Vehicle Repair Finance After Separation in BC | SkipCarDealer

Table of Contents

- Immediate Answers & Your First Steps

- Key Takeaways: Your First 5 Minutes Reading This Guide

- Key Takeaways

- The Legal & Financial Crossroads: Who is Responsible?

- Deep Dive: Is This Repair Bill 'Family Debt' Under BC Law?

- De-Coupling Your Credit: How Separation Impacts Your Lending Power

- Strategic Financing: Your Path to Getting Back on the Road

- The Strategic Advantage: Why Financing Beats Draining Your Post-Separation Savings

- Comparing Your Arsenal: Dealer Financing vs. Bank Loans vs. Lines of Credit

- Building Your Post-Separation Loan Application: A 7-Point Checklist for Success

- Looking Ahead: The Long-Term View

- The 2026 Outlook: How BC's Economy & New Lending Rules Could Impact Your Repair Loan

- Your Roadmap to a Repaired Vehicle and Financial Independence

- Frequently Asked Questions

Immediate Answers & Your First Steps

The piercing glow of the check engine light is the last thing you need right now. The emotional and logistical weight of a separation is already a full-time job. Juggling lawyers, finding a new place, and establishing a new routine is overwhelming. Now, the one machine you rely on to get to work, take the kids to school, or simply escape for a moment of clarity has decided to quit. This isn't just a mechanical failure; it's a financial and legal crisis hitting you all at once.

You're facing a critical question that thousands of British Columbians in your shoes have asked: Who pays for this? How can I afford a major repair when my household income has just been cut in half? The intersection of BC's complex family law and the urgent, practical need for a working vehicle is a confusing and stressful place to be.

But you are not stuck. This guide is your roadmap. We will walk you, step-by-step, through the legal questions, financial realities, and strategic options available. We'll move you from a state of crisis and confusion to a concrete action plan, getting you and your vehicle back on the road to independence.

Key Takeaways: Your First 5 Minutes Reading This Guide

Key Takeaways

- Debt Responsibility is Key: Under BC's Family Law Act, a vehicle repair bill could be considered 'family debt' if the car is 'family property', meaning the cost might be shared. This depends heavily on the date of separation.

- Your Income is Now Solo: Lenders will assess your loan application based on your individual income and credit, not your former household income. Gathering proof of your new financial reality is your first step.

- Dealer Financing Can Be Faster: While banks are an option, specialized dealer financing often has quicker approval times and understands vehicle-specific costs, which is critical when you need your car back on the road ASAP.

- Don't Drain Your Savings: Using financing preserves your cash reserves, which are vital for unexpected legal fees, moving costs, and establishing your new life post-separation.

- Documentation is Your Shield: Keep every quote, invoice, and communication about the repair. This documentation is crucial for potential family law proceedings to determine if the debt is shared.

The Legal & Financial Crossroads: Who is Responsible?

Before you can figure out how to pay for a repair, you need to understand who is legally on the hook for the bill. In British Columbia, the answer isn't always straightforward and hinges on provincial law and the specific details of your separation.

Deep Dive: Is This Repair Bill 'Family Debt' Under BC Law?

Under BC's Family Law Act, assets and debts acquired during a relationship are typically divided equally upon separation. This includes 'family property' (like a car) and 'family debt'. A significant car repair bill could fall into this category, but only if it meets certain criteria.

The core concept is this: was the debt incurred for a "family purpose"? Was the vehicle itself used for family purposes? Answering these questions is your first step in determining if you can legally seek contribution from your ex-partner.

Key Questions to Determine Responsibility:

- When was the vehicle purchased? If it was bought during the relationship, it's almost certainly family property.

- Whose name is on the ownership/loan? Even if the car is in one person's name, if it was used for family purposes, it's likely family property.

- Was the vehicle used for family purposes? Think commuting to a job that supports the family, driving kids to activities, grocery runs, and family vacations. If yes, it strengthens the case for it being family property.

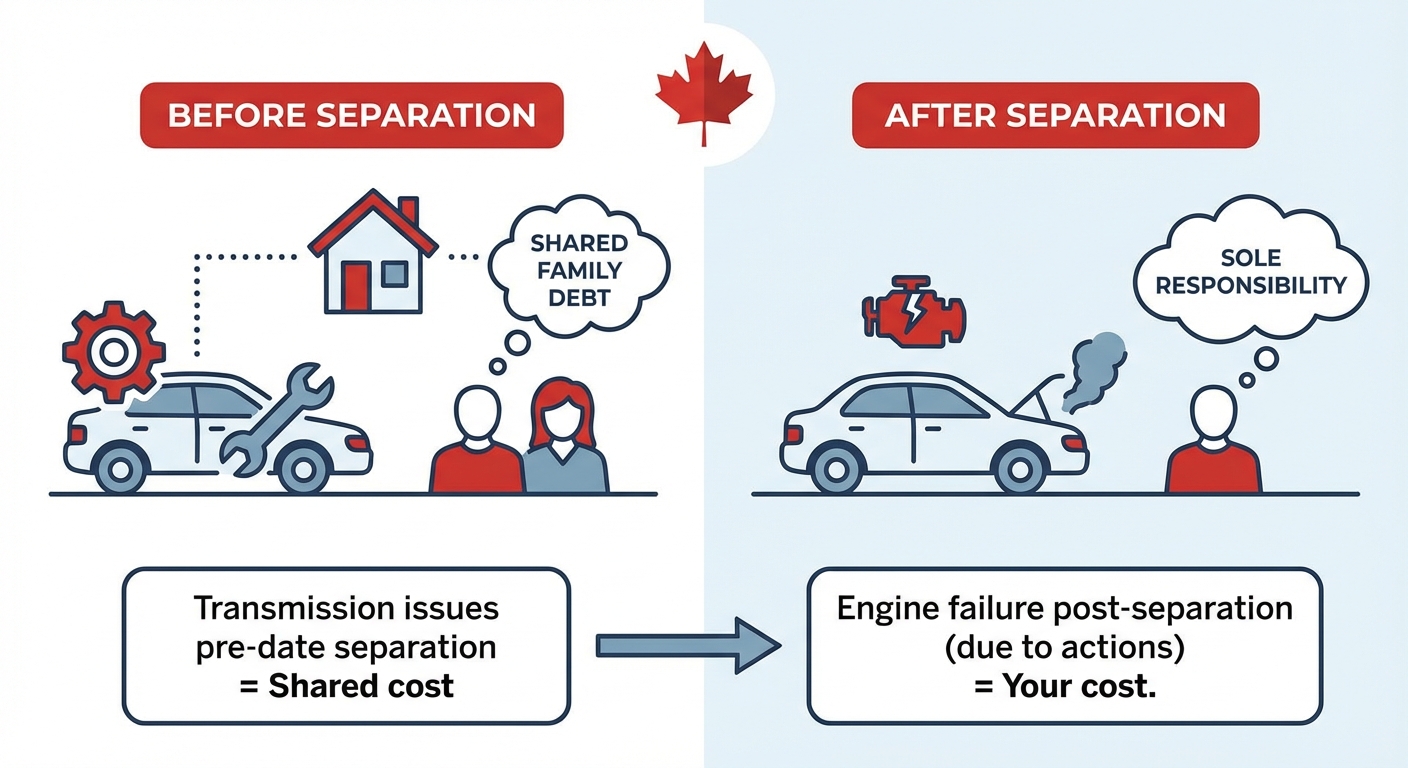

- Did the mechanical issue exist before the date of separation? This is a crucial point. If a known problem (like a failing transmission) existed before you officially separated, the repair cost is much more likely to be considered a shared family debt. If the engine blows a month after separation due to your own actions, it's more likely to be your sole responsibility.

Context: A flowchart titled 'Is Your Car Repair a Shared Family Debt in BC?'.

Context: A flowchart titled 'Is Your Car Repair a Shared Family Debt in BC?'.

Pro Tip: 'The Separation Date Matters Most.'

The official date of separation is the critical line in the sand. This is the date you and your partner began to live "separate and apart" with the intention of ending the relationship. Debts incurred before this date for a family purpose are generally family debt. Debts incurred after this date are generally considered the sole responsibility of the person who incurred them. Be prepared to establish this date in any legal discussion.

Disclaimer: This information is for guidance and does not constitute legal advice. The division of property and debt can be incredibly complex. We strongly recommend you consult a family lawyer for advice tailored to your specific situation.

De-Coupling Your Credit: How Separation Impacts Your Lending Power

One of the most immediate financial shocks of separation is realizing your financial identity has been intertwined with your partner's. For years, lenders saw you as a single household unit. Now, you're on your own, and your ability to secure a loan rests solely on your individual financial footing.

The first step is to understand your new reality. Pull your credit reports from both Equifax and TransUnion. Look for:

- Joint Accounts: Any loans, credit cards, or lines of credit held in both names. These are your biggest risk, as you are both 100% liable for the entire balance, regardless of who spent the money.

- Authorized User Status: Are you an authorized user on their card, or are they on yours? This can impact your score, and it's time to have those names removed.

Next comes the challenge of proving your income, especially if you weren't the primary earner, are re-entering the workforce, or now rely on support payments. Lenders need to see stable, verifiable income. Gather these documents:

- Recent pay stubs (last 2-3)

- A letter of employment or a new job contract

- Bank statements showing regular deposits

- A copy of your signed separation agreement or court order detailing spousal or child support payments. Many modern lenders, including SkipCarDealer, understand that these payments are a legitimate and stable source of income. For more on this, our guide on Vancouver Auto Loan with Child Benefit Income offers valuable insights.

Pro Tip: 'Notify Lenders of Your New Marital Status.'

It might feel counterintuitive to highlight a major life disruption on a loan application, but honesty is the best policy. When you apply, being upfront that you are "Separated" provides crucial context for the underwriter. It explains a recent change of address or a sudden shift in your financial picture. It shows you are organized and aware of your new circumstances, which can actually build confidence with the lender.

Strategic Financing: Your Path to Getting Back on the Road

When faced with a four-figure repair bill, the instinct might be to raid your savings. But in the midst of a separation, cash is king. Preserving your liquidity is one of the most powerful strategic moves you can make.

The Strategic Advantage: Why Financing Beats Draining Your Post-Separation Savings

Financing an urgent repair isn't just about not having the cash on hand; it's about protecting your financial future during a period of intense uncertainty. Think of it as a tool for self-preservation.

Consider these critical reasons to finance:

- Preserving Your Emergency Fund: The separation process is littered with unexpected costs. You may need cash for a rental deposit, a lawyer's retainer, moving expenses, or replacing essential household items. Draining your savings on a car repair leaves you vulnerable.

- Avoiding Asset Dissipation Claims: In family law, "dissipation of assets" refers to the intentional spending or wasting of family property to reduce what your ex-partner might receive. While a legitimate repair isn't dissipation, suddenly spending $7,000 in cash could raise questions. A documented loan for a specific, necessary repair is a clean, transparent transaction that is easy to explain in legal proceedings.

- Maintaining Financial Flexibility: A manageable monthly payment keeps your cash flow predictable. You know exactly what's going out, which helps you build your new, single-person budget without the shock of a massive one-time expense.

Let's make this real. Imagine the transmission on your Ford F-150, a common workhorse in BC, suddenly fails. You get a quote from a shop in Surrey for $6,500. Paying that in cash could wipe out the funds you've set aside for the first and last month's rent on a new apartment. Financing that repair, however, might translate to a payment of around $200 a month. That's a manageable expense that keeps your housing plan intact and your life moving forward.

Comparing Your Arsenal: Dealer Financing vs. Bank Loans vs. Lines of Credit

Once you've decided to finance, you have several options. Each has distinct advantages and disadvantages, especially for someone navigating a separation. The "best" choice depends on your priorities: speed, interest rate, or flexibility.

Here’s how they stack up in the context of a post-separation repair:

Context: An infographic comparison table.

Context: An infographic comparison table.

| Financing Option | Best For... | Approval Speed | Typical Interest Rate Range (BC) | Separation-Specific Challenge |

|---|---|---|---|---|

| Dealer Financing (e.g., SkipCarDealer) | Speed, convenience, and those with new or challenged credit situations. | Very Fast (often within hours; funding in 1-2 days) | 7.99% - 29.99% (Varies widely based on credit profile) | Interest rates can be higher than a prime bank loan, but approval odds are significantly better for non-traditional situations. |

| Bank/Credit Union Personal Loan | Individuals with excellent, established solo credit and a stable income history. | Slow (can take several days to a week) | 6.99% - 12.99% (Prime rates for top-tier credit) | Stricter income verification can be a hurdle for those recently separated or relying on support payments. Less flexible on credit imperfections. |

| Line of Credit (Personal or HELOC) | Flexibility to draw funds as needed, if you already have one established. | Varies (Fast if pre-existing; slow to apply for new) | Variable (Prime + 2% to Prime + 7%) | HIGH RISK. Using a joint LOC is extremely risky post-separation. A Home Equity Line of Credit (HELOC) will likely require your ex-spouse's signature. |

In our experience, when your primary goal is to get your vehicle out of the shop and get back to your life with minimal hassle, specialized dealer financing is often the most effective path. We work with individuals in unique situations every day, from gig workers to those rebuilding their credit. If you've recently been through bankruptcy or a consumer proposal as part of your separation, don't assume you're out of options. Our guide on Car Loan After Bankruptcy Discharge? The 2026 Approval Guide shows there's always a path forward.

Building Your Post-Separation Loan Application: A 7-Point Checklist for Success

A well-prepared application is a fast-approved application. Lenders value organization and clarity. Walking in with your documents in order shows you are serious and in control of your finances, even during a turbulent time. Use this checklist to build a bulletproof application.

- Official Repair Quote: Don't just give a verbal estimate. Get a detailed, written quote from a licensed repair facility. It should break down parts and labour costs clearly.

- Proof of Individual Income: Your last 2-3 pay stubs are standard. If you've just started a new job, an employment letter stating your salary and start date is crucial.

- Proof of Other Income: Don't forget to include a copy of your signed separation agreement or court order that specifies child or spousal support payments. This is verifiable income.

- Updated Personal Information: You'll need proof of your new address, like a recent utility bill or tenancy agreement, and a valid government-issued ID.

- Vehicle Ownership/Registration: The lender needs to see the vehicle's registration to confirm you are the legal owner of the asset they are financing.

- A Recent Credit Report: Pull your own credit report beforehand. Knowing your score and what's on your file allows you to address any potential issues proactively.

- A Brief, Factual Explanation (if needed): A short, typed note can work wonders. Simply stating, "Please note the recent change of address and marital status is due to a recent separation. My income sources are as listed." provides helpful context to underwriters.

Pro Tip: 'Apply for Pre-Approval First.'

Before you even authorize the repair, secure pre-approved financing. This accomplishes two critical things. First, it tells you exactly how much you can afford, giving you immense negotiating power with the repair shop. Second, it protects your credit score. Instead of having multiple repair shops pull your credit (which can lower your score), you have one pre-approval that you can take anywhere. It's the smartest first move you can make.

Looking Ahead: The Long-Term View

Getting your car fixed is the immediate battle, but winning the war means establishing long-term financial stability. Understanding future trends in lending and the economy can help you make smarter choices today.

The 2026 Outlook: How BC's Economy & New Lending Rules Could Impact Your Repair Loan

As a leader in Canadian auto finance, we keep a close eye on the horizon. Looking towards 2026, we see several trends that will impact borrowers in British Columbia.

First, interest rates. The Bank of Canada's rate-setting decisions have a direct impact on the cost of borrowing. While rates have been volatile, the general outlook suggests that securing a fixed-rate loan now could protect you from potential future increases. A variable-rate line of credit might seem cheaper today, but it could become more expensive over the next few years.

Second, the rise of digital lending. The shift towards AI-driven loan approvals is accelerating. For individuals in complex situations—like a recent separation—this can be a major benefit. Sophisticated algorithms can look beyond a simple credit score and analyze alternative data, like the consistency of support payments or gig economy income, leading to faster and fairer approvals. This technology is at the core of what we do at SkipCarDealer, allowing us to serve clients that traditional banks might turn away. For those with a challenging credit history, this technological shift is a game-changer. Our experience helping clients in BC shows that a low score is just a number, not a final verdict, as detailed in our guide That '69 Charger & Your Low Credit? We See a Future, British Columbia.

Finally, we anticipate potential changes in how credit bureaus report financial information for separated individuals. There is a growing push for systems that make it easier to de-couple joint accounts and establish solo credit histories more quickly. This could significantly reduce the time it takes for someone to rebuild their financial identity after a separation.

Your Roadmap to a Repaired Vehicle and Financial Independence

The journey from a broken-down car during a separation to financial control can feel long, but it's a series of clear, manageable steps. Here is your action plan:

- Step 1: Get a definitive quote. Visit a trusted mechanic and get a detailed, written estimate for the necessary repairs.

- Step 2: Assess debt responsibility. Use the principles in this guide to make an initial determination of whether this is a potential 'family debt'. Discuss this with your lawyer.

- Step 3: Gather your documents. Use the 7-point checklist from this article to assemble everything you need for a loan application.

- Step 4: Secure pre-approved financing. Know your budget and protect your credit score by getting pre-approved before you authorize the work. This puts you in the driver's seat.

- Step 5: Get the repair done. Authorize the work, get back on the road, and meticulously keep every receipt and invoice for your family law file.

Facing a major car repair during a separation is more than an inconvenience; it's a test of your resilience. But by understanding the legal landscape, taking control of your new financial reality, and making strategic financing choices, you can navigate this challenge successfully. This is a crucial step in rebuilding your independent life, one kilometre at a time.