Vancouver: Your Private Car Deal, Our Bad Credit Cash. Zero Bank Drama.

Table of Contents

- Key Takeaways

- Why Vancouver's Private Car Market is Your Secret Weapon (Even with Imperfect Credit)

- The Allure of Private Sales: Saving Money in British Columbia's Hot Market

- Dispelling the Myth: You Don't Need Perfect Credit for a Private Deal

- Decoding 'Bad Credit': What Lenders *Really* See (and How to Address It)

- Beyond the Score: Understanding Your Credit Report's True Narrative

- The Pillars of Approval: Income, Stability, and Debt-to-Income Ratios

- Dispelling Common Bad Credit Myths: You're Not Alone, and You Have Options

- The 'Zero Bank Drama' Revolution: Specialized Lenders for Private Sales in Canada

- Why Traditional Banks Often Say 'No' to Private Sales (Especially with Bad Credit)

- How Non-Traditional Lenders Bridge the Gap: Flexibility and Understanding

- The Application Process: Simpler and Faster Than You Think

- Navigating the Vancouver Private Car Scene: From Online Listings to Ownership

- Where to Find Your Next Car: Local Platforms in British Columbia's Lower Mainland

- Essential Questions to Ask the Seller Before You Even See the Car

- Understanding British Columbia's Vehicle Transfer Regulations and Sales Tax

- Your Approval Blueprint: What You *Really* Need to Secure Your Loan

- The Documentation Checklist: Proof of Income, Residency, and Identification

- The Power of a Down Payment: Boosting Your Approval Odds and Lowering Costs

- Co-Signers: When They Help, When They Don't, and How to Choose Wisely

- Beyond the Sticker Price: Unmasking the True Cost of Your Private Car Loan

- Interest Rates for Bad Credit: What's Realistic and How to Compare

- Understanding Loan Terms and Amortization: Your Monthly Payment Explained

- Hidden Fees and Charges to Watch Out For: Protecting Your Wallet

- Vehicle Vetting for Value: Choosing the Right Car for Your Loan (and Wallet)

- Age and Mileage Considerations for Private Sale Financing in Vancouver

- Popular Vehicle Types That Are Easier to Finance (and Maintain)

- Avoiding Problematic Vehicles: Red Flags to Watch For

- Building Bridges, Not Walls: How This Process Can Improve Your Credit

- The Power of On-Time Payments: Your Path to a Stronger Credit Score

- Rebuilding Your Credit Profile Step-by-Step: Beyond the Car Loan

- Refinancing Opportunities Down the Line: Lowering Your Rates as Your Credit Improves

- Expanding Your Horizons: How These Principles Apply Across Canada (Vancouver as the Blueprint)

- Brief Comparisons: Financing Private Sales in Toronto, Calgary, and Montreal

- Provincial Variations: Vehicle Registration, Sales Tax, and Insurance in Canada

- Your Next Steps to Approval: Driving Away with Confidence in Vancouver

- Recap of Your Journey: From Bad Credit Doubts to Private Car Ownership

- Clear, Actionable Final Advice: Start Your Application Today

- Frequently Asked Questions About How to Finance a Private Car Sale with Bad Credit in Vancouver

Navigating the bustling streets of Vancouver, from the vibrant downtown core to the serene landscapes of Stanley Park, often requires the freedom and convenience of your own vehicle. But what if your credit history isn't as pristine as the mountain air, and the thought of traditional bank loans feels like scaling a financial Everest? For many Vancouverites, the dream of car ownership hits a roadblock when faced with bad credit, especially when eyeing the cost-saving potential of a private car sale.

At SkipCarDealer.com, we understand this challenge. We know that life happens, and a less-than-perfect credit score shouldn't be a permanent barrier to securing reliable transportation. In fact, we see it as an opportunity – an opportunity to connect you with a private car deal that offers incredible value, powered by our specialized bad credit financing solutions. Forget the "zero bank drama" because we operate outside the rigid, often unhelpful, constraints of traditional financial institutions.

This comprehensive guide is designed to demystify the process of financing a private car sale in Vancouver, even with bad credit. We'll show you how to unlock the hidden gems of the private market, understand what lenders truly look for, and walk you through a streamlined approval process that prioritizes your future, not just your past. Get ready to discover how you can drive away in your next vehicle, all while rebuilding your financial confidence.

Key Takeaways

- Bad Credit is NOT a Barrier: Traditional banks may hesitate, but specialized lenders are ready to finance private car sales for individuals with imperfect credit histories in Vancouver and across Canada.

- Private Sales Offer Superior Value: Discover significant cost savings and a wider selection of vehicles compared to dealerships, especially in British Columbia's competitive market.

- Specialized Lenders Are Your Solution: Bypass the "bank drama" with flexible, understanding financing options tailored to your unique financial situation.

- Your Credit Can Improve: Responsible management of a private car loan can be a powerful tool for rebuilding and strengthening your credit score over time.

- Knowledge is Power: Learn how to spot genuine private deals, understand provincial regulations, and what documentation you'll need for a smooth transaction and approval.

Why Vancouver's Private Car Market is Your Secret Weapon (Even with Imperfect Credit)

Vancouver, with its stunning natural beauty and thriving economy, also has a reputation for being an expensive city. This extends to vehicle purchases, where dealership markups can add significant costs. This is precisely why the private car market becomes an invaluable resource for savvy buyers, particularly those navigating bad credit. By cutting out the middleman, you gain access to more competitive pricing and a broader, often more unique, selection of vehicles that might not be found on a dealership lot.

The Allure of Private Sales: Saving Money in British Columbia's Hot Market

In vibrant urban centres like Vancouver, Burnaby, and Richmond, the demand for reliable transportation is consistently high. Dealerships capitalize on this, often pricing vehicles to cover their overheads, sales commissions, and profit margins. Private sellers, on the other hand, typically just want to sell their car quickly and fairly, often leading to more negotiable prices. This difference can translate into substantial savings, making private sales an attractive option when every dollar counts, especially when you're managing a budget with bad credit.

Consider this comparison:

| Feature | Private Car Sale | Dealership Purchase |

|---|---|---|

| Price Negotiation | Often highly flexible, direct with seller. | Less flexibility, structured pricing, sales tactics. |

| Selection | Diverse, unique, individual owner preferences. | Limited to current inventory, specific brands/models. |

| "Hidden" Fees | Minimal (sales tax, registration, perhaps a lien check fee). | Documentation fees, administrative charges, detailing fees, extended warranty push. |

| Time Commitment | Can be quicker if you find the right car, direct communication. | Can be lengthy, involving multiple sales reps, finance managers. |

| Financing Options (Bad Credit) | Requires specialized lenders like SkipCarDealer.com. | Some dealerships offer bad credit, but often with higher markups or limited options. |

Dispelling the Myth: You Don't Need Perfect Credit for a Private Deal

A common misconception is that if you have bad credit, your only option for a car is through a "buy here, pay here" lot or a dealership that specializes in subprime loans, often at exorbitant rates or with limited vehicle choices. This simply isn't true, especially when considering private sales. While traditional banks are indeed hesitant to finance private transactions for those with imperfect credit, a new wave of specialized lenders has emerged to fill this void. These lenders look beyond just your credit score, focusing on your current ability to pay and your overall financial stability. For more on this, check out our guide on No Credit? Great. We're Not Your Bank.

PRO TIP: How to Spot a Genuine Private Deal vs. a 'Curb-Sider' in Vancouver

The Vancouver private market, like any other, has its pitfalls. A "curb-sider" is an unlicensed dealer posing as a private seller to avoid regulations and taxes, often selling vehicles with undisclosed issues. To protect yourself, always insist on meeting the seller at their registered home address, check that the name on the registration matches their ID, and be wary of sellers who refuse a pre-purchase inspection or are overly pushy. A legitimate private seller will be transparent and cooperative.

Decoding 'Bad Credit': What Lenders *Really* See (and How to Address It)

When you hear "bad credit," you might immediately think of a low three-digit number. While your credit score is a snapshot, it's far from the whole story. Specialized lenders, particularly those willing to finance private car sales with bad credit, delve much deeper. They want to understand the narrative behind your score, assessing your overall financial health and your potential for responsible repayment.

Beyond the Score: Understanding Your Credit Report's True Narrative

Your credit report is a detailed history of your financial behaviour. Lenders scrutinize several key components:

- Payment History: This is paramount. Late payments, collections, and bankruptcies significantly impact your score. However, a recent history of on-time payments, even after past issues, can show a positive trend.

- Debt Utilization: How much of your available credit are you using? High utilization (e.g., maxed-out credit cards) suggests financial strain.

- Length of Credit History: A longer history with good behaviour is generally better.

- Credit Mix: A healthy mix of different credit types (e.g., a credit card and a small loan) can be positive.

- New Credit Inquiries: Too many recent applications can suggest desperation or higher risk.

Specialized lenders understand that life events – job loss, illness, divorce – can lead to credit challenges. They are more interested in understanding *why* your credit suffered and what steps you're taking now to improve your situation.

The Pillars of Approval: Income, Stability, and Debt-to-Income Ratios

Beyond your credit score, specialized lenders prioritize your current ability to make payments. This means they focus heavily on:

- Income: Do you have a steady, verifiable source of income? This doesn't always mean a traditional salary. Income from employment insurance (EI), child tax benefits, or pensions can also be considered. For British Columbia residents, specifically, you might find our article on British Columbia EI? Your Car Loan Just Called 'Shotgun'. to be helpful.

- Stability: How long have you been at your current job and residence? Stability signals reliability. Longer tenure at both suggests a lower risk of sudden financial changes.

- Debt-to-Income (DTI) Ratio: This is a crucial metric. It compares your total monthly debt payments to your gross monthly income. Lenders want to see that you have enough disposable income left after your existing obligations to comfortably afford a car payment. A lower DTI ratio is always more favourable.

Dispelling Common Bad Credit Myths: You're Not Alone, and You Have Options

Many individuals with bad credit feel isolated and believe their options are severely limited. This simply isn't the case. Here are some common myths we love to debunk:

- Myth: "I'll never get approved for a car loan with bad credit."

Reality: Specialized lenders exist specifically for this purpose. They understand and cater to unique financial situations. - Myth: "Private sales are only for cash buyers."

Reality: With the right financing partner, you can secure a loan for a private sale just as easily as for a dealership purchase. - Myth: "My credit is too far gone to ever recover."

Reality: Every on-time payment you make on a new loan contributes positively to your credit history, acting as a stepping stone to better financial health.

Don't let past financial hurdles define your future. There are always options, and at SkipCarDealer.com, we specialize in helping Vancouver residents find them. You're not alone in this journey, and your car loan is within reach.

The 'Zero Bank Drama' Revolution: Specialized Lenders for Private Sales in Canada

The traditional banking system, with its stringent criteria and bureaucratic processes, often feels like an impenetrable fortress when you have bad credit, especially for a private car sale. This is where specialized lenders, like SkipCarDealer.com, step in, offering a refreshing, customer-centric approach that cuts through the "bank drama."

Why Traditional Banks Often Say 'No' to Private Sales (Especially with Bad Credit)

Traditional banks operate on a model of minimizing risk. When it comes to financing a private car sale, several factors make them hesitant:

- Lack of Collateral Control: With a private sale, the vehicle's condition isn't typically vetted by the bank's preferred appraisers or mechanics, and there's no dealership to guarantee the sale or the vehicle's history.

- Increased Fraud Risk: Private sales can be more susceptible to fraud (e.g., undisclosed liens, curb-siding), which banks are eager to avoid.

- Higher Administrative Costs: Processing individual private sale loans often involves more manual work and verification than bulk financing deals with established dealerships.

- Credit Score Dependency: Banks are heavily reliant on credit scores and established credit histories. Bad credit applicants fall outside their preferred risk profile, making them an automatic "no" for anything perceived as higher risk, like a private sale.

Their business model simply isn't built to navigate the nuances and perceived risks of private transactions for applicants who don't fit their perfect credit mold.

How Non-Traditional Lenders Bridge the Gap: Flexibility and Understanding

Specialized lenders, on the other hand, have built their entire business around bridging this gap. They understand that a credit score is just one piece of a larger puzzle. Their approach is characterized by:

- Holistic Assessment: They look at your overall financial picture, including your income, employment stability, living situation, and even the circumstances that led to your bad credit. They're more interested in your present capacity to pay.

- Tailored Solutions: Instead of a one-size-fits-all approach, they work to find a loan solution that fits your specific needs and budget.

- Efficiency: Their processes are often streamlined and technology-driven, allowing for faster approvals and funding.

- Canada-Wide Reach: Whether you're in Vancouver, British Columbia; Calgary, Alberta; Toronto, Ontario; Montreal, Quebec; or even Halifax, Nova Scotia, these lenders have systems in place to facilitate private car sales across the country.

This flexibility and understanding are what truly set them apart, transforming what seems like an impossible situation into a real possibility. For those who feel "denied everywhere," remember that specialized lenders see a challenge, not a dead end. In fact, we revel in it, as our article Why 'Denied Everywhere' Is Our Favourite Challenge, Vancouver. highlights.

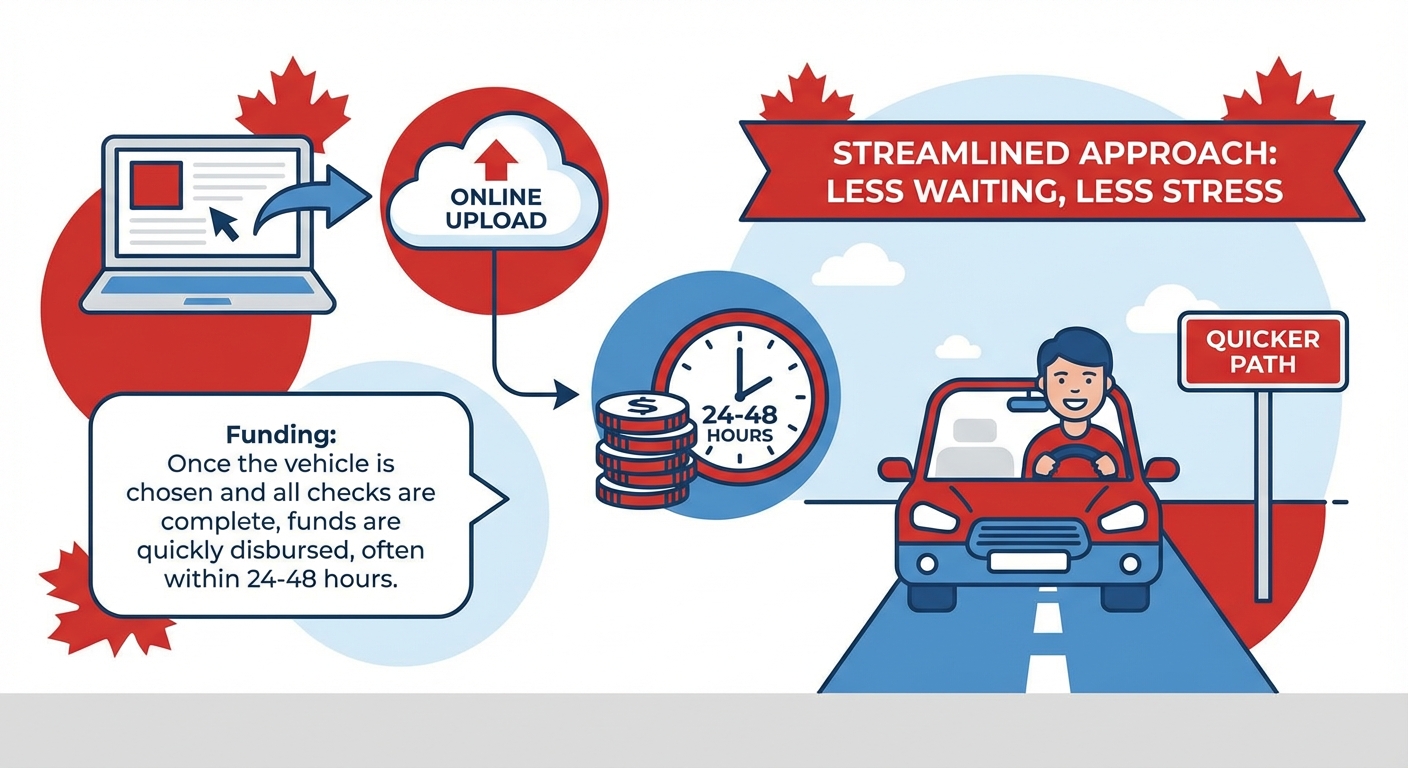

The Application Process: Simpler and Faster Than You Think

Forget the stacks of paperwork and endless appointments associated with traditional bank loans. The application process with specialized lenders is designed for your convenience:

- Online Application: Start with a simple, secure online form that takes minutes to complete.

- Quick Review: Your application is quickly reviewed by a team that specializes in bad credit financing.

- Vehicle Search: Once pre-approved, you can confidently search for your ideal private sale vehicle.

- Documentation: Provide necessary documents (proof of income, ID, etc.) usually via secure online upload.

- Funding: Once the vehicle is chosen and all checks are complete, funds are quickly disbursed, often within 24-48 hours.

This streamlined approach means less waiting, less stress, and a quicker path to getting behind the wheel.

– Your New Ride, Your Way: Freedom from Bank Constraints

Navigating the Vancouver Private Car Scene: From Online Listings to Ownership

Once you understand that bad credit isn't a deal-breaker for a private car loan, the next step is confidently navigating the Vancouver private car market. This requires a strategic approach, from finding the right vehicle to understanding the provincial regulations that govern private sales in British Columbia.

Where to Find Your Next Car: Local Platforms in British Columbia's Lower Mainland

The Lower Mainland offers several excellent platforms for discovering private car sales. Focusing your search on these local resources can yield better results and more convenient viewings:

- Craigslist Vancouver: A classic for private sales, offering a wide array of vehicles. Be prepared to filter thoroughly and exercise caution.

- Kijiji British Columbia: Another popular platform, similar to Craigslist, with extensive listings across Vancouver, Surrey, Langley, and other key areas.

- Facebook Marketplace: Growing rapidly, this platform allows you to search within specific geographic areas and often provides more direct access to sellers through their profiles.

- AutoTrader.ca (Private Listings): While primarily known for dealership listings, AutoTrader also features a robust section for private sellers.

When searching, be specific with your filters – price range, make, model, year, and kilometres – to narrow down options that align with both your needs and potential lender requirements.

Essential Questions to Ask the Seller Before You Even See the Car

Before you commit time and effort to an in-person viewing, a few key questions can help you pre-qualify a vehicle and seller:

- "Why are you selling the car?" (Provides insight into the seller's motivation and potential issues.)

- "How long have you owned it?" (Longer ownership often means better maintenance history.)

- "Do you have the maintenance records?" (Crucial for understanding the car's history and care.)

- "Has it ever been in an accident? Do you have a CarFax or ICBC claims history report?" (Essential for verifying the vehicle's structural integrity.)

- "Is the car still under any warranty?" (Could save you money on future repairs.)

- "Are there any mechanical issues I should be aware of?" (Allows the seller to disclose problems upfront.)

- "Is the asking price firm, or is there room for negotiation?" (Sets expectations for bargaining.)

- "When is the best time for me to see the car and have it inspected?" (Tests their willingness for a professional check.)

Understanding British Columbia's Vehicle Transfer Regulations and Sales Tax

Purchasing a private vehicle in British Columbia involves specific provincial requirements you need to be aware of:

- Provincial Sales Tax (PST): You will be required to pay 7% PST on the purchase price of the vehicle, or its average wholesale value, whichever is greater, when you register the vehicle at an ICBC office.

- Registration and Transfer: Both the buyer and seller must complete the "Transfer/Tax Form" (APV250). The seller provides the buyer with the original vehicle registration and a signed transfer form. The buyer must then register the vehicle in their name at an ICBC Autoplan broker within 10 days of the sale.

- Insurance: Mandatory basic insurance (through ICBC) is required before you can drive the car legally. Your lender will also likely require full coverage insurance to protect their investment.

- Lien Check: It is absolutely critical to perform a lien search (through services like CarFax or the Personal Property Registry) to ensure there are no outstanding debts against the vehicle. Your specialized lender will also perform their own checks, but it's good practice for you to be aware.

PRO TIP: The Non-Negotiable Importance of a Pre-Purchase Inspection (PPI) in Vancouver

Never, under any circumstances, buy a used car from a private seller without a professional pre-purchase inspection (PPI). A PPI, conducted by an independent, certified mechanic, can uncover hidden mechanical issues, accident damage, or potential problems that aren't apparent to the untrained eye. This small investment (typically $100-$200) can save you thousands in future repairs. Ask the seller if you can take the car to a mechanic of your choice (e.g., reputable shops in Kitsilano, Mount Pleasant, or Richmond). If they refuse, walk away. The PPI should cover engine, transmission, brakes, suspension, electrical systems, and a comprehensive body check.

Your Approval Blueprint: What You *Really* Need to Secure Your Loan

Securing a private car loan with bad credit isn't about magic; it's about preparation and presentation. By understanding and providing what specialized lenders need, you significantly enhance your chances of approval. This section outlines the practical steps and documentation required to build your approval blueprint.

The Documentation Checklist: Proof of Income, Residency, and Identification

To process your application efficiently, lenders will require specific documents to verify your identity, income, and stability. Having these ready can expedite the entire process:

- Proof of Income:

- Recent pay stubs (2-3 most recent)

- Bank statements (showing regular income deposits)

- Letter of employment

- If self-employed: tax assessments (T1 Generals), invoices, or bank statements.

- If on government benefits (EI, Child Tax Benefit, Disability): benefit statements or bank statements showing deposits. For Vancouver parents, your Child Tax Benefit can be an unexpected key to your car loan.

- If retired: pension statements.

- Proof of Residency:

- Utility bill (hydro, gas, internet) with your name and address

- Lease agreement or mortgage statement

- Driver's license or other government-issued ID with address

- Identification:

- Valid Canadian driver's license (mandatory for car loans)

- Secondary ID (e.g., passport, SIN card, major credit card)

- Banking Information:

- Void cheque or direct deposit form from your bank account

Ensuring these documents are current, clear, and easily accessible will make your application journey significantly smoother.

The Power of a Down Payment: Boosting Your Approval Odds and Lowering Costs

While some lenders offer zero-down options, especially for those with bad credit, making a down payment, even a small one, is highly recommended. Here's why:

- Reduces Lender Risk: A down payment shows the lender you have "skin in the game" and are committed to the purchase, making you a less risky borrower.

- Lowers Loan Amount: Less money borrowed means lower monthly payments and less interest paid over the life of the loan, saving you money in the long run.

- Improves Approval Chances: For applicants with bad credit, a down payment can be the factor that tips the scales towards approval, or secures you a better interest rate.

- Builds Equity Faster: You start with more equity in your vehicle, reducing the risk of negative equity (owing more than the car is worth).

Even a few hundred dollars can make a tangible difference in your loan terms and approval likelihood.

Co-Signers: When They Help, When They Don't, and How to Choose Wisely

A co-signer can be a powerful asset when securing a car loan with bad credit, but it's crucial to understand their role and responsibilities. A co-signer, typically someone with good credit, essentially guarantees the loan, promising to make payments if you default. This reduces the lender's risk and can help you get approved or secure a better interest rate.

- When They Help: A co-signer can be particularly beneficial if your credit is very poor, you have a limited credit history, or your income alone isn't quite strong enough for approval.

- When They Don't Help (or are not ideal): If your co-signer's credit isn't significantly better than yours, or if they already have a high debt load, their contribution may be minimal. It's also a significant ask, as their credit is on the line.

- How to Choose Wisely: Select a co-signer who has excellent credit, stable income, and a clear understanding of their commitment. This should ideally be a trusted family member or close friend with whom you have open communication. Remember, if you miss payments, it impacts both your credit scores.

Beyond the Sticker Price: Unmasking the True Cost of Your Private Car Loan

While securing a car loan with bad credit is achievable, it's vital to have a clear understanding of the overall financial commitment. Beyond the vehicle's price, several factors contribute to the true cost of your loan. Transparency is key to making an informed decision and avoiding surprises.

Interest Rates for Bad Credit: What's Realistic and How to Compare

When you have bad credit, it's realistic to expect a higher interest rate compared to someone with excellent credit. This is how lenders compensate for the increased risk. However, "higher" doesn't mean predatory. Specialized lenders aim to provide fair, manageable rates. What's realistic?

- Expectations: Rates for bad credit car loans can range anywhere from 9% to 29% APR (Annual Percentage Rate), depending on your credit profile, income, the loan term, and the vehicle itself.

- Comparison: Don't just accept the first offer. Shop around and compare offers from different specialized lenders. Look at the total cost of the loan, not just the monthly payment. Be wary of any lender promising unrealistically low rates for bad credit, as there might be hidden terms.

Here’s a simplified illustration of how interest rates impact total cost:

| Loan Amount | Interest Rate (APR) | Term (Months) | Approx. Monthly Payment | Total Interest Paid |

|---|---|---|---|---|

| $15,000 | 12% | 60 | $333 | $4,980 |

| $15,000 | 18% | 60 | $380 | $7,780 |

| $15,000 | 24% | 60 | $430 | $10,800 |

This table clearly shows that even a few percentage points difference in interest can add thousands to your total cost over the loan term.

Understanding Loan Terms and Amortization: Your Monthly Payment Explained

The loan term refers to the length of time you have to repay the loan (e.g., 36, 48, 60 months). Amortization is the process of paying off debt over time through regular payments. Here's how they impact your finances:

- Shorter Terms (e.g., 36-48 months):

- Pros: You pay less interest overall, and you own the car outright sooner.

- Cons: Monthly payments will be higher.

- Longer Terms (e.g., 60-72 months):

- Pros: Lower monthly payments, making the car more affordable on a tight budget.

- Cons: You pay significantly more interest over the life of the loan, and you build equity slower.

Choosing the right term is a balancing act between your monthly budget and the total cost of the loan. Specialized lenders can help you find a term that works for you.

Hidden Fees and Charges to Watch Out For: Protecting Your Wallet

While reputable lenders are transparent, it's always wise to be vigilant about potential fees. Always ask for a full breakdown of all costs associated with your loan. Common fees to inquire about include:

- Administrative Fees: Some lenders charge a small fee for processing the loan.

- Late Payment Penalties: Understand the fees and interest charges for missed or late payments.

- NSF (Non-Sufficient Funds) Fees: If a payment bounces, your bank and the lender may charge a fee.

- Early Payout Penalties: While less common with specialized lenders, some loans may have penalties for paying off the loan ahead of schedule. Always ask.

PRO TIP: Always Request a Detailed Loan Breakdown Before Signing

Before you commit to any loan agreement, insist on receiving a comprehensive breakdown of all costs, including the principal amount, interest rate (APR), total interest payable, loan term, all fees, and the total cost of the loan. This document, often called a loan disclosure statement, ensures full transparency and allows you to compare offers effectively. Do not sign anything you don't fully understand.

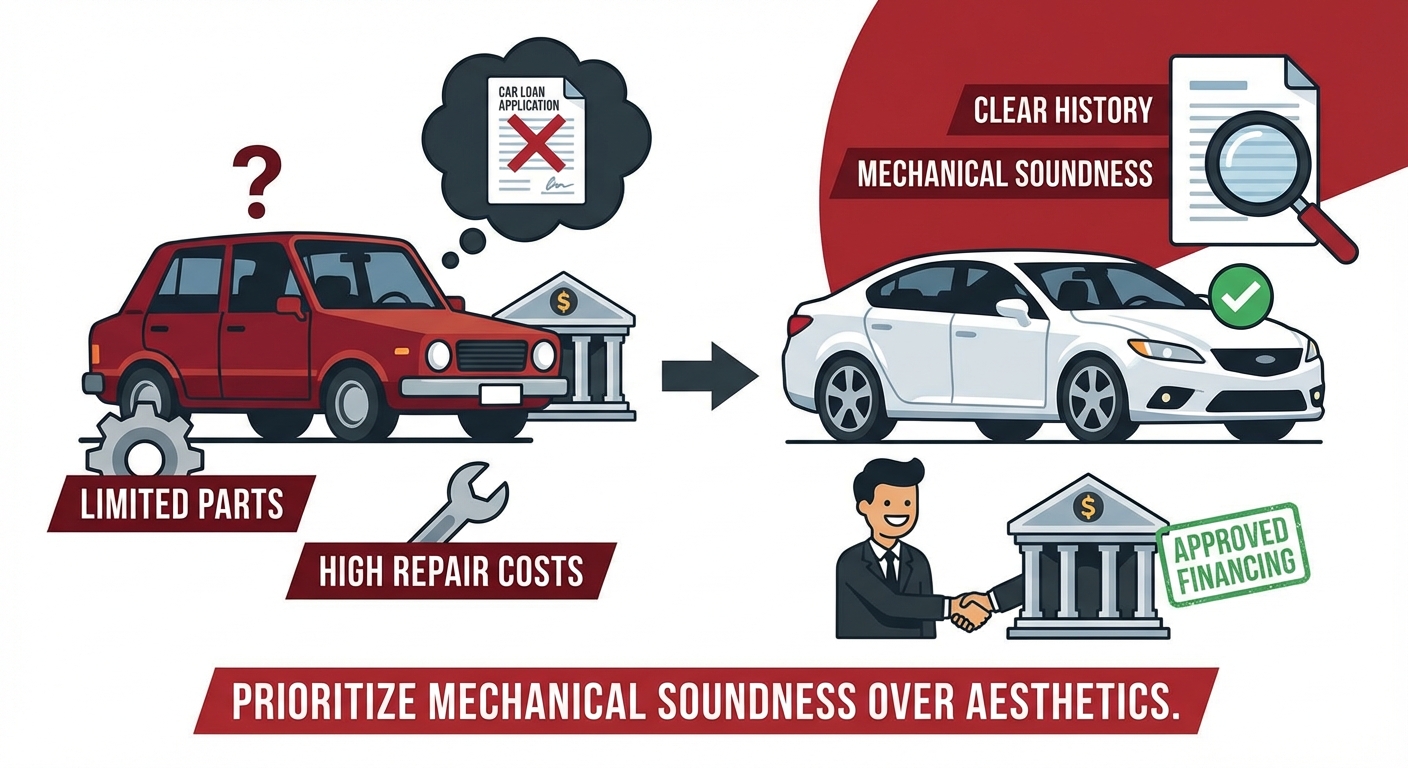

Vehicle Vetting for Value: Choosing the Right Car for Your Loan (and Wallet)

When you're financing a private car sale with bad credit, the choice of vehicle isn't just about personal preference; it's also about what lenders are willing to finance and what makes financial sense for you in the long run. Selecting a vehicle that aligns with lending criteria and offers good value is crucial for a successful and sustainable loan.

Age and Mileage Considerations for Private Sale Financing in Vancouver

Lenders have criteria for the vehicles they'll finance, largely due to depreciation and reliability concerns. Generally, for private sales and bad credit financing:

- Age: Most lenders prefer vehicles that are no older than 8-10 years. An older car poses a higher risk of mechanical failure, which could jeopardize your ability to make payments if expensive repairs are needed.

- Mileage: Similarly, lenders often have mileage caps, typically around 150,000 to 200,000 kilometres. High mileage indicates more wear and tear, and a higher likelihood of significant maintenance costs.

While these are general guidelines, some specialized lenders may be more flexible depending on the make, model, and condition of the vehicle. Focus your search in Vancouver on vehicles that fall within these parameters to increase your approval odds.

Popular Vehicle Types That Are Easier to Finance (and Maintain)

Certain vehicle types are generally easier to finance due to their proven reliability, strong resale value, and widespread availability of parts:

- Compact/Mid-Size Sedans: Models like the Honda Civic, Toyota Corolla, Mazda3, or Hyundai Elantra are often excellent choices. They are fuel-efficient, reliable, and relatively inexpensive to maintain.

- Small SUVs/Crossovers: Vehicles such as the Honda CR-V, Toyota RAV4, or Hyundai Kona offer practicality, good resale value, and are popular in British Columbia, making them good financing candidates.

- Minivans: For families, minivans like the Honda Odyssey or Toyota Sienna are robust and hold their value well.

Choosing a vehicle from a reputable brand with a track record for dependability reduces risk for both you and the lender.

Avoiding Problematic Vehicles: Red Flags to Watch For

Just as there are good choices, there are vehicles that can complicate financing and lead to headaches down the road. Be wary of:

- Salvage or Rebuilt Titles: These cars have been declared a total loss by an insurance company and then repaired. While cheaper, they carry significant risk, can be difficult to insure, and many lenders will refuse to finance them.

- Excessive Modifications: Heavily modified vehicles (e.g., custom engines, suspensions, body kits) can indicate a history of hard driving or can be difficult to assess for value and reliability. Lenders generally prefer stock vehicles.

- Signs of Neglect: Obvious rust, fluid leaks, warning lights on the dashboard, mismatched tires, or a strong odour inside the car are all red flags that the vehicle has not been well-maintained.

- Uncommon Makes/Models: While unique cars can be appealing, obscure brands or models might have limited parts availability and higher repair costs, making them less attractive to lenders.

Always prioritize a vehicle's mechanical soundness and clear history over aesthetic appeal, especially when relying on financing.

– The Smart Check: Ensuring Your Private Car is Road-Ready

Building Bridges, Not Walls: How This Process Can Improve Your Credit

Securing a private car loan with bad credit isn't just about getting a vehicle; it's a strategic move that can significantly contribute to rebuilding your financial health. Every on-time payment you make is a step towards a stronger credit profile, opening doors to better financial opportunities in the future.

The Power of On-Time Payments: Your Path to a Stronger Credit Score

Your payment history is the single most important factor influencing your credit score. When you obtain a car loan, it's reported to the major credit bureaus in Canada (Equifax and TransUnion). Each month you make your payment on time, it sends a positive signal:

- Demonstrates Responsibility: You're proving your ability to manage debt consistently.

- Builds a Positive History: A new, well-managed tradeline on your credit report offsets previous negative marks.

- Increases Your Score: Over time, consistent on-time payments will incrementally improve your credit score.

Think of your car loan as a structured savings plan for your credit score. It's an accessible way to demonstrate financial discipline, even if your past has been a bit rocky.

Rebuilding Your Credit Profile Step-by-Step: Beyond the Car Loan

While your car loan will play a significant role, consider these additional strategies to accelerate your credit rebuilding journey:

- Pay All Bills On Time: This includes utilities, credit cards, and any other loans. Consistency is key.

- Reduce Credit Card Debt: Keep your credit utilization ratio low (ideally below 30% of your available credit).

- Monitor Your Credit Report: Regularly check your credit report for errors and unauthorized activity. You're entitled to a free copy annually from each bureau.

- Avoid New Unnecessary Debt: Focus on managing your current obligations before taking on more.

- Maintain Stable Employment and Residency: Lenders appreciate stability, as it indicates a reliable income stream.

Refinancing Opportunities Down the Line: Lowering Your Rates as Your Credit Improves

One of the most exciting long-term benefits of managing your private car loan responsibly is the potential for refinancing. As your credit score improves, you become a less risky borrower to a wider range of lenders. This means you could qualify for a new loan with a lower interest rate, which would:

- Reduce Your Monthly Payments: Freeing up more cash flow.

- Lower Your Total Cost of the Loan: Saving you a significant amount in interest over the remaining term.

Refinancing is a smart financial move once you've established a solid payment history for 12-18 months. It's a tangible reward for your efforts in rebuilding your credit. For a deeper dive into this, read our comprehensive guide on Approval Secrets: How to Refinance Your Canadian Car Loan with Bad Credit.

Expanding Your Horizons: How These Principles Apply Across Canada (Vancouver as the Blueprint)

While this guide focuses on Vancouver, the principles and strategies for financing a private car sale with bad credit are broadly applicable across Canada. The challenges and solutions discussed here serve as an excellent blueprint, with only minor regional variations to consider.

Brief Comparisons: Financing Private Sales in Toronto, Calgary, and Montreal

The core concept – that specialized lenders can finance private sales for bad credit applicants – holds true in Canada's other major cities:

- Toronto, Ontario: As Canada's largest city, Toronto's private car market is vast and competitive. The same advice for vetting sellers and obtaining PPIs applies. Specialized lenders have a strong presence, understanding the diverse income streams and credit profiles common in a bustling metropolis.

- Calgary, Alberta: Calgary, known for its strong automotive culture, also offers a robust private sale market. Alberta has no provincial sales tax, which is a significant saving compared to British Columbia. However, lenders still assess income and stability rigorously.

- Montreal, Quebec: In Montreal, the private market is active, though language and specific provincial consumer protection laws might add a layer of nuance. The need for a comprehensive vehicle inspection and transparent seller communication remains universal.

Regardless of the city, the "zero bank drama" approach of specialized lenders provides consistent support for those with bad credit looking for private car loans.

Provincial Variations: Vehicle Registration, Sales Tax, and Insurance in Canada

While the financing aspect is similar, the provincial governments dictate specific rules for vehicle transfers, taxes, and insurance:

- Sales Tax:

- British Columbia (BC): 7% Provincial Sales Tax (PST) on the purchase price or wholesale value.

- Ontario: 13% Harmonized Sales Tax (HST) on the purchase price or wholesale value.

- Alberta: No provincial sales tax. You only pay the national 5% GST on new vehicles; private used vehicle sales are exempt from GST.

- Quebec: 9.975% Quebec Sales Tax (QST) on the purchase price or estimated value, plus 5% GST.

- Other Provinces: Varying rates of HST (e.g., Nova Scotia, New Brunswick, Newfoundland & Labrador, Prince Edward Island) or GST only (e.g., Saskatchewan, Manitoba).

- Registration: Each province has its own motor vehicle registry (e.g., ICBC in British Columbia, ServiceOntario in Ontario, SAAQ in Quebec) with specific forms and timelines for transferring ownership.

- Insurance:

- Public Systems: British Columbia, Saskatchewan, Manitoba, and Quebec have public insurance systems (ICBC, SGI, MPI, SAAQ respectively) that manage basic mandatory coverage.

- Private Systems: Other provinces operate with private insurance markets, allowing you to shop around for coverage.

PRO TIP: Always Verify Provincial Requirements for Private Vehicle Sales

Before initiating a private vehicle purchase outside of British Columbia, dedicate time to research and confirm the specific provincial and territorial regulations. This includes exact sales tax rates, required documentation for transfer, and mandatory insurance requirements. Government websites (e.g., ICBC, ServiceOntario, SAAQ) are the best sources for the most up-to-date information.

Your Next Steps to Approval: Driving Away with Confidence in Vancouver

You've journeyed through the intricacies of financing a private car sale with bad credit in Vancouver, from understanding the market's advantages to decoding lender expectations and navigating provincial regulations. The path to car ownership, even with past financial challenges, is not only possible but within your grasp.

Recap of Your Journey: From Bad Credit Doubts to Private Car Ownership

Remember the initial doubts? Perhaps the worry that bad credit would forever keep you from a reliable vehicle, or that traditional banks would always be a closed door. This guide has illuminated a different path:

- We've shown how Vancouver's private market offers cost-effective opportunities.

- We've dispelled myths, proving that specialized lenders prioritize your current stability over past credit woes.

- We've armed you with the knowledge to vet vehicles, understand provincial rules, and prepare your application with confidence.

- Most importantly, we've highlighted how this process isn't just about getting a car; it's a powerful tool for rebuilding your credit and fostering long-term financial health.

You now possess the blueprint to navigate the private car sale landscape, empowered by the knowledge that "zero bank drama" is a reality with the right financial partner.

Clear, Actionable Final Advice: Start Your Application Today

The time for hesitation is over. The freedom of a private car deal, financed with understanding and flexibility, awaits you in Vancouver. Here’s what you should do next:

- Assess Your Needs: Clearly define what kind of vehicle you need and what your budget allows for monthly payments.

- Gather Your Documents: Start collecting the necessary proof of income, residency, and identification.

- Begin Your Search: Confidently browse local online platforms for private sale vehicles that fit your criteria and lender guidelines.

- Apply for Pre-Approval: Take the first, crucial step by completing our simple online application. It's fast, secure, and the best way to understand your financing options without obligation.

Don't let bad credit dictate your mobility. Take control of your journey today. Your private car deal and the road to a stronger financial future start now.