budget is essential for long-term success. Consider these critical expenses:

- Car Insurance: Ontario has some of the highest auto insurance rates in Canada. This can be a significant monthly expense, so get quotes early.

- Fuel: Gas prices fluctuate. Estimate your weekly or monthly fuel costs based on your driving habits.

- Maintenance: Regular oil changes, tire rotations, brake checks, and other preventative maintenance are crucial to prolonging your car's life and preventing costly breakdowns.

- Unexpected Repairs: Even reliable cars need repairs sometimes. It's wise to have a small emergency fund dedicated to these unforeseen expenses.

- Registration & Licensing: Annual fees to keep your vehicle legal on Ontario roads.

- Parking: If you live in an urban centre like Toronto or Mississauga, parking fees can add up.

Create a detailed spreadsheet or use a budgeting app to account for all these costs. This realistic financial planning will not only help you stay on top of your payments but also demonstrate to lenders that you've thought through the full commitment of car ownership.

Chapter 4: Navigating Ontario's Lending Landscape – Where to Find ODSP-Friendly Car Loans

Dealership Financing: The Convenience Factor and Its Caveats

Many dealerships across Ontario, especially in larger cities like Mississauga, Hamilton, and London, offer convenient in-house financing or work with a network of external lenders. The pros include a one-stop-shop experience: you choose your car and arrange financing all in one place. Dealerships often have access to special manufacturer incentives or can tailor packages to specific credit situations. They may also have more experience dealing with diverse income types, including ODSP, particularly those that advertise "all credit approved" or "bad credit car loans."

However, there are caveats. Dealerships might push their preferred lenders, which may not always offer you the best rates. Their financing department often focuses on maximizing profit, so be prepared to negotiate fiercely on both the car price and the loan terms. While convenient, it's essential to compare their offers with your pre-approval to ensure you're getting the most competitive rate possible.

Banks vs. Credit Unions: Traditional Lenders and Community Support

When considering traditional lenders, you'll generally look at banks and credit unions. Large banks (like RBC, TD, BMO, Scotiabank, CIBC) can be more conservative in their lending practices, often preferring applicants with strong credit scores and traditional employment income. While not impossible, securing a direct car loan from a major bank solely on ODSP may require a very strong credit history or a substantial down payment.

Credit unions, on the other hand, often adopt a more community-focused approach. They are member-owned and can sometimes be more flexible and understanding of individual circumstances, including non-traditional income sources like ODSP. Building a relationship with a local credit union in your Ontario community (e.g., in Windsor, Kingston, or Sudbury) can be beneficial, as they might be more willing to work with you, especially if you're an existing member in good standing. Their rates can also be very competitive.

Specialized Lenders: Your Best Bet for Non-Traditional Income

For many ODSP recipients, specialized lenders are often the most viable and effective path to car loan approval. These lenders operate in the 'subprime' or 'non-traditional' financing market, meaning they cater to individuals with less-than-perfect credit, limited credit history, or non-traditional income sources like ODSP. They have specific underwriting processes designed to evaluate these applications, making them much more likely to understand and approve your situation.

Characteristics of reputable specialized lenders in Ontario include a transparent application process, clear terms and conditions, and a focus on your current ability to pay rather than solely on past credit issues. While interest rates may be higher than prime rates, they are a crucial gateway to vehicle ownership and, more importantly, an opportunity to rebuild your credit. For those navigating challenging credit situations with disability income, this type of lender can be a game-changer. You might find further insights in our article Disability Income? Bad Credit? Your Car Loan Just Got Its Green Light, Toronto.

Online Car Loan Platforms: Speed, Variety, and Cautionary Tales

The digital age has brought numerous online car loan platforms to the forefront, offering speed, convenience, and access to a wide network of lenders from anywhere in Ontario. You can apply from the comfort of your home, often receiving pre-approval in minutes or hours. These platforms can be particularly useful for ODSP recipients as they often partner with specialized lenders who are accustomed to non-traditional income types.

However, caution is advised. While many are legitimate, it's essential to verify the credibility of online platforms. Look for secure websites (HTTPS), positive customer reviews, and clear contact information. Be wary of sites that guarantee approval without any financial review or demand upfront fees. Reputable online platforms will connect you with actual lenders and dealerships, not act as a lender themselves. Use them to explore options, but always do your due diligence before sharing personal financial information.

Finding 'ODSP-Friendly' Dealerships & Brokers in Major Ontario Cities

How do you find these specific dealerships or brokers that understand and cater to ODSP clients? Start by searching online for "ODSP car loans Ontario," "bad credit car loans Toronto," "disability income auto financing Ottawa," or similar terms for your local city (e.g., London, Hamilton, Windsor). Look for dealerships that explicitly mention working with all credit types or specialize in financing for individuals on government benefits.

When you contact them, be upfront about your income source. Ask direct questions: "Do you have experience financing clients on ODSP?" "Which lenders do you work with that understand government benefits as income?" A truly ODSP-friendly dealership or broker will be knowledgeable, empathetic, and transparent about your options, rather than dismissing you or making vague promises. Red flags include high-pressure sales tactics, demands for excessive upfront fees, or an unwillingness to explain terms clearly.

Chapter 5: Beyond the Sticker Price – Unmasking the True Costs of Car Ownership in Ontario

Understanding Interest Rates: What to Expect and How to Improve Them

For ODSP recipients, especially those with challenged credit, interest rates on car loans might be higher than the prime rates offered to borrowers with excellent credit. This is because lenders perceive a higher risk associated with non-traditional income or past credit issues. While prime rates might be in the single digits, you might see rates ranging from 10% to 25% or even higher, depending on your credit profile and the lender.

What constitutes a 'good' vs. 'bad' rate in your situation? A 'good' rate is the lowest you can realistically achieve given your financial circumstances. A 'bad' rate is one that is excessively high, making the loan unsustainable. Strategies to secure the lowest possible rate include: offering a larger down payment, choosing a shorter loan term (which increases monthly payments but reduces total interest paid), improving your credit score before applying, or securing a co-signer. Always compare multiple offers to ensure you're getting a competitive rate for your situation.

The Hidden Costs: Fees, Warranties, and Extras to Watch Out For

The sticker price of a car is rarely the final price. Beyond the vehicle's cost and interest, a variety of fees and extras can inflate your loan total. Be vigilant and understand what each charge entails:

- Administration Fees: Dealerships often charge these for processing paperwork. They can range from a few hundred dollars to over a thousand. These are often negotiable.

- PPSA (Personal Property Security Act) Registration: A provincial fee to register the lender's interest in the vehicle. This is typically non-negotiable and relatively small.

- Lien Registration Fees: Similar to PPSA, ensures the lender is protected.

- Extended Warranties: Offer coverage beyond the factory warranty. While some can be valuable, many are overpriced or cover items already included. Research thoroughly before buying.

- Protection Packages: Such as rust proofing, paint protection, fabric protection. Often high-profit items for dealerships; consider if you truly need them and if the price is fair.

- Gap Insurance: Covers the difference between what your car is worth and what you owe if it's stolen or totalled. This can be a wise investment, especially for new cars or those with high loan-to-value ratios.

Always ask for a full breakdown of all fees and charges. Don't be afraid to negotiate or decline optional add-ons that don't provide genuine value for your situation. Knowledge is power here.

Ontario Car Insurance: A Major Budgetary Consideration

This cannot be stressed enough: car insurance costs in Ontario are among the highest in Canada. For an ODSP recipient, budgeting for insurance is paramount and must be done *before* finalizing your car purchase. Factors affecting your rates include your driving history, the type of vehicle, where you live in Ontario (e.g., Brampton and Toronto often have higher rates than rural areas), your age, and the coverage you choose.

Tips for finding affordable coverage:

- Shop Around: Get at least three to five quotes from different insurance providers.

- Choose Your Vehicle Wisely: Older, less expensive, and commonly available models often have lower insurance premiums. Sports cars or luxury vehicles will be significantly more expensive.

- Increase Deductibles: A higher deductible (the amount you pay out-of-pocket before insurance kicks in) will lower your monthly premium.

- Bundle Policies: If you have home or tenant insurance, bundling it with your auto insurance can often lead to discounts.

- Ask About Discounts: Many insurers offer discounts for good driving records, winter tires, security systems, or being a member of certain associations.

Do not underestimate this cost. It can easily add hundreds of dollars to your monthly budget.

New vs. Used: The ODSP Perspective on Vehicle Choice

The decision between a new and used car is a significant one, particularly when managing finances on ODSP. Each option has distinct pros and cons:

New Car Pros:

- Reliability: Brand new, typically comes with a comprehensive manufacturer's warranty, reducing immediate repair concerns.

- Latest Features: Modern safety features, fuel efficiency, and technology.

- Lower Interest Rates: Sometimes, manufacturers offer promotional low-interest financing for new vehicles to qualified buyers.

New Car Cons:

- Rapid Depreciation: New cars lose significant value the moment they're driven off the lot.

- Higher Purchase Price: Generally more expensive, leading to larger loans and payments.

- Higher Insurance: Often more costly to insure due to higher replacement value.

Used Car Pros:

- Lower Purchase Price: Significantly more affordable, reducing the loan amount.

- Slower Depreciation: Most of the depreciation has already occurred.

- Lower Insurance: Generally cheaper to insure.

- Wider Selection: More options within a given budget.

Used Car Cons:

- Potential for Repairs: Older vehicles may require more maintenance or unexpected repairs.

- Limited Warranty: Manufacturer warranty may be expired or limited.

- Higher Interest Rates: Sometimes, used car loans carry slightly higher rates, especially for older models.

For most ODSP recipients, a reliable used car often presents the most financially sound choice. It allows for a more manageable loan size and lower overall ownership costs, better aligning with a fixed income budget. Focus on well-maintained, reputable used models with a proven track record for reliability.

Here's a comparative chart to help visualize the long-term costs of new versus used cars for budgeting purposes on ODSP in Ontario:

| Cost Factor | New Car (Example) | Used Car (Example) | Impact for ODSP Budget |

|---|---|---|---|

| Initial Purchase Price | $30,000+ | $10,000 - $20,000 | Significant: Lower purchase price directly translates to a smaller loan and lower monthly payments. |

| Depreciation (Year 1) | 15-25% of value | 5-10% of value | Moderate: Less loss of value means better equity and easier resale/trade-in if needed. |

| Car Insurance (Annual) | $2,500 - $4,000+ | $1,800 - $3,000+ | High: A major ongoing expense in Ontario. Used cars generally have lower premiums. |

| Warranty Coverage | 3-5 years full bumper-to-bumper | Limited or expired; often dealer-backed for short term | Variable: New car warranty offers peace of mind. For used, factor in potential repair costs or consider extended warranty (carefully). |

| Maintenance Costs (Annual Avg.) | Low (under warranty) | Moderate to High (depending on age/condition) | Crucial: Older cars may require more frequent or costly repairs. Budget for an emergency fund. |

| Interest Rate Potential | Lower (0-10% for qualified) | Higher (5-25%+ for challenged credit) | Important: Even with potentially higher rates, the lower principal of a used car loan can mean lower total interest paid. |

| Fuel Efficiency | Generally better (newer tech) | Can vary widely (older tech, condition) | Considerable: Fuel is a weekly expense. More efficient cars save money over time. |

Chapter 6: Driving Forward – Managing Your Loan and Building a Brighter Financial Future

Mastering Your Monthly Payments: The Cornerstone of Credit Building

Once you've secured your car loan, the most critical step to building a brighter financial future is consistent, on-time monthly payments. This is the cornerstone of credit building. Every payment you make on time is reported to credit bureaus (Equifax and TransUnion), progressively improving your credit score. A strong payment history demonstrates reliability and responsibility to all future lenders, opening doors to better rates on future loans (e.g., for a home, or even another car) and credit cards.

Strategies for mastering your payments include: setting up automatic payments from your bank account to ensure you never miss a due date, scheduling reminders on your phone or calendar, and making bi-weekly payments if your budget allows (this can subtly reduce interest over the loan term). Treat your car payment as a top priority. Your financial independence starts here.

Refinancing Your ODSP Car Loan: When and Why it Makes Sense

Securing your initial car loan on ODSP might involve a higher interest rate, especially if you had challenged credit. However, this isn't necessarily a permanent situation. After a year or two of diligent, on-time payments, you might qualify for better interest rates through refinancing. Refinancing involves taking out a new loan to pay off your existing car loan, ideally with a lower interest rate, a shorter term, or both.

When does it make sense? If your credit score has improved significantly, if interest rates have dropped, or if you now have a stronger financial profile (e.g., through supplementary income or a larger emergency fund), refinancing can save you thousands of dollars over the life of your loan. You'll typically need to have made at least 12-24 consistent payments and have a car that hasn't depreciated excessively. Explore this option regularly; it's a powerful tool for optimizing your financial health.

Protecting Your Investment: Maintenance, Warranties, and Emergency Funds

Your car is a significant investment, and protecting it goes beyond just making loan payments. Regular maintenance is crucial to prolonging its life, ensuring its safety, and preventing costly breakdowns. Follow the manufacturer's recommended maintenance schedule for oil changes, tire rotations, fluid checks, and brake inspections. Neglecting maintenance is a false economy that almost always leads to more expensive repairs down the line.

Regarding warranties, understand what your vehicle comes with. For used cars, a reputable dealer might offer a short-term warranty. Carefully evaluate extended warranties – some can be valuable for high-risk vehicles or if you plan to keep the car long-term, but many are overpriced. Finally, the importance of building a small emergency fund cannot be overstated. Unexpected repairs are a reality of car ownership. Having $500-$1,000 set aside specifically for car emergencies can prevent financial stress and protect your ability to make your loan payments.

Your Next Steps to Approval: Charting Your Course in Ontario

Securing a car loan on ODSP in Ontario is not just a possibility; it's an achievable goal with the right knowledge and strategy. This article has equipped you with the tools to navigate the lending landscape, understand the true costs, and build a strong financial foundation. The journey to vehicle ownership requires preparation, persistence, and a clear understanding of your financial situation, but the independence and opportunities it provides are immeasurable. Take these actionable steps, empower yourself with information, and drive towards the independence you deserve.