Quebec Newcomers: Your Credit History? We're Writing It With Your Car.

Table of Contents

- Key Takeaways

- The Quebec Road Ahead: Why a Car is More Than Just Transport for Newcomers

- The Zero-Credit Conundrum: Unpacking the Newcomer's Hurdle in Quebec

- Pro Tip 1: Start Small, Start Now

- Forging Your Credit Story: The Pathways to a Quebec Car Loan with Zero History

- Understanding Lender Archetypes

- 1. The Big Banks (e.g., RBC, CIBC, BMO): Newcomer Programs & Their Nuances

- 2. Dealership Financing: Your On-Site Advocate

- 3. Specialized Lenders & Credit Unions: The Alternative Route

- The Power of the Down Payment: Your Golden Ticket

- The Co-Signer Conundrum: A Double-Edged Sword

- Pro Tip 2: Get Pre-Approved, Then Shop

- Quebec's Unique Landscape: Laws, Taxes, and Consumer Rights for Car Buyers

- The Taxman Cometh: GST & QST on Vehicle Purchases

- Registration & Licensing: Navigating the SAAQ

- Mandatory Insurance: Protecting Your Investment (and Others)

- Winter Tire Law: A Quebec-Specific Imperative

- Consumer Protection Powerhouse: The Office de la protection du consommateur (OPC)

- Decoding the Numbers: Interest Rates, Loan Terms, and the True Cost of Car Ownership in Quebec

- Interest Rates for Newcomers: Setting Realistic Expectations

- Understanding Loan Terms: The 96-Month Dilemma

- Beyond the Sticker Price: Unpacking Hidden Costs and Quebec's Unique Taxes

- Pro Tip 3: Negotiate the Out-the-Door Price, Not Just the Monthly Payment

- Making the Choice: New vs. Used, Buying vs. Leasing for the Quebec Newcomer

- New Cars: The Lure of the Latest

- Used Cars: Value and Practicality

- Buying vs. Leasing: Ownership vs. Flexibility

- Pro Tip 4: Get a Pre-Purchase Inspection (PPI) for Any Used Car

- Your Credit Catalyst: How This Car Loan Builds Your Canadian Financial Future

- Steering Towards Success: Your Final Action Plan for Quebec Car Ownership

- Frequently Asked Questions (FAQ)

Arriving in Quebec as a new permanent resident brings a whirlwind of new experiences and opportunities. But for many, the dream of independent mobility, of navigating the vast landscapes from Montreal to Gaspésie, hits a speed bump: zero Canadian credit history. This isn't just about getting from point A to point B; it's about establishing your financial footprint in a new country. This comprehensive guide will demystify the process, empower you with knowledge, and show you how your first car loan in Quebec can be the cornerstone of your Canadian credit story.

Key Takeaways

- Your Zero Credit Isn't a Dead End: While challenging, securing a car loan in Quebec without prior Canadian credit is entirely possible, especially with strategic planning.

- Beyond the Banks: While major banks like RBC offer newcomer programs, explore dealership financing and specialized lenders, understanding their unique requirements and potential trade-offs.

- Down Payment is Your Best Friend: A significant down payment acts as a powerful risk mitigator for lenders, often improving your approval odds and potentially securing better rates.

- Quebec Specifics Matter: From the Office de la protection du consommateur (OPC) to sales taxes and mandatory winter tires, understanding Quebec's unique automotive landscape is crucial.

- This Car Loan is a Credit Builder: View your first car loan not just as transportation, but as a strategic financial tool to establish and build a strong Canadian credit history for future endeavors.

The Quebec Road Ahead: Why a Car is More Than Just Transport for Newcomers

Quebec is Canada's largest province by area, a vast and diverse territory stretching from the bustling urban centres of Montreal and Quebec City to the serene fjords of Saguenay and the rugged beauty of the Gaspé Peninsula. While Montreal boasts an impressive public transit system, the reality for many newcomers is that life and opportunities often extend far beyond the Métro lines. For those settling in regions like Laval, Longueuil, Gatineau, Sherbrooke, or even more rural communities, a personal vehicle quickly transitions from a luxury to a necessity.

Consider the geographical realities: securing a desirable job might mean commuting from the South Shore of Montreal to a business park in the West Island, or from a suburb of Quebec City to an industrial zone. Public transport, while functional in core areas, can become time-consuming, infrequent, or simply non-existent when you venture further out. A car provides essential access to these employment opportunities, allowing you to cast a wider net in your job search and reduce daily commute times, giving you back precious hours in your day.

Beyond employment, a car unlocks amenities and cultural integration. Imagine needing to visit a specialist doctor in a neighbouring town, taking your children to a unique cultural event outside the city, or simply exploring the provincial parks and beautiful landscapes that make Quebec so unique. A car enables families to access schools, healthcare facilities, grocery stores, and recreational activities with ease, significantly improving their overall quality of life and helping them feel more settled and integrated into their new community. It means spontaneous weekend trips to the Laurentians or the Eastern Townships become possible, fostering a deeper connection to your new home.

Ultimately, for many newcomers, car ownership is a tangible step towards achieving the "Canadian Dream" – the dream of independence, stability, and full integration. It signifies a level of self-sufficiency that opens doors to broader opportunities, greater convenience, and a richer life experience in Quebec. It's about being able to say, "I can go wherever I need to go, whenever I need to go."

The Zero-Credit Conundrum: Unpacking the Newcomer's Hurdle in Quebec

When you arrive in Canada, you effectively start with a blank financial slate. This means you have no Canadian credit history, a concept that can be perplexing for those accustomed to different financial systems in their home countries. So, what exactly is Canadian credit history? It's a detailed record of your borrowing and repayment behaviour maintained by credit bureaus like Equifax and TransUnion. Lenders rely on this history as a primary tool for risk assessment. A strong credit history demonstrates that you are a reliable borrower who pays debts on time, making you a more attractive candidate for loans, mortgages, and even apartment rentals.

The "Catch-22" for newcomers is stark: you need credit history to get credit, but you can't get credit without a history. This hurdle can feel insurmountable when attempting to finance a major purchase like a car, which is often essential for settling into Quebec life. Canadian lenders, unfamiliar with your financial past from another country, view applicants with no credit history as an 'unknown' risk. It's not necessarily a 'bad' risk, but a lack of data means they can't predict your repayment behaviour. This 'unknown' factor requires them to assess you using different criteria, often leading to more stringent requirements or higher interest rates than someone with an established credit profile.

Pro Tip 1: Start Small, Start Now

Do not wait until you need a car loan to begin building credit. Immediately upon arrival in Quebec, take proactive steps. Open a bank account, secure a secured credit card (where you deposit money as collateral), or even a basic credit card from your bank. Ensure utility bills (electricity, internet, phone) are in your name and paid on time. These small, consistent actions create early entries on your credit report, signaling to future lenders that you are financially responsible. For a more detailed guide on this, check out our article on New to Canada? Your Permanent Resident Auto Loan Starts Before Your Credit Does, Vancouver.

Forging Your Credit Story: The Pathways to a Quebec Car Loan with Zero History

Navigating the lending landscape in Quebec as a newcomer requires understanding the different types of financial institutions and their approaches. While the challenge of zero credit history is real, several pathways exist to secure your first car loan.

Understanding Lender Archetypes

Generally, you'll encounter three main types of lenders: major banks, dealership financing, and specialized lenders/credit unions. Each has its own criteria and advantages for newcomers.

1. The Big Banks (e.g., RBC, CIBC, BMO): Newcomer Programs & Their Nuances

Many of Canada's major banks offer specific programs designed to assist newcomers. These programs acknowledge the lack of Canadian credit history but compensate by looking for other strong indicators of financial stability. What they typically look for includes:

- Stable Employment: Full-time, permanent employment is highly valued. Lenders want to see consistent income.

- Proof of Income: Recent pay stubs (typically 2-3), an official employment letter, or even a job offer letter for those starting soon.

- Significant Down Payment: This is crucial. A substantial down payment reduces the loan amount and the lender's risk.

- Permanent Resident (PR) Card: Proof of your status in Canada is essential.

- Proof of Quebec Residency: Utility bills, a lease agreement, or other official documents confirming your address in a Quebec city like Montreal, Quebec City, or Sherbrooke.

When banks say 'No Canadian Credit History Required,' it means they won't automatically deny you for that sole reason. However, they will scrutinize other aspects of your financial profile even more closely. You'll need to present a very clear picture of stability and capacity to pay. The application process typically involves an in-person meeting with a banking advisor, who can guide you through their specific newcomer offerings and required documentation.

2. Dealership Financing: Your On-Site Advocate

Dealerships, such as SkipCarDealer.com, are often excellent resources for newcomers. They don't just sell cars; they act as intermediaries, working with a network of lenders. This network includes major banks, local credit unions, and even captive finance companies (e.g., Toyota Financial Services, Honda Financial Services) that are often more flexible, especially for new vehicle purchases.

The finance manager at a dealership plays a crucial role. They are experts in matching customers with suitable lenders based on their unique financial situation, including those with zero Canadian credit. They understand the nuances of newcomer applications and can often present your case to multiple lenders simultaneously, significantly increasing your approval odds. While rare, some dealerships might offer in-house financing directly, though these typically come with higher interest rates and stricter terms to compensate for the increased risk.

For individuals struggling to get approved through traditional banks, dealerships often have access to alternative lending solutions. If you've been told "No credit? Great. We're not your bank," by a dealership, it means they might have options beyond conventional lending. Visit our page No Credit? Great. We're Not Your Bank. for more insights.

3. Specialized Lenders & Credit Unions: The Alternative Route

Beyond major banks and dealership networks, there are specialized lenders and local credit unions that cater to higher-risk profiles, including newcomers with no credit history. These institutions may be more willing to approve loans where traditional banks might hesitate. The primary trade-off, however, is often significantly higher interest rates. While they offer a viable path to securing a vehicle and building credit, it's crucial to understand that the total cost of borrowing will be greater. Always compare offers carefully and ensure the monthly payments are manageable within your budget.

The Power of the Down Payment: Your Golden Ticket

A significant down payment is arguably the most powerful tool a newcomer has to secure a car loan. Why is it so crucial? It directly reduces the amount of money you need to borrow, thereby lowering the lender's risk. A larger down payment demonstrates your financial commitment and capacity to save, which are strong indicators of reliability. It often improves your approval odds and can even help you secure a more favourable interest rate. We often recommend aiming for a target range of 10-20% of the vehicle's purchase price, or even more if possible. The more you put down, the stronger your application becomes. For those who might be worried about a low down payment, check out our insights on Your Down Payment Just Called In Sick. Get Your Car.

The Co-Signer Conundrum: A Double-Edged Sword

Having a co-signer with an established, strong Canadian credit history can significantly improve your approval odds and potentially secure you a much lower interest rate. The co-signer essentially guarantees the loan, taking full responsibility if you default. However, finding a trusted individual with good credit who is willing to take on this significant financial obligation can be challenging for newcomers, who may not yet have deep roots or a wide network in Canada. It's a serious commitment for the co-signer, as their credit will be affected if payments are missed. While an option, it's often not the most accessible path for many new arrivals.

Pro Tip 2: Get Pre-Approved, Then Shop

Before you even step onto a dealership lot in Quebec, consider getting pre-approved for a car loan. This process involves a lender assessing your financial situation and providing an estimate of how much you can borrow and at what interest rate. Knowing your budget beforehand empowers you to shop confidently, focus on vehicles you can truly afford, and gives you strong negotiation leverage at the dealership. It transforms you from a hopeful buyer into a serious contender.

Quebec's Unique Landscape: Laws, Taxes, and Consumer Rights for Car Buyers

Buying a car in Quebec involves navigating specific provincial regulations, taxes, and consumer protections that are vital for newcomers to understand. Being prepared for these specifics will ensure a smoother and more transparent purchase experience, whether you're in Montreal, Quebec City, or Rimouski.

The Taxman Cometh: GST & QST on Vehicle Purchases

When you purchase a vehicle in Quebec, you'll be subject to two sales taxes: the federal Goods and Services Tax (GST) and the provincial Quebec Sales Tax (QST). As of late, GST is 5% and QST is 9.975%, which is applied to the price of the vehicle, including any accessories or optional services. Unlike some other provinces, QST is calculated on the price including GST, making the combined effective tax rate slightly higher (approximately 14.975%). This applies to both new and used vehicles purchased from a dealership. If you purchase a used vehicle from a private seller, you only pay QST on the higher of the purchase price or the estimated retail value of the vehicle, as determined by the Société de l'assurance automobile du Québec (SAAQ).

Registration & Licensing: Navigating the SAAQ

The Société de l'assurance automobile du Québec (SAAQ) is the provincial body responsible for vehicle registration and driver's licensing. All vehicles driven in Quebec must be registered with the SAAQ and carry valid license plates. As a newcomer, you'll need to provide proof of ownership, insurance, and your identity to register your vehicle. For your driver's license, if you hold a valid driver's license from your home country, you might be able to exchange it for a Quebec license, depending on agreements between Quebec and your country of origin. If no agreement exists, you may need to pass knowledge and road tests. It's crucial to address your driver's license status promptly, as it's a prerequisite for vehicle registration and insurance.

Mandatory Insurance: Protecting Your Investment (and Others)

Quebec has a unique dual-system for auto insurance. The SAAQ provides public insurance that covers bodily injuries sustained in an accident, regardless of fault. However, for vehicle damage (collision, comprehensive) and civil liability (damage to property or other vehicles), you must obtain private insurance from a licensed insurer. For newcomers, securing private insurance can sometimes be more expensive due to a lack of Canadian driving history. Factors influencing your premiums will include your driving record (if recognized), the type of vehicle, your age, and your location within Quebec (e.g., insurance rates can differ significantly between downtown Montreal and a smaller town in Saguenay).

Winter Tire Law: A Quebec-Specific Imperative

One of Quebec's most distinctive automotive laws is the mandatory use of winter tires. From December 1 to March 15, all passenger vehicles registered in Quebec must be equipped with winter tires. Failure to comply can result in fines and demerit points. This law is in place for safety, given Quebec's often harsh winter conditions. As a newcomer, you must budget for the cost of purchasing and installing winter tires, typically twice a year (summer tires off, winter tires on, and vice-versa). This is not an optional expense but a legal requirement for driving during winter months.

Consumer Protection Powerhouse: The Office de la protection du consommateur (OPC)

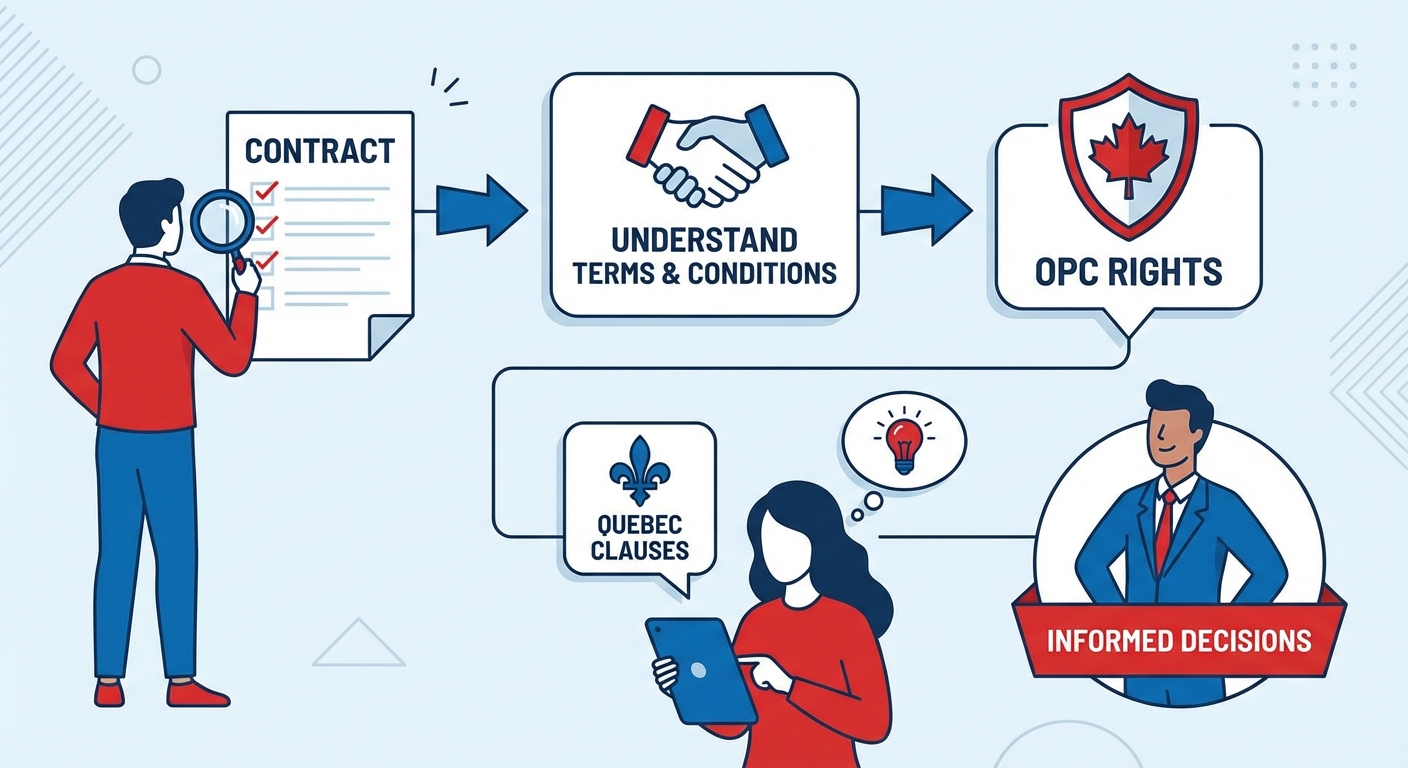

Quebec boasts one of the strongest consumer protection bodies in Canada: the Office de la protection du consommateur (OPC). The OPC plays a vital role in protecting car buyers in Quebec, ensuring fair practices, particularly regarding contracts, hidden fees, and disputes with dealerships. They regulate car sales, requiring dealerships to provide detailed contracts that clearly outline all costs, warranties, and terms. Before signing any car purchase or loan agreement, it is paramount that you review every line thoroughly. Understand all the terms, conditions, and Quebec-specific clauses. Knowing your rights, as upheld by the OPC, empowers you to make informed decisions and address any concerns effectively.

Image Context: The vastness of Quebec, from the bustling streets of Montreal to the serene landscapes of the Eastern Townships, makes personal transport a cornerstone of integration and mobility for newcomers. Understanding the provincial specifics is key to a smooth journey.

Decoding the Numbers: Interest Rates, Loan Terms, and the True Cost of Car Ownership in Quebec

Understanding the financial specifics of your car loan goes far beyond the monthly payment. For newcomers, a clear grasp of interest rates, loan terms, and the comprehensive costs of vehicle ownership in Quebec is essential to avoid unexpected financial strain.

Interest Rates for Newcomers: Setting Realistic Expectations

It's important to set realistic expectations regarding interest rates when you have zero Canadian credit history. Due to the perceived higher risk, lenders will typically offer rates significantly higher than those for established residents with excellent credit. While someone with a stellar credit score might secure a rate of 4-7% APR, newcomers could face rates ranging from 8-15% or even higher, particularly with specialized lenders. This is not a punitive measure but a reflection of the 'unknown' risk profile. The Annual Percentage Rate (APR) is the most critical number to look at, as it represents the true yearly cost of borrowing, including the interest rate and any associated fees. A 'good' rate for a newcomer with no credit might be anything below 10%, while anything above 15% should prompt careful consideration and comparison.

Understanding Loan Terms: The 96-Month Dilemma

Loan terms, often expressed in months (e.g., 60, 72, 84, or even 96 months), dictate how long you have to repay the loan. Longer terms, like the 84 or 96-month options sometimes offered by major banks like RBC or other lenders, can make monthly payments seem more affordable. This is a significant 'pro' for newcomers on a tighter budget. However, the 'con' is substantial: you pay significantly more interest over the lifespan of the loan. Furthermore, a longer term means your car depreciates faster than you build equity, potentially leaving you in an 'underwater' loan situation where you owe more than the car is worth. While lower monthly payments are appealing, always balance affordability with the total cost of the loan. Aim for the shortest term you can comfortably afford to minimize interest paid and build equity faster.

Beyond the Sticker Price: Unpacking Hidden Costs and Quebec's Unique Taxes

The purchase price and loan payments are only part of the equation. True car ownership in Quebec involves several ongoing costs:

- Vehicle Registration Fees: The SAAQ charges annual registration fees, which vary by vehicle type and region.

- Fuel Costs: Gas prices in Quebec can fluctuate, but they represent a significant ongoing expense, especially if you have a long commute or plan frequent trips to places like Gaspésie or Val-d'Or.

- Maintenance & Repairs: Budget for routine servicing (oil changes, tire rotations) and unexpected repairs. Quebec's harsh winters, with road salt and freezing temperatures, can accelerate wear and tear, making rust proofing a wise investment.

- Parking: If you live or work in urban centres like downtown Montreal or Quebec City, parking can be a considerable daily or monthly expense.

Pro Tip 3: Negotiate the Out-the-Door Price, Not Just the Monthly Payment

When discussing a car purchase, dealerships often focus on the monthly payment. While important for budgeting, focusing solely on this can obscure the total cost of the vehicle, leading you to pay more than necessary over the loan term. Always negotiate the "out-the-door price" – the total cost including all taxes, fees, and the vehicle price itself. Once you have this number, then work with your lender or finance manager to find a monthly payment that fits your budget, considering various loan terms and interest rates. This approach ensures transparency and prevents overpaying.

| Factor | Short Loan Term (e.g., 60 months) | Long Loan Term (e.g., 96 months) |

|---|---|---|

| Monthly Payment | Higher | Lower |

| Total Interest Paid | Significantly Less | Significantly More |

| Equity Building | Faster (car's value exceeds loan balance sooner) | Slower (risk of being "underwater" longer) |

| Flexibility/Future | Paid off sooner, more financial freedom | Longer commitment, ties up budget for extended period |

| Impact on Credit Score | Positive, if payments are on time | Positive, if payments are on time, but for longer duration |

Making the Choice: New vs. Used, Buying vs. Leasing for the Quebec Newcomer

Deciding between a new or used car, and whether to buy or lease, are significant considerations for any car buyer, especially for newcomers in Quebec establishing their financial footing.

New Cars: The Lure of the Latest

- Pros: A new car comes with a full manufacturer's warranty, offering peace of mind against unexpected repairs. You get the latest safety features, technology, and design. New cars are often easier to finance for newcomers through manufacturer-backed programs that can be more flexible.

- Cons: The most significant drawback is rapid depreciation. A new car loses a substantial portion of its value the moment you drive it off the lot. They also have a higher initial purchase price and typically higher insurance premiums.

Used Cars: Value and Practicality

- Pros: Used cars offer a lower initial cost, making them more accessible for budget-conscious buyers. Their depreciation curve is slower, meaning they retain their value better over time. You also have a much wider selection of makes and models across various price points.

- Cons: The primary risks with used cars are potential unknown history and the possibility of out-of-warranty repairs. Very old or high-mileage used cars can sometimes be harder to finance due to lender risk assessments.

- Crucial Steps for Used Car Buyers: To mitigate risks, always obtain a vehicle history report (like CarFax) to check for accident history, liens, and mileage discrepancies. More importantly, arrange a pre-purchase inspection (PPI) by an independent, trusted mechanic. This small investment can save you thousands in future repairs. And of course, always take a thorough test drive to assess the vehicle's performance and comfort.

Buying vs. Leasing: Ownership vs. Flexibility

This decision hinges on your long-term goals and financial situation as a newcomer.

- Buying: When you buy a car, you own it outright once the loan is paid off. This builds equity, gives you the freedom to customize the vehicle, and imposes no mileage limits. For newcomers focused on building Canadian credit and long-term stability, buying (especially a reliable used car) is generally the recommended path. Each on-time payment contributes directly to your credit score and future financial independence.

- Leasing: Leasing involves paying for the right to use a car for a set period, typically 2-5 years. It often comes with lower monthly payments and you're always driving a new car, usually under warranty, which means less maintenance responsibility. However, leasing often has stricter credit requirements, mileage limits (with penalties for exceeding them), and you build no equity in the vehicle. At the end of the lease, you return the car or have the option to buy it for a predetermined residual value. For newcomers, securing a lease can be more challenging due to the lack of credit history, and it doesn't offer the credit-building benefits of an installment loan.

Recommendation for Newcomers: Generally, buying (especially a reliable used car) is a more financially sound path for building credit and long-term stability. It allows you to build equity, avoid mileage restrictions, and use your car loan as a powerful credit-building tool.

Pro Tip 4: Get a Pre-Purchase Inspection (PPI) for Any Used Car

No matter how reputable the seller or how clean the vehicle history report, always invest in a pre-purchase inspection by an independent, certified mechanic. This small cost (typically $100-$200) can uncover hidden mechanical issues, safety concerns, or expensive repairs that could save you thousands of dollars and immense headaches down the road. It’s an indispensable step for any used car purchase in Quebec.

| Feature | Buying (New or Used) | Leasing (New Only) |

|---|---|---|

| Initial Cost | Higher (full purchase price or significant down payment) | Lower (typically smaller down payment or none) |

| Monthly Payments | Higher (paying off full vehicle cost) | Lower (paying for depreciation during lease term) |

| Ownership & Equity | You own the car; builds equity over time | No ownership; no equity built |

| Credit Building for Newcomers | Excellent (installment loan shows repayment ability) | More challenging (stricter credit requirements; less impact on credit mix) |

| Mileage Restrictions | None | Strict limits with penalties for overage |

| Maintenance | Your responsibility (can be costly for used cars) | Often covered by warranty during lease term |

| End of Term Options | Keep, sell, trade-in, customize | Return car, buy out lease, lease new car |

Your Credit Catalyst: How This Car Loan Builds Your Canadian Financial Future

For newcomers to Quebec, your first car loan is far more than just a means of transportation; it's a powerful financial tool, a credit catalyst that can rapidly accelerate your integration into the Canadian financial system. When managed responsibly, a major installment loan like an auto loan is a significant positive entry on your credit report, carrying substantial weight in the calculation of your credit score.

The golden rule for credit building is simple yet profoundly impactful: on-time payments. Every single payment you make on or before its due date is a positive mark on your credit history. Lenders and credit bureaus value consistency and reliability above almost all else. Over several months, these consistent payments will demonstrate to future lenders (and credit bureaus like Equifax and TransUnion) that you are a trustworthy borrower, capable of managing significant debt. This track record of responsible repayment is the bedrock upon which a strong Canadian credit score is built.

It's crucial to actively monitor your progress. You are entitled to a free copy of your credit report from Equifax and TransUnion annually. Regularly reviewing these reports allows you to understand your credit score, check for any inaccuracies, and see how your car loan is positively impacting your credit profile. Look for increasing credit scores and the consistent record of "paid as agreed" entries for your auto loan.

Beyond the car itself, leveraging your new credit history opens doors to a wider array of financial products and opportunities in Quebec and across Canada. A successfully managed car loan can make you eligible for:

- Better Credit Cards: You might qualify for unsecured credit cards with higher limits, lower interest rates, and better rewards programs.

- Personal Loans: Access to personal loans for other needs, often at more favourable terms.

- Mortgages: Perhaps the most significant long-term goal for many newcomers, a strong credit history from a car loan is a crucial prerequisite for securing a mortgage to buy a home in Montreal, Gatineau, or anywhere else in Canada.

- Lower Insurance Premiums: A good credit score can even indirectly influence some insurance providers, potentially leading to better rates over time.

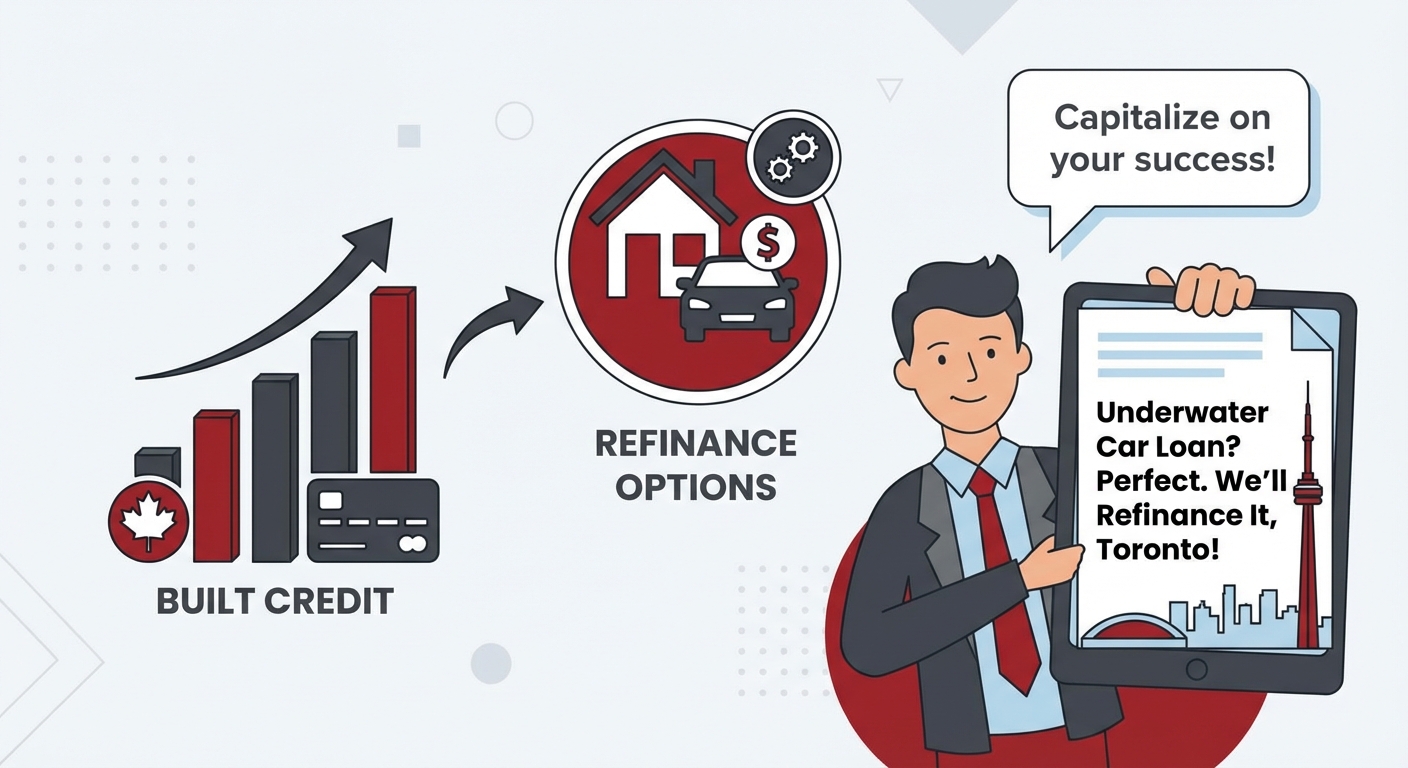

After 12 to 24 months of perfect, on-time payments, you may even be in a position to re-evaluate your loan. With a significantly improved credit score, you could explore refinancing options for your car loan. Refinancing allows you to potentially secure a lower interest rate, which can dramatically reduce your total interest paid and your monthly payments. This is an excellent way to capitalize on the credit you've built. For more information on refinancing, especially if you're looking to improve your loan terms, consider reading our article on Underwater Car Loan? Perfect. We'll Refinance It, Toronto!

Image Context: Your car loan isn't just a means of transport; it's a powerful and visible tool for establishing your financial credibility in Canada. Every on-time payment is a step towards a robust credit score and a brighter financial future in Quebec.

Steering Towards Success: Your Final Action Plan for Quebec Car Ownership

Embarking on the journey of car ownership in Quebec as a newcomer is a significant step towards independence and integration. By approaching the process strategically and with informed decision-making, you can turn the challenge of zero credit history into an opportunity to build a strong financial foundation.

First, review your financial readiness. Ensure you have a stable job with consistent income, a solid understanding of your budget, and a clear picture of all associated costs beyond the monthly payment (insurance, fuel, maintenance, winter tires). A substantial down payment remains your strongest asset in this process.

Next, gather all your documents. This checklist should include your Permanent Resident card, employment letter and recent pay stubs, bank statements, proof of address in Quebec (utility bills, lease agreement), and your driver's license. Having everything organized will streamline the application process.

Then, explore all lender avenues. Don't limit yourself to just one option. Check with major banks offering newcomer programs, leverage the expertise of dealership finance managers who work with a network of lenders, and research specialized lenders or credit unions if necessary. Compare offers meticulously, focusing on the APR and total cost of the loan.

Most critically, read every line of the contract. Do not rush this step. Understand all the terms, conditions, interest rates, fees, and Quebec-specific clauses before you sign. If anything is unclear, ask questions until you are completely satisfied. The Office de la protection du consommateur (OPC) is there to protect your rights, so be informed.

Finally, embrace the journey. This process is more than just buying a car; it's about building your financial identity in Canada. View your car loan as a strategic investment in your credit future. Make every payment on time, and watch as your Canadian credit history flourishes, opening doors to even greater financial opportunities down the road. With careful planning and responsible management, your first car in Quebec will be a symbol of your successful integration and a testament to your financial diligence.