Defy Bad Credit: Find Low Monthly Car Payments for 2026

Table of Contents

- Your Quick Path to an Affordable Car Payment

- The Reality Check: What Lenders See and How to Set Your Budget for 2026

- Deep Dive: Understanding Your Credit Score's Real Impact on Rates

- The '20/4/10' Rule, Modified for Bad Credit

- The Pre-Approval Gauntlet: Building Your Application Armour

- Your Essential Document Checklist

- Solving for Income Gaps or 'Gig Worker' Status

- Dealership Financing vs. Banks & Credit Unions: The Bad Credit Battleground

- The In-House Dealership: Convenience at a Potential Cost

- The Bank/Credit Union Pre-Approval: Your Negotiation Gold Standard

- The Smart Shopper's Playbook: Choosing the Right Car to Lower Your Payment

- Why a $15,000 Used Honda Civic is Better Than a $9,000 Old Minivan

- Negotiating Beyond the Sticker Price: Focus on the 'Out-the-Door' Number

- Your Next Steps: How This Car Loan Becomes Your Credit Rebuilding Tool

- Setting Up for Success: Bi-Weekly Payments and Automation

- Your Roadmap to the Driver's Seat: A Final Action Plan

- Frequently Asked Questions About Bad Credit Car Loans

The sting of a “loan denied” email is frustrating. It can feel like your past financial mistakes have locked you out of the driver's seat, forcing you to rely on inconvenient transit or unreliable rides. For many Canadians with bruised credit, the dream of a reliable vehicle with an affordable monthly payment seems miles away. But what if that’s not the whole story? What if there was a clear, strategic path to not only get approved for a car loan in 2026 but to secure a monthly payment that fits comfortably into your budget?

This isn't an article of maybes or vague suggestions. This is your strategic playbook. We’re going to pull back the curtain on how lenders view bad credit and give you the exact steps to take—from building your budget to choosing the right vehicle and negotiating like a pro. Forget the frustration. It's time to defy your credit score and find the low monthly car payment you deserve.

Your Quick Path to an Affordable Car Payment

- Focus on the Total Loan Cost, Not Just the Payment: A low payment over a long term can cost you thousands more. We'll show you how to calculate it.

- Your Down Payment is Your Superpower: A larger down payment (aim for 10-20%) is the single best way to lower your monthly cost and improve approval odds.

- Get Pre-Approved Before You Shop: Walking into a dealership in Toronto or Edmonton with a pre-approval from a credit union or online lender gives you immense negotiating power.

- Choose the Right Car for Your Credit: A reliable, 2-4 year old used vehicle is often the sweet spot for bad credit loans, offering lower prices and better interest rates than older cars.

- This Loan Can Be Your Credit's Second Chance: Making consistent, on-time payments is one of the fastest ways to rebuild your credit score for future, better loans.

The Reality Check: What Lenders See and How to Set Your Budget for 2026

To find low monthly car payments with bad credit, you must first shift your perspective from the car you want to the loan you can realistically secure. Lenders are in the business of managing risk, and a low credit score signals higher risk. By understanding exactly how they quantify that risk, you can build a budget and application that directly addresses their concerns, dramatically increasing your chances of approval at a reasonable rate.

Deep Dive: Understanding Your Credit Score's Real Impact on Rates

Your credit score isn't just a number; it's a price tag. Lenders in Canada use it to place you into tiers, each with a corresponding range of interest rates. For auto loans, these tiers generally look something like this:

- Prime (660-900): You're considered a low-risk borrower. Lenders compete for your business, offering the best rates (typically 5% - 9%).

- Near-Prime (600-659): You're on the edge. You'll likely get approved, but at a slightly higher rate than prime borrowers (typically 10% - 15%).

- Subprime (500-599): You're considered a higher risk due to past missed payments, collections, or high debt. Expect significantly higher interest rates (typically 16% - 25%+).

- Deep Subprime (Below 500): Approval is challenging and will almost always require a significant down payment and proof of very stable income. Rates will be at the highest end of the spectrum.

Let's see how this plays out in the real world. Consider a modest $20,000 car loan with a 60-month (5-year) term. The difference a hundred credit score points makes is staggering.

| Credit Profile | Example Credit Score | Estimated Interest Rate | Estimated Monthly Payment | Total Interest Paid |

|---|---|---|---|---|

| Near-Prime | 650 | 9.99% | $425 | $5,496 |

| Subprime | 550 | 18.99% | $519 | $11,140 |

| The "Bad Credit Premium" Over 5 Years: | $5,644 | |||

As the chart clearly shows, that 100-point difference costs you nearly $100 more every single month and over $5,600 in pure interest over the life of the loan. This is why your first step is always to know your score and ground your budget in this financial reality.

The '20/4/10' Rule, Modified for Bad Credit

You may have heard of the classic "20/4/10" rule for car buying: put 20% down, finance for no more than 4 years, and keep your total monthly car expenses (payment, insurance, fuel) under 10% of your gross income. It’s sound advice for someone with great credit, but it's often unrealistic for those in the subprime category.

We recommend the "10/5/15 Bad Credit Rule" for a safer, more achievable budget:

- 10% Down Payment (Minimum): Aim for at least a 10% down payment. On a $15,000 vehicle, that’s $1,500. This shows the lender you have skin in the game and immediately lowers the amount you need to finance. If you can do more, do more. A 20% down payment is your best weapon.

- 5-Year (60 Month) Maximum Term: Lenders will tempt you with 72, 84, or even 96-month terms to advertise a lower monthly payment. Resist. A longer term means you pay vastly more in interest and you'll be "upside-down" (owing more than the car is worth) for years. Stick to 60 months as your absolute maximum.

- 15% of Take-Home Pay for Total Costs: Instead of gross income, use your after-tax, take-home pay. And don't just budget for the loan payment. Add your estimated insurance premium, fuel costs, and a small buffer for maintenance. This total should not exceed 15% of your net monthly income.

Pro Tip: Factor in province-specific insurance rates. A driver in Brampton, Ontario, will have vastly different insurance costs than one in Calgary, Alberta, which directly impacts your total monthly budget. Get an online insurance quote for your desired vehicle *before* you start shopping to know your all-in cost.

The Pre-Approval Gauntlet: Building Your Application Armour

The single biggest mistake bad credit car buyers make is walking onto a dealership lot unprepared. This puts you on the defensive, letting the dealer control the financing process. The smart move is to build your case and get pre-approved *before* you even think about test drives. This empowers you, turning you from a credit applicant into a cash-ready buyer.

Your Essential Document Checklist

Lenders need to verify three things: who you are, where you live, and that you have a stable income to make payments. Having these documents ready makes you look organized and serious. Gather the following:

- Proof of Income: This is the most critical piece. You'll need your two most recent pay stubs. If your hours vary, bring the last three months' worth.

- Proof of Residence: A recent utility bill (hydro, gas) or a cell phone bill with your name and address is perfect. This proves stability.

- Valid Driver's License: It must be valid and not expired. This confirms your identity and legal ability to drive the vehicle you're financing.

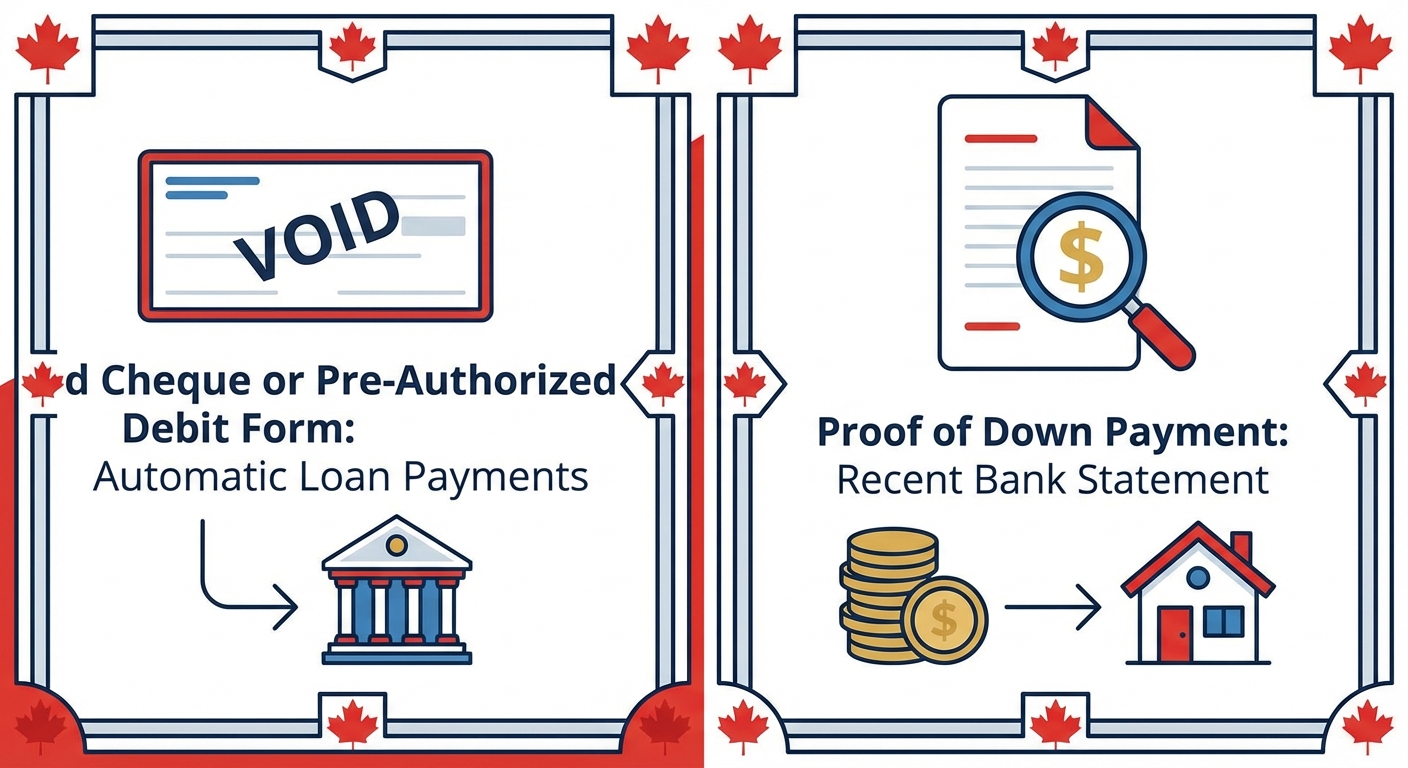

- Void Cheque or Pre-Authorized Debit Form: This is for setting up the automatic loan payments from your bank account.

- Proof of Down Payment: If you're providing a down payment, a recent bank statement showing the funds are available is often required.

Solving for Income Gaps or 'Gig Worker' Status

What if you don't have traditional pay stubs? This is a common hurdle for self-employed Canadians, freelancers, and gig economy workers. Don't worry, you can still prove your income, but it requires more documentation. Lenders need to see consistency.

Instead of pay stubs, you can build your case with:

- Personal Bank Statements: Provide the last 3-6 months of statements to show consistent deposits from your work.

- Notices of Assessment (NOA): Your last two years of NOAs from the Canada Revenue Agency (CRA) provide an official record of your declared income.

- Business Registration or Articles of Incorporation: If you have a registered business, this adds a layer of legitimacy.

- Letters from Major Clients: For freelancers, a letter from a primary client confirming your contract and regular payment can be very powerful.

The key is to paint a picture of financial stability. If your income fluctuates, it’s even more important to have a larger down payment to reduce the lender's risk. For a deeper dive into this topic, our guide on Variable Income Auto Loan 2026: Your Yes Starts Here. provides specific strategies for getting approved.

Dealership Financing vs. Banks & Credit Unions: The Bad Credit Battleground

Where you get your loan is just as important as the car you choose. For borrowers with bad credit, the options usually boil down to two main arenas: the dealership's in-house finance department or an outside lender like a bank or credit union. Each has distinct advantages and disadvantages.

The In-House Dealership: Convenience at a Potential Cost

Most dealerships have a Finance & Insurance (F&I) manager who works with a network of lenders, including those who specialize in subprime loans. This is often the path of least resistance.

Pros:

- Higher Approval Odds: They have relationships with lenders who specifically handle bad credit, bankruptcies, and consumer proposals. Their goal is to sell a car, so they will work hard to get you an approval.

- One-Stop-Shop: You can choose your car, negotiate the price, and secure financing all in one place, often in a single afternoon. This is highly convenient, especially if you need a vehicle urgently.

Cons:

- Much Higher Interest Rates: Convenience comes at a price. The rates offered through these specialized lenders are almost always higher than what you might find elsewhere. The dealership may also receive a commission from the lender for securing a higher rate.

- Limited Vehicle Selection: Sometimes, the lender will only approve a loan for specific types of vehicles on the lot (e.g., newer used cars under a certain kilometre limit), which can limit your choices.

This option can be a lifeline for someone in a smaller Ontario town who needs a car immediately for work and has been turned down by their bank. However, it's crucial to be aware of the potential costs. To protect yourself, it's wise to understand the warning signs of predatory lending, which we cover in detail in our guide on how to Unmasking 'Bad Credit' Car Lenders: Red Flags You Miss, Quebec.

Pro Tip: Always ask a dealership F&I manager if they are the direct lender (as in a 'Buy Here, Pay Here' lot) or if they are 'shopping' your application to multiple lenders. The latter can result in multiple hard inquiries on your credit report in a short period, which can temporarily lower your score further.

The Bank/Credit Union Pre-Approval: Your Negotiation Gold Standard

Securing a pre-approval from your own bank or a local credit union before you shop is a complete game-changer. It fundamentally alters the power dynamic at the dealership.

When you have a pre-approval letter in hand, you are no longer a credit applicant in the dealer's eyes; you are a cash buyer. You are there to negotiate the price of the car, not the terms of a loan. This allows you to focus solely on getting the best price for the vehicle.

In our experience, local credit unions are often more flexible and community-focused than large national banks. If you have a long-standing relationship with a credit union, they may be more willing to look past an old credit mistake and consider your current income and stability.

Here is a simplified comparison of the process:

| Factor | Dealership Financing | Bank/Credit Union Pre-Approval |

|---|---|---|

| Process | Find car first, then apply for financing. Emotionally invested. | Secure financing first, then shop for a car with a set budget. Logical and detached. |

| Interest Rates | Generally higher, especially for subprime credit. Rates can be marked up. | Often more competitive. You can shop around for the best rate before committing. |

| Negotiating Power | Lower. The negotiation is often a confusing mix of car price, trade-in, and financing terms. | Highest. You are negotiating one thing only: the "out-the-door" price of the car. |

The Smart Shopper's Playbook: Choosing the Right Car to Lower Your Payment

The vehicle you choose has a massive impact on the loan you can get. Lenders aren't just betting on you; they're betting on the car's ability to retain value. A smart vehicle choice can directly lead to a better interest rate and a lower monthly payment.

Why a $15,000 Used Honda Civic is Better Than a $9,000 Old Minivan

This might seem counterintuitive. Cheaper car should mean cheaper payment, right? Not always. Lenders operate on a principle called "Loan-to-Value" (LTV). They are more willing to lend money on an asset that holds its value well because if you default, they can recoup more of their money by repossessing and selling the vehicle.

A 3-year-old, low-kilometre Honda Civic, Toyota Corolla, or Hyundai Elantra is a lender's dream. It's reliable, in high demand, and depreciates slowly. A 12-year-old minivan with 200,000 km is a higher risk—it's more likely to have a major mechanical failure, leading the owner to stop making payments.

Because of this risk assessment, a lender might offer you a 16% interest rate on the $15,000 Civic but demand a 22% rate on the $9,000 minivan. Let's see how the payments shake out over 60 months:

- $15,000 Civic @ 16%: $365/month

- $9,000 Minivan @ 22%: $245/month

While the minivan's payment is lower, you're paying a much higher interest rate and getting a significantly older, less reliable vehicle that will likely cost you more in repairs. The Civic offers better value, more reliability, and helps you secure a more favourable loan structure.

Negotiating Beyond the Sticker Price: Focus on the 'Out-the-Door' Number

When you're at the dealership, a common tactic is to ask, "What monthly payment are you looking for?" This is a trap. It allows the salesperson to manipulate the numbers—extending the loan term, for example—to hit your payment target while charging you more for the car.

Your response should always be: "I'm not discussing monthly payments. I am focused on the 'out-the-door' price."

The "out-the-door" price is the total cost of the vehicle, including:

- The negotiated price of the car itself.

- Freight and PDI (Pre-Delivery Inspection) charges, which are common on new and some used cars.

- Dealership administration fees (always ask if these are negotiable).

- Any mandatory government fees (e.g., air conditioning tax).

- Provincial sales tax (HST in Ontario, GST/PST elsewhere), which is calculated on the final sale price.

Negotiate this single number. Once you have a final, all-in price, you can then apply your down payment and use your pre-approved loan to cover the rest. This keeps the transaction clean and ensures you know exactly what you're paying for.

Your Next Steps: How This Car Loan Becomes Your Credit Rebuilding Tool

Getting the keys to your new car isn't the end of the journey; it's the beginning of your credit recovery. This auto loan is one of the most powerful tools you have to rebuild your credit score. Every single on-time payment is reported to the credit bureaus (Equifax and TransUnion), demonstrating your reliability to future lenders.

Setting Up for Success: Bi-Weekly Payments and Automation

The best way to ensure you never miss a payment is to make it effortless. Here are two powerful strategies:

- Automate Everything: Set up automatic payments from your chequing account for the due date. This "set it and forget it" approach eliminates the risk of human error or forgetfulness, which is critical when rebuilding credit.

- Use Bi-Weekly Payments: If your lender allows it, switch to a bi-weekly payment schedule. You take your normal monthly payment, divide it by two, and pay that amount every two weeks. Because there are 26 bi-weekly periods in a year, you end up making 13 full monthly payments instead of 12. This small change helps you pay off the loan faster and reduces the total amount of interest you pay over the term.

Pro Tip: After 12-18 months of perfect, on-time payments, your credit score will have likely improved significantly. At this point, you should investigate refinancing your auto loan. You may be eligible for a new loan at a much lower interest rate, which could lower your monthly payment and save you thousands of dollars for the remainder of the term.

Your Roadmap to the Driver's Seat: A Final Action Plan

Feeling overwhelmed? Don't be. Here is your simple, step-by-step plan to get an affordable car payment in 2026, even with bad credit:

- Calculate Your Budget: Use the 10/5/15 rule. Determine your max all-in monthly cost (15% of take-home pay) and your minimum down payment (10% of vehicle price).

- Gather Your Documents: Assemble your proof of income, residence, and ID before you do anything else.

- Get Pre-Approved: Apply for a loan with your local credit union or a trusted online lender like SkipCarDealer.com to know exactly how much you can afford.

- Choose a Reliable Used Car: Focus on 2-4 year old sedans or small SUVs known for reliability. This lowers lender risk and can get you a better rate.

- Negotiate the Total Price: Ignore monthly payment talk. Negotiate the final, "out-the-door" price of the vehicle.

- Set up Automated Payments: Once you have the loan, set up automatic bi-weekly payments to build your credit score effortlessly.

Following this roadmap transforms you from a hopeful applicant into a prepared, strategic buyer. You can and will find a reliable car with a payment that works for you.