Retiree Car Finance: Zero Down with Investment Income.

Table of Contents

- Key Takeaways

- Retiree Car Finance: Zero Down with Investment Income

- Beyond the Paycheck: Why Investment Income is Your Golden Ticket to Auto Ownership

- The Lender's Lens: How Financial Institutions Evaluate Investment Income for Stability and Consistency

- Diversifying Your Income Portfolio: Highlighting Dividends, Interest, RRIF/RRSP Withdrawals, and Rental Income

- Strategic Withdrawal Planning: Optimizing RRIF/RRSP Distributions to Enhance Loan Applications

- Pension vs. Portfolio: Understanding the Nuances of Guaranteed vs. Managed Income Streams

- Pro Tip: Documenting Your Income Stream – What Lenders Really Want to See for Seamless Approval

- Decoding 'Zero Down': The Reality and the Risks for Retirees

- The 'No Money Down' Promise: Separating Marketing Hype from Financial Reality

- The Trade-Offs: How Zero Down Can Impact Interest Rates, Loan Terms, and Overall Cost

- Protecting Your Nest Egg: When is Zero Down a Prudent Financial Move (and When is it Not)?

- Understanding Your Debt-to-Income Ratio: Implications of a Zero-Down Commitment

- Strategies to Mitigate Risk: Exploring Shorter Terms, Higher Monthly Payments, and GAP Insurance

- Navigating the Lending Labyrinth: Where Retirees Find Their Best Zero-Down Deals

- Traditional Banks: The Conservative Approach to Assessing Retirement Income

- Credit Unions: Often More Flexible, Community-Oriented, and Understanding of Unique Income Scenarios

- Dealership Financing: Convenience vs. Competitive Rates – A Balancing Act for Retirees

- Specialized Auto Finance Companies: Tailored Solutions for Diverse Investment Income Profiles

- The Role of Brokers: Unlocking Hidden Opportunities and Matching Retirees with Ideal Lenders

- Pro Tip: The Power of Pre-Approval – Your Negotiation Superpower in Any Showroom

- Maximizing Your Approval Odds: Beyond the Credit Score

- The Unsung Hero: Demonstrating Income Stability and Predictability Through Documentation

- Credit Score Re-examined: What a 'Good' Score Truly Means for Retiree Auto Finance

- Debt Management: How Existing Obligations Impact Your Eligibility and Strategies for Optimization

- Leveraging Assets: How Your Net Worth Can Indirectly Strengthen Your Application (Without Collateral)

- Building a Strong Case: The Art of Presenting a Comprehensive Application Package

- Pro Tip: Co-Signers and Guarantors – When They Help and When They Might Hinder Your Application

- The True Cost of Convenience: Hidden Fees, Insurance, and Extended Warranties

- Beyond the Monthly Payment: Dissecting Loan Origination, Administrative, and Documentation Fees

- Mandatory Insurance: The Non-Negotiable Cost of Ownership and How it Varies for Retirees

- Extended Warranties: Are They a Prudent Investment for Retirees or an Unnecessary Expense?

- Registration, Taxes, and Licensing: The Initial Out-of-Pocket Expenses to Budget For

- The 'Total Cost of Ownership' Equation: Factoring in Fuel, Maintenance, and Depreciation Over Time

- Choosing Your Ride: Car Brands, Models, and Resale Value Considerations for Retirees

- Reliability First: Brands Known for Longevity, Lower Maintenance Costs, and Peace of Mind

- Safety Features: Prioritizing Advanced Driver-Assistance Systems (ADAS) and Crash Test Ratings

- Ergonomics and Accessibility: Ensuring Comfort, Ease of Entry/Exit, and User-Friendly Controls

- The Resale Value Factor: Protecting Your Investment (Even Without an Initial Down Payment)

- New vs. Used: Weighing the Financial Implications and Benefits for Zero-Down Applicants

- Pro Tip: Test Driving Beyond the Showroom – Evaluating Real-World Usability and Comfort

- The Road Ahead: 2026 Market Outlook and Emerging Trends in Retiree Auto Finance

- Regulatory Shifts: How Potential New Rules Might Impact Retiree Lending and Protections

- Technological Innovations: The Rise of Electric Vehicles (EVs) and Their Financing Implications for Retirees

- Economic Forecasts: Interest Rate Predictions and Their Effect on Auto Loan Affordability

- Alternative Ownership Models: Exploring Subscription Services and Their Viability for Retirees

- The Future of Investment Income Verification: Streamlined, Digital Processes on the Horizon?

- Your Next Steps to Driving Away with Confidence

- Step 1: Comprehensive Financial Health Check-Up and Meticulous Documentation Gathering

- Step 2: Exploring All Lender Options and Securing the Best Pre-Approval Offer

- Step 3: Smart Vehicle Selection, Thorough Research, and Extensive Test Driving

- Step 4: Decoding the Loan Agreement, Understanding All Terms, and Skillfully Negotiating

- Step 5: Finalizing the Purchase and Implementing Strategies to Protect Your Investment Long-Term

Retirement in Canada brings a new chapter of freedom, and for many, that includes the desire for a reliable vehicle to explore our vast landscapes, visit family, or simply maintain independence. But what if you're a retiree living on investment income, and the thought of a significant down payment seems daunting? The good news is, securing zero-down car finance in 2026 is not just a dream for retirees with stable investment income; it's a very achievable reality. SkipCarDealer.com is here to guide you through the intricacies, showing you how your hard-earned portfolio can be your golden ticket to a new set of wheels without touching your principal.

Key Takeaways

- Dispelling the Age Myth: Lenders prioritize income stability and financial health over age. Your consistent investment income is a powerful asset.

- The Power of Passive: Diverse investment income streams like dividends, interest, RRIF/RRSP withdrawals, and rental income are highly valued by lenders.

- Decoding 'Zero Down': Understand that 'zero down' can impact interest rates and overall cost. Strategic planning is crucial to make it a prudent financial move.

- Strategic Lending: Credit unions and specialized auto finance companies often offer more flexibility for retirees leveraging investment income than traditional banks.

- Future-Proofing Your Purchase: Prepare for 2026 by understanding evolving regulations, new vehicle technologies, and economic forecasts to make informed decisions.

Retiree Car Finance: Zero Down with Investment Income

For Canadian retirees, zero-down car finance with investment income means securing a vehicle loan without an initial lump-sum payment, by demonstrating a reliable and consistent income stream derived from investments such as dividends, interest, RRIF/RRSP withdrawals, or rental properties, which lenders accept as sufficient proof of repayment capability.

Beyond the Paycheck: Why Investment Income is Your Golden Ticket to Auto Ownership

Gone are the days when a traditional employment paycheck was the sole determinant of creditworthiness. For retirees across Canada, from the bustling streets of Toronto to the serene coasts of Vancouver Island, your investment income portfolio has emerged as a powerful and often preferred alternative for securing auto financing. Lenders are increasingly recognizing the stability and predictability that well-managed investment income streams offer, sometimes even viewing them as more reliable than fluctuating employment wages. This section delves into how different forms of investment income are assessed, positioning them as your strongest asset for car loan qualification.

The Lender's Lens: How Financial Institutions Evaluate Investment Income for Stability and Consistency

When you approach a lender for a car loan, their primary concern is your ability to repay. For retirees, this evaluation shifts from employment history to the robustness of your financial portfolio. Lenders scrutinize the source, consistency, and longevity of your investment income. They want to see a clear pattern of regular distributions, whether monthly, quarterly, or annually, that can comfortably cover potential loan payments. For instance, a retiree in Montreal receiving consistent dividend payouts from a diversified portfolio for several years presents a much stronger case than someone with sporadic, unpredictable capital gains. They'll ask for statements, tax assessments, and potentially letters from your financial advisor to verify these streams.

Diversifying Your Income Portfolio: Highlighting Dividends, Interest, RRIF/RRSP Withdrawals, and Rental Income

Your investment income isn't a monolith; it's often a rich tapestry of various sources. Each type holds unique weight with lenders:

- Dividends: Regular dividends from established, blue-chip Canadian companies (like those on the TSX) are often viewed as highly stable. Lenders prefer a history of consistent payouts over several years.

- Interest Income: Income from bonds, GICs, or high-interest savings accounts is typically considered very stable and predictable, especially if the underlying assets are low-risk.

- RRIF/RRSP Withdrawals: Scheduled withdrawals from your Registered Retirement Income Fund (RRIF) or Registered Retirement Savings Plan (RRSP) are a cornerstone of many retirees' income. Lenders will look at the withdrawal schedule and the total balance to ensure sustainability over the loan term.

- Rental Income: If you own income properties in Calgary or elsewhere, consistent rental payments, backed by lease agreements and bank statements, are an excellent source of verifiable income. Expenses related to the property will also be factored in.

Strategic Withdrawal Planning: Optimizing RRIF/RRSP Distributions to Enhance Loan Applications

For many Canadian retirees, RRIF and RRSP withdrawals form a substantial part of their monthly income. To maximize your chances of zero-down approval, strategic withdrawal planning is key. Consider structuring your withdrawals to be consistent and predictable, perhaps on a monthly basis, mirroring a traditional paycheck. This demonstrates a reliable income flow to lenders. It's often beneficial to have a financial advisor help you plan these distributions not only for tax efficiency but also to present a strong, steady income profile to potential lenders. They want to see that you're not depleting your nest egg too quickly. For more on how pension and other income types are viewed, check out our guide on Your Pension is the New Pay Stub. Get Approved for a Car, Calgary.

Pension vs. Portfolio: Understanding the Nuances of Guaranteed vs. Managed Income Streams

While a defined-benefit pension offers a guaranteed income, investment income from a managed portfolio introduces a different dynamic. Lenders understand the market fluctuations but prioritize a well-diversified portfolio managed by a reputable advisor. They assess the asset allocation, historical performance, and your withdrawal strategy. A pension might offer absolute certainty, but a robust, well-documented investment income stream can often be equally, if not more, persuasive, especially if it demonstrates significant capital reserves beyond the income itself.

Pro Tip: Documenting Your Income Stream – What Lenders Really Want to See for Seamless Approval

The key to success is meticulous documentation. Lenders need tangible proof. Prepare at least 3-6 months of bank statements showing consistent deposits from your investment income sources. Include your latest Notice of Assessment (NOA) from the Canada Revenue Agency (CRA), investment account statements, RRIF/RRSP withdrawal schedules, and any relevant tax slips (T3, T4RIF, T5). For rental income, provide lease agreements and corresponding bank deposit records. The more transparent and organized you are, the smoother your approval process will be.

Decoding 'Zero Down': The Reality and the Risks for Retirees

The allure of a 'zero down' car loan is undeniable, especially for retirees who wish to preserve their capital. It means driving away in a new vehicle without upfront cash. However, it's crucial to understand that 'zero down' is not a magic bullet; it comes with its own set of financial implications. This section will peel back the marketing layers, exposing the reality of zero-down financing and how it can impact your total cost of ownership as a retiree in Canada.

The 'No Money Down' Promise: Separating Marketing Hype from Financial Reality

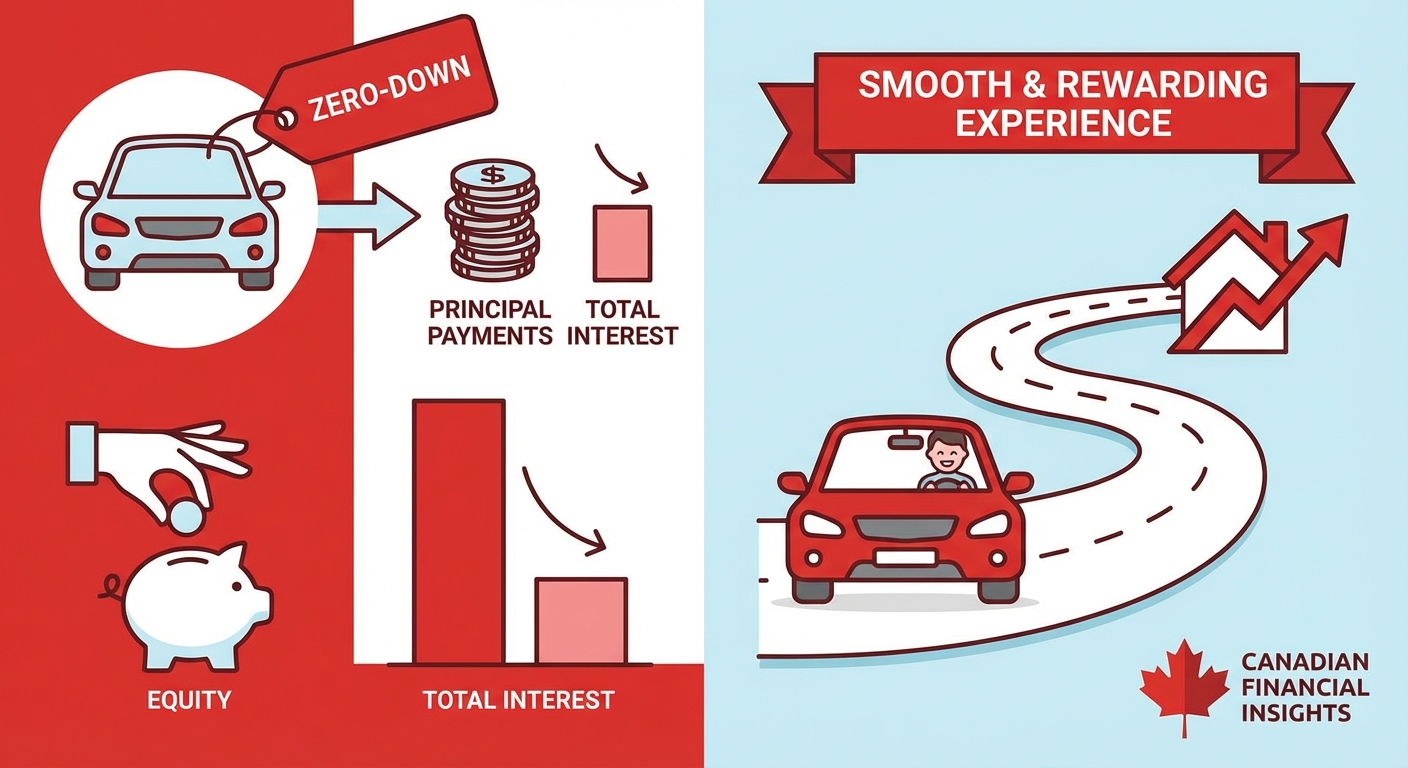

When you see advertisements for "no money down," it means you don't have to pay a cash lump sum at the time of purchase. However, the cost of that down payment doesn't disappear; it's simply rolled into the total amount financed. This increases your principal loan amount, which in turn means you'll pay more interest over the life of the loan. While preserving your immediate cash flow, it often translates to higher monthly payments or a longer loan term, or both. For retirees, this means a careful calculation to ensure the convenience doesn't outweigh the long-term financial strain on your fixed income.

The Trade-Offs: How Zero Down Can Impact Interest Rates, Loan Terms, and Overall Cost

Embracing a zero-down option often means accepting certain trade-offs. Lenders perceive loans with no down payment as having a higher risk, as there's less equity from the outset. This can lead to slightly higher interest rates compared to loans where a substantial down payment (e.g., 10-20%) is made. Let's look at an example for a $30,000 vehicle in Vancouver:

| Scenario | Loan Amount | Interest Rate (Est.) | Term (Months) | Monthly Payment (Est.) | Total Interest Paid (Est.) |

|---|---|---|---|---|---|

| Zero Down | $30,000 | 8.99% | 72 | $537 | $8,664 |

| 10% Down ($3,000) | $27,000 | 7.99% | 72 | $464 | $6,408 |

| 20% Down ($6,000) | $24,000 | 6.99% | 72 | $406 | $5,232 |

As you can see, the 'convenience' of zero down can add thousands to your total cost over the loan term. This isn't to say it's always a bad idea, but it requires careful consideration of your budget and investment income stability.

Protecting Your Nest Egg: When is Zero Down a Prudent Financial Move (and When is it Not)?

Zero down can be a prudent move for retirees when:

- Your investment income is exceptionally stable and significantly exceeds your expenses, allowing you to comfortably absorb higher monthly payments.

- You have a high-yield investment that you don't want to liquidate, and its returns significantly outpace the car loan interest rate.

- You need to maintain maximum liquidity for unexpected emergencies or other strategic investments.

However, it might not be prudent if:

- Your investment income is tight or prone to significant fluctuations.

- The higher interest cost puts undue strain on your monthly budget, potentially forcing you to dip into your principal earlier than planned.

- You prioritize minimizing total interest paid over maintaining immediate liquidity.

Understanding Your Debt-to-Income Ratio: Implications of a Zero-Down Commitment

Your debt-to-income (DTI) ratio is a critical metric for lenders. It compares your total monthly debt payments to your gross monthly income. A zero-down loan means a higher principal, leading to higher monthly payments, which in turn increases your DTI ratio. For retirees, maintaining a healthy DTI (typically below 40% for housing and all other debts) is vital. A higher DTI could limit your ability to secure future credit or impact your overall financial flexibility. Lenders in cities like Calgary and Toronto pay close attention to this.

Strategies to Mitigate Risk: Exploring Shorter Terms, Higher Monthly Payments, and GAP Insurance

If you opt for zero-down financing, consider these strategies to mitigate the inherent risks:

- Shorter Loan Terms: While monthly payments will be higher, a 48- or 60-month term instead of 72 or 84 months significantly reduces the total interest paid and helps you build equity faster.

- Higher Monthly Payments (if feasible): If your budget allows, making slightly higher payments than required can reduce your principal more quickly and save on interest.

- GAP Insurance: This covers the "gap" between what you owe on your loan and what your comprehensive insurance policy would pay if your car is stolen or totaled. With zero down, you're immediately "upside down" (owe more than the car is worth), making GAP insurance a wise investment.

Navigating the Lending Labyrinth: Where Retirees Find Their Best Zero-Down Deals

Finding the right lender is paramount for retirees seeking zero-down car finance with investment income. Not all financial institutions evaluate non-traditional income sources equally. Understanding the nuances of each lending avenue can significantly impact your approval odds, interest rates, and overall experience. Let's explore where retirees in Canada, from Edmonton to Halifax, can best navigate the lending landscape.

Traditional Banks: The Conservative Approach to Assessing Retirement Income

Major banks like RBC, TD, Scotiabank, BMO, and CIBC are often the first stop for many. While they offer competitive rates for prime borrowers, their assessment of investment income can be more conservative. They prefer clear, consistent, and long-standing income streams, often with a preference for substantial assets backing those streams. They might require more extensive documentation and have stricter debt-to-income ratios. Their processes can sometimes be less flexible for unique income scenarios, though they are certainly a viable option for retirees with rock-solid financial statements and high credit scores.

Credit Unions: Often More Flexible, Community-Oriented, and Understanding of Unique Income Scenarios

Credit unions, such as Vancity, Meridian Credit Union, or Desjardins, frequently stand out as more retiree-friendly options. Being member-owned and community-focused, they often have a more holistic approach to evaluating loan applications. They are typically more willing to look beyond rigid criteria and consider the full picture of a retiree's financial health, including diverse investment income streams, net worth, and long-term financial planning. Their rates can be very competitive, and their personalized service can make the application process feel less intimidating. They often have specific programs or understanding for members on fixed or investment-based incomes.

Dealership Financing: Convenience vs. Competitive Rates – A Balancing Act for Retirees

Dealership financing offers unparalleled convenience. You can select your vehicle and arrange financing all in one place. Dealerships work with a network of lenders, including captive finance companies (e.g., Ford Credit, Toyota Financial Services) and external banks. While convenient, it's essential to be cautious. The rates offered might not always be the most competitive, as the dealership earns a commission. However, for retirees with strong credit and investment income, dealerships can sometimes access special manufacturer incentives (like 0% financing promotions, though rare for zero-down and often for shorter terms). Always get a pre-approval from an external lender before visiting the dealership to have a benchmark for negotiation. For insights into ensuring your loan is legitimate, consider reading How to Check Car Loan Legitimacy 2026: Canada Guide.

Specialized Auto Finance Companies: Tailored Solutions for Diverse Investment Income Profiles

Companies like SkipCarDealer.com specialize in connecting individuals with lenders who understand unique financial situations, including those of retirees relying on investment income. These companies often have a broader network of lenders, some of whom specialize in non-traditional income verification. They can be particularly helpful if your investment income structure is complex or if you've faced rejections from traditional banks. They focus on your ability to pay, often looking at bank statements and investment statements more closely than just credit scores. This is where you might find more flexible zero-down options.

The Role of Brokers: Unlocking Hidden Opportunities and Matching Retirees with Ideal Lenders

Auto finance brokers act as intermediaries, connecting you with multiple lenders without you having to apply individually to each. They understand the criteria of various financial institutions and can efficiently match your investment income profile with lenders most likely to approve your zero-down application. This can save you time, protect your credit score from multiple inquiries, and potentially unearth better rates or more favourable terms than you might find on your own. Many specialized auto finance companies operate as brokers or have strong brokerage divisions.

Pro Tip: The Power of Pre-Approval – Your Negotiation Superpower in Any Showroom

Before you even step foot into a dealership, secure a pre-approval. This means a lender has already evaluated your financial situation, including your investment income, and committed to lending you a specific amount at a certain interest rate. Armed with a pre-approval, you become a cash buyer in the eyes of the dealership. This empowers you to negotiate the car's price separately from the financing, potentially saving you thousands. It also gives you a benchmark; if the dealership offers a better rate, great! If not, you have your pre-approved loan ready.

Maximizing Your Approval Odds: Beyond the Credit Score

While a good credit score is always beneficial, for retirees with investment income, it's just one piece of the puzzle. Lenders understand that your financial narrative is unique. To secure a zero-down car loan, especially in 2026, you need to present an application that highlights your overall financial stability and reliability, leveraging all available assets and demonstrating meticulous debt management. This section focuses on strategies to make your application shine.

The Unsung Hero: Demonstrating Income Stability and Predictability Through Documentation

As discussed, consistent income is paramount. For retirees, this means showing a robust history of investment income. Provide comprehensive documentation:

- Investment Account Statements: 6-12 months, clearly showing dividends, interest, or withdrawal patterns.

- RRIF/RRSP Withdrawal Schedules: Official documents outlining planned distributions.

- Bank Statements: Reflecting regular deposits from your investment income.

- Tax Returns (NOA): Your Notice of Assessment for the past 2-3 years, validating declared income.

- Letters from Financial Advisor: A letter confirming your investment strategy, portfolio value, and sustainable withdrawal rates can add significant credibility.

Lenders want to see that your income will consistently cover the proposed car payment, even with a zero-down commitment.

Credit Score Re-examined: What a 'Good' Score Truly Means for Retiree Auto Finance

For zero-down financing, a credit score of 700+ is generally considered 'good' or 'prime' in Canada and will open the door to the best rates. However, a score in the 650-699 range (good) can still qualify, though perhaps with a slightly higher interest rate. Even if your credit isn't perfect, a strong investment income can compensate. Lenders are more flexible when they see consistent income and responsible financial behaviour. If you're concerned about past credit issues, exploring options for those with less-than-perfect credit is wise. For those with no credit history, options still exist. See our article on Zero Credit? Perfect. Your Canadian Car Loan Starts Here.

Debt Management: How Existing Obligations Impact Your Eligibility and Strategies for Optimization

Lenders will scrutinize your existing debt-to-income (DTI) ratio. High existing debts, such as mortgages, lines of credit, or other loans, can reduce your borrowing capacity, even with strong investment income. Before applying for a zero-down car loan, consider:

- Reducing High-Interest Debts: Paying down credit card balances or personal loans can significantly improve your DTI.

- Consolidating Debts: If feasible, consolidating multiple debts into a single, lower-interest payment can simplify your financial picture and free up cash flow.

- Avoid New Debt: Refrain from opening new credit accounts or taking on additional loans in the months leading up to your car loan application.

For retirees who have recently completed a debt management plan, lenders are often more understanding of past issues, especially with a clear path forward. For more on this, read DMP Done? Your 2026 Car Loan Awaits. Canada.

Leveraging Assets: How Your Net Worth Can Indirectly Strengthen Your Application (Without Collateral)

While a zero-down loan means you're not putting up collateral directly, your overall net worth is an indirect but powerful asset. Lenders view substantial non-registered investments, real estate equity, or other valuable assets as indicators of financial stability and a safety net. Even if you're not using them as collateral, disclosing your net worth (through investment statements or property assessments) demonstrates a strong financial position, reducing perceived risk and potentially leading to better loan terms, even for a zero-down option. It shows you have resources to fall back on if income streams face unexpected disruptions.

Building a Strong Case: The Art of Presenting a Comprehensive Application Package

Think of your application as a financial story. Present it clearly and comprehensively. Organize all your documents – income statements, bank statements, tax documents, investment summaries, and credit report. A well-organized, thorough application package signals responsibility and makes the lender's job easier, which can accelerate approval. Highlight the consistency of your investment income and any significant assets you hold.

Pro Tip: Co-Signers and Guarantors – When They Help and When They Might Hinder Your Application

A co-signer or guarantor can significantly strengthen your application, especially if your credit score is borderline or your investment income is perceived as less stable. They essentially guarantee the loan if you default. This can help you secure approval or a better interest rate. However, ensure they understand the full implications, as their credit will be affected, and they will be legally responsible for the debt. Only consider this if absolutely necessary and with full transparency between all parties. Sometimes, a co-signer can also complicate the process if their own financial situation is complex, so weigh the pros and cons carefully.

The True Cost of Convenience: Hidden Fees, Insurance, and Extended Warranties

Securing a zero-down car loan with investment income is a significant achievement, but the journey to true car ownership doesn't end there. Beyond your monthly payment, a myriad of additional costs can surprise retirees if not anticipated. Understanding these "hidden" expenses is crucial for accurate budgeting and ensuring your new vehicle remains a joy, not a financial burden. This section will dissect all the associated costs, helping you budget comprehensively for your 2026 car purchase.

Beyond the Monthly Payment: Dissecting Loan Origination, Administrative, and Documentation Fees

While you might avoid a down payment, other upfront costs can still apply. These typically include:

- Loan Origination Fees: Some lenders charge a fee for processing your loan, usually a small percentage of the loan amount or a flat fee.

- Administrative Fees: Dealerships often add administrative or "doc" fees to cover the cost of paperwork, licensing, and other internal processes. These can range from a few hundred dollars to over a thousand in some provinces like Ontario. Always ask for a breakdown and negotiate if possible.

- Documentation Fees: Specific charges for preparing the sales contract and other necessary documents.

These fees might not be explicitly advertised, so always scrutinize the full purchase agreement before signing. They will be added to the total amount you finance or paid out-of-pocket, even with a zero-down loan.

Mandatory Insurance: The Non-Negotiable Cost of Ownership and How it Varies for Retirees

Comprehensive car insurance is not just a good idea; it's mandatory for financed vehicles, especially zero-down loans, to protect the lender's asset. The cost of insurance can vary significantly for retirees based on several factors:

- Age and Driving Record: While older drivers can sometimes face higher premiums, a clean driving record and decades of experience often result in favourable rates.

- Vehicle Type: More expensive, high-performance, or frequently stolen vehicles will have higher premiums.

- Location: Insurance rates vary by province and even by city. For example, premiums in a bustling city like Toronto or Montreal are typically higher than in rural Alberta.

- Coverage Level: Lenders will require full collision and comprehensive coverage.

Always get insurance quotes before finalizing your purchase to understand this significant ongoing cost. Expect to pay anywhere from $100-$300+ per month, depending on these factors.

Extended Warranties: Are They a Prudent Investment for Retirees or an Unnecessary Expense?

Extended warranties offer peace of mind by covering repairs beyond the manufacturer's basic warranty. For retirees on a fixed income, avoiding unexpected, costly repairs can be appealing. However, they come at a significant cost (often $2,000-$4,000, which can be rolled into your zero-down loan). Consider:

- Vehicle Reliability: Research the specific car's reliability ratings. If it's known for issues, a warranty might be wise.

- Your Financial Buffer: Do you have an emergency fund sufficient to cover a major repair (e.g., $3,000-$5,000)? If not, a warranty might be a good hedge.

- Coverage Details: Read the fine print! What's covered? What's excluded? Are there deductibles?

Often, these are negotiable. For a highly reliable vehicle, an extended warranty might be an unnecessary expense, but for others, it could be a prudent investment in financial security.

Registration, Taxes, and Licensing: The Initial Out-of-Pocket Expenses to Budget For

Even with zero down on the loan, you'll still have initial out-of-pocket expenses for:

- Sales Tax: HST/GST/PST applies to the full purchase price of the vehicle, regardless of whether you make a down payment. This can be thousands of dollars (e.g., 13% HST in Ontario on a $30,000 car is $3,900). While it can sometimes be rolled into the loan, it's often an upfront cost or added to the principal, increasing your payments.

- License Plates and Registration: Annual fees vary by province but are typically a few hundred dollars.

- Tire Levy: A small environmental fee on new tires.

These are unavoidable government charges and should be factored into your overall budget, as they might not be part of your zero-down financing.

The 'Total Cost of Ownership' Equation: Factoring in Fuel, Maintenance, and Depreciation Over Time

Beyond purchase and financing, consider the total cost of ownership over the years:

- Fuel: Electric vehicles (EVs) have different costs than gasoline cars. Factor in your driving habits.

- Maintenance: Regular oil changes, tire rotations, brake service, and occasional repairs. New cars have lower maintenance initially, but costs rise with age.

- Depreciation: The value a car loses over time. With zero down, you're always "upside down" for longer, meaning you owe more than the car is worth, which impacts trade-in value.

A comprehensive view of these costs helps ensure your zero-down car finance decision is sustainable for your retirement lifestyle.

Choosing Your Ride: Car Brands, Models, and Resale Value Considerations for Retirees

Selecting the right vehicle is paramount for retirees, especially when utilizing zero-down financing. Your choice should align not only with your lifestyle and budget but also with long-term financial goals, focusing on reliability, safety, comfort, and the crucial aspect of resale value. This section guides you through making an informed decision for your 2026 vehicle purchase in Canada.

Reliability First: Brands Known for Longevity, Lower Maintenance Costs, and Peace of Mind

For retirees, a reliable vehicle translates to fewer unexpected repair bills and less stress. Brands consistently ranking high in reliability surveys (like those from J.D. Power or Consumer Reports) often include:

- Toyota & Honda: Known for bulletproof engines, long lifespan, and high resale value.

- Subaru: Excellent for all-weather driving in places like Alberta or British Columbia, with a reputation for durability.

- Mazda: Increasingly lauded for reliability, driving dynamics, and premium interiors at a good value.

- Hyundai & Kia: Have significantly improved reliability and offer excellent warranties.

Opting for a reliable brand can offset some of the higher interest costs associated with zero-down financing by reducing maintenance expenditures over the loan term.

Safety Features: Prioritizing Advanced Driver-Assistance Systems (ADAS) and Crash Test Ratings

Safety should be a top priority. Look for vehicles equipped with comprehensive ADAS features, such as:

- Automatic Emergency Braking (AEB): Can prevent or mitigate frontal collisions.

- Lane-Keeping Assist (LKA) & Lane Departure Warning (LDW): Helps keep the vehicle within its lane.

- Blind-Spot Monitoring (BSM) & Rear Cross-Traffic Alert (RCTA): Crucial for highway driving and parking lot manoeuvres.

- Adaptive Cruise Control (ACC): Reduces driver fatigue on long trips.

Check crash test ratings from organizations like the Insurance Institute for Highway Safety (IIHS) and the National Highway Traffic Safety Administration (NHTSA) for their top safety picks. Many new cars, even entry-level models, offer these features as standard or affordable options in 2026.

Ergonomics and Accessibility: Ensuring Comfort, Ease of Entry/Exit, and User-Friendly Controls

As we age, comfort and ease of use become increasingly important. Consider:

- Seat Comfort: Adjustable lumbar support, heated seats, and easy-to-reach controls.

- Entry/Exit: SUVs and crossovers often offer a higher ride height, making it easier to get in and out compared to lower sedans.

- Visibility: Good all-around visibility, large windows, and minimal blind spots.

- User-Friendly Controls: Intuitive infotainment systems, physical buttons for common functions (instead of touchscreens for everything), and clear instrument clusters.

Test drive thoroughly, paying attention to these details, especially if you plan long road trips across provinces.

The Resale Value Factor: Protecting Your Investment (Even Without an Initial Down Payment)

Even with zero down, your vehicle is a significant investment. High resale value mitigates depreciation, meaning you'll lose less money when you eventually sell or trade it in. Brands like Toyota, Honda, and Subaru consistently hold their value well in the Canadian market. Choosing a popular colour, a common trim level, and avoiding excessive aftermarket modifications can also help maintain resale value. This is particularly important for zero-down loans, where you start with no equity; a strong resale value helps you recover equity faster.

New vs. Used: Weighing the Financial Implications and Benefits for Zero-Down Applicants

The new vs. used debate is crucial for zero-down applicants:

- New Cars: Offer the latest safety features, technology, full warranty, and often access to lower promotional interest rates (though zero-down deals might still carry slightly higher rates). Depreciation is steepest in the first few years.

- Used Cars: Significantly lower purchase price, meaning a smaller loan amount and less overall interest paid. Depreciation has already occurred, so the loss in value is slower. However, warranties might be shorter or expired, and maintenance costs could be higher.

For zero-down, a slightly used (1-3 years old) reliable model can offer an excellent balance, giving you a lower principal to finance while still benefiting from modern features and some remaining warranty.

Pro Tip: Test Driving Beyond the Showroom – Evaluating Real-World Usability and Comfort

Don't just take a quick spin around the block. Request an extended test drive (at least 30-60 minutes) that includes typical driving conditions you'll encounter: city traffic, highway speeds, parking maneuvers, and perhaps even a familiar route like your grocery store or doctor's office. Pay attention to blind spots, ease of parking, road noise, seat comfort over time, and how intuitively you can access controls. If possible, test drive the car at different times of day to assess visibility and headlight performance. This real-world evaluation is critical for long-term satisfaction.

The Road Ahead: 2026 Market Outlook and Emerging Trends in Retiree Auto Finance

The auto finance landscape is constantly evolving, and 2026 promises significant shifts that will directly impact retirees seeking car loans, especially those relying on investment income. From regulatory changes to the rise of electric vehicles and new ownership models, staying informed is key to making the best financial decisions. This section offers a forward-looking perspective on what Canadian retirees can expect.

Regulatory Shifts: How Potential New Rules Might Impact Retiree Lending and Protections

The Canadian financial sector is always under review. In 2026, we could see further tightening of lending regulations aimed at consumer protection. This might include more stringent income verification processes, clearer disclosure of total loan costs, or limits on extended loan terms. While this could make zero-down financing slightly more challenging for some, it ultimately protects retirees from predatory lending practices. Keep an eye on announcements from the Financial Consumer Agency of Canada (FCAC) for any updates that might affect how lenders assess your investment income and overall eligibility.

Technological Innovations: The Rise of Electric Vehicles (EVs) and Their Financing Implications for Retirees

Electric vehicles (EVs) are no longer a niche market; they are rapidly becoming mainstream. For retirees, EVs offer benefits like lower fuel costs, reduced maintenance, and a quieter ride. However, their higher upfront purchase price can be a hurdle, especially for zero-down financing. Expect more tailored EV financing options in 2026, potentially including government incentives (federal and provincial) that can effectively reduce the amount to be financed. Lenders may also start offering slightly better rates for EVs due to lower running costs, which could improve a borrower's ability to pay.

Economic Forecasts: Interest Rate Predictions and Their Effect on Auto Loan Affordability

Interest rates are a critical factor in auto loan affordability. Economic forecasts for 2026 suggest a period of potential stability or moderate fluctuations after recent shifts. Retirees should monitor the Bank of Canada's policy rates, as these directly influence prime lending rates for auto loans. Even a 0.5% increase or decrease can significantly impact your monthly payments over a long loan term, especially for zero-down loans with higher principals. Planning your purchase when rates are favourable can save you thousands over the life of the loan. Always factor in potential rate changes when evaluating long-term affordability.

Alternative Ownership Models: Exploring Subscription Services and Their Viability for Retirees

Beyond traditional ownership, alternative models like car subscription services are gaining traction. These services (offered by some manufacturers or third-party companies) provide access to a vehicle for a monthly fee that typically includes insurance, maintenance, and registration. For retirees, this could be an appealing zero-down option, offering flexibility and predictability without the long-term commitment or depreciation risk of ownership. However, the total cost over several years often exceeds traditional financing, so a careful cost-benefit analysis is essential based on your driving needs and financial situation.

The Future of Investment Income Verification: Streamlined, Digital Processes on the Horizon?

As technology advances, the process of verifying investment income for loan applications is likely to become more streamlined. Expect increased use of secure digital platforms that can link directly to your financial institutions (with your permission) to verify income and asset statements in real-time. This could significantly speed up the approval process for retirees, making it easier to demonstrate the consistency of your investment income without extensive paper documentation. This digital transformation will likely enhance accuracy and efficiency for both borrowers and lenders.

Your Next Steps to Driving Away with Confidence

Embarking on the journey to secure a zero-down car loan with investment income in Canada requires a strategic approach. By following these steps, retirees can confidently navigate the process, secure the best possible terms, and drive away in a vehicle that perfectly suits their needs and financial comfort. This guide provides a practical, step-by-step roadmap to empower your decision-making.

Step 1: Comprehensive Financial Health Check-Up and Meticulous Documentation Gathering

Start by taking a detailed inventory of your financial situation. Understand your monthly investment income from all sources, your current expenses, and your overall net worth. Critically assess how much you can realistically afford for a monthly car payment, including insurance and other running costs. Then, gather every piece of documentation that validates your income and financial stability:

- Bank statements (6-12 months)

- Investment account statements (showing dividends, interest, or withdrawals)

- RRIF/RRSP withdrawal schedules

- Latest Notice of Assessment (NOA) from CRA (2-3 years)

- Any rental property lease agreements and income statements

- Proof of other pension income (if applicable)

- Your credit report and score (obtained from Equifax or TransUnion)

The more prepared you are, the smoother the process will be.

Step 2: Exploring All Lender Options and Securing the Best Pre-Approval Offer

Do not limit yourself to just one lender. Research and contact a variety of financial institutions: traditional banks, local credit unions, and specialized auto finance companies like SkipCarDealer.com. Clearly explain your income sources and your goal of zero-down financing. Seek pre-approval from at least two or three different lenders. This will give you a clear understanding of the interest rates and terms you qualify for, empowering you with a benchmark for negotiation. Remember, pre-approval is a soft inquiry that typically doesn't harm your credit score significantly.

Step 3: Smart Vehicle Selection, Thorough Research, and Extensive Test Driving

With your pre-approval in hand, you know your budget. Now, focus on finding the right vehicle. Prioritize reliability, safety features, comfort, and good resale value. Use online resources to research models that fit your criteria, read reviews, and compare features. Once you've narrowed down your choices, schedule extensive test drives. Don't rush. Drive the car in various conditions, assess ergonomics, and ensure it meets your practical needs. Consider both new and certified pre-owned options to find the best value within your budget. Think about future maintenance, fuel costs, and insurance premiums for each model.

Step 4: Decoding the Loan Agreement, Understanding All Terms, and Skillfully Negotiating

When you've chosen your car and are presented with a final loan agreement, read every single line item carefully. Understand the total loan amount, the interest rate, the loan term, and the total cost of the loan (principal + interest). Ask about any fees (origination, administrative, documentation) and how they are handled. Don't be afraid to negotiate, not just on the vehicle's price, but also on the loan terms, if you have a competitive pre-approval offer. Ensure you understand all insurance requirements and whether any extended warranties are being pushed (and if they are truly necessary for your situation).

Step 5: Finalizing the Purchase and Implementing Strategies to Protect Your Investment Long-Term

Once you are fully satisfied with all terms and have signed the agreement, congratulations – you're a car owner! But the journey continues. Implement long-term strategies to protect your investment:

- Maintain a Budget: Stick to your monthly car payment budget and factor in all running costs.

- Regular Maintenance: Follow the manufacturer's recommended maintenance schedule to keep your vehicle reliable and preserve its value.

- Monitor Your Investments: Continue to manage your investment portfolio to ensure a steady income stream for future payments.

- Consider Extra Payments: If your budget allows, making extra payments towards the principal can significantly reduce the total interest paid and help you build equity faster, mitigating the zero-down effect.

By staying proactive, your zero-down car finance with investment income will be a smooth and rewarding experience.